A common question when considering a title loan is can you get one if you are still making payments on a car? Generally, to get a car title loan, most title lenders require what is called a lien free title.

What is a Lien Free Title?

Before we can figure out how to get a title loan while still making payments we need to understand what is meant by a lien free title and why it is such and important requirement. To get a title loan, the lender will need to record their lien on your vehicle title. This provides them with a security interest in the vehicle. Before they can record their lien, any previous liens must first be removed.

When you purchase a vehicle it is either purchased outright (fully paid) or financed. If it is purchased outright you receive a title without any liens (a lien free title). When you finance the vehicle the financer records their lien on your title. The lien remains until you make your final car loan payment.

If you are still making payments on a vehicle, then this means your title has a lien. The lien holder is the finance company you are making your payments to.

This does not mean, however, that it is not possible to get a title loan while still making payments. It absolutely is, it just depends on the specifics of the situation.

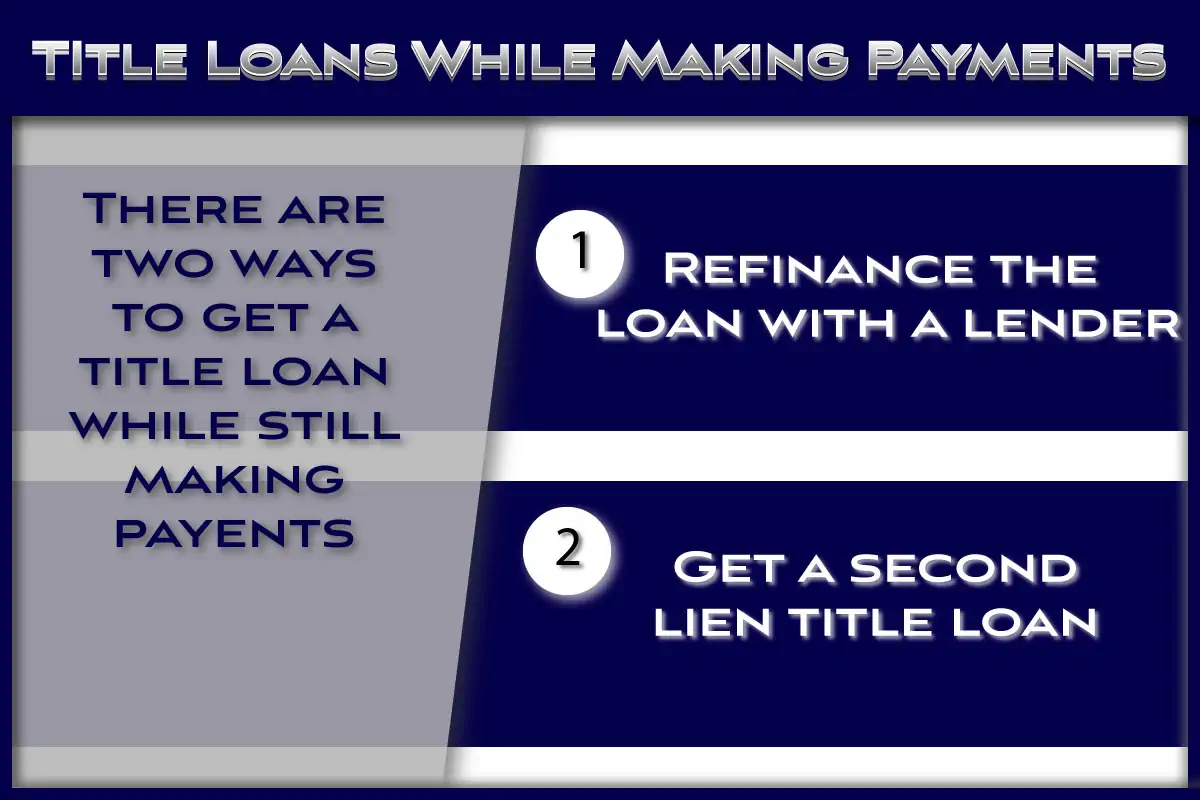

It is possible to get a title loan while still making payments assuming there is enough equity in the vehicle to support the loan. There are a few ways to accomplish this. These include both a title loan refinance and getting a second lien title loan.

How to get a Title Loan while still Making Payments

While most title loans do require a paid off vehicle, in some cases it is possible to get a title loan while still making payments. The ability to get a car title loan in this situation will depend on two major factors:

- The value of the vehicle

- The current balance on your existing loan

If you are very close to finished paying off your existing loan, the lender may opt to pay the remaining balance and make the title loan.

This is more likely to happen if the vehicle has a significant amount of equity, like a late model car with low mileage. The amount will be added to your loan with the title lender.

This is the most common way to get a title loan while still making payments. But what if you have a significant number of payments left?

With a large number of payments left it can be more difficult to get a title loan. This depends on how much you still owe, versus how much the vehicle is worth.

Vehicle Value versus Loan Balance

To illustrate the point above, let’s take a look at several different scenarios that involve getting a title loan while still making payments; and the probability of being approved based on the amount still owed.

| Vehicle Value | Existing Loan Balance | Equity After Loan | Title Loan Approval Probability |

|---|---|---|---|

| $20,000 | $1,000-$5,000 | $17,000-$19,000 | High |

| $20,000 | $6,000-$15,000 | $5,000-$14,000 | Medium |

| $20,000 | $16,000-$19,000 | $1,000-$4,000 | Low |

| $10,000 | $1,000-$3,000 | $7,000-$9,000 | High |

| $10,000 | $4,000-$6,000 | $4,000-$6,000 | Medium |

| $10,000 | $7,000-$9,000 | $1,000-$3,000 | Low |

As you can see from the table above the equity in the vehicle and the loan balance will determine whether or not you can get a car title loan while still paying off an existing loan.

Title Loan Example While Making Payments

To illustrate the situation above, let’s say you purchased a new car a few years ago and toady it is worth $18,000. You still have some payments left and owe $2,000 on the vehicle. You are looking for a $3,000 title loan.

In this case, the lender may opt to pay the $2,000 you owe to the bank that financed your new car purchase and lend you the $3,000 you need for your title loan.

The total amount of the title loan will be $5,000 because the lender paid your lienholder $2,000 and you $3,000. This means you would no longer have a car payment since that loan will have been satisfied, but you will have a payment on a $5,000 title loan.

Refinancing and 2nd Lien Title Loans

What about if you have more than a few payments left? In these cases, you will either need to:

- Get a Second Lien Title Loan

- Refinance the loan

Second lien title loans are not available from all lenders and are more difficult to get.

Vehicle Payment Types for Existing Loans

The ability to get a title loan while still making makings depends on what type of loan you are still making payments on. The two most common types of loans include:

- A New or Used Car Loan

- A Car Title Loan

Whether or not you can get a title loan while making payments will depend on both the vehicle value and the amount left on the loan. Ideally you will only have a few payments left with a vehicle value that is significantly more than the amount still owed.

If you just got the loan and have only paid a small portion, then it may be more difficult to get a title loan while still making these payments. It may be an option to refinance the title loan at a lower rate.

Car Loan Payments

There are, however, a couple of ways to get a title loan if you have an existing lien on the vehicle. These are a bit more difficult than a typical title loan and may take longer depending on the specifics of your vehicle and existing loan. This is similar to refinancing the title loan, except it may be easier if the existing loan is not a title loan.

Rather, it is a loan from a car dealer or bank. In these cases, it is not considered refinancing the title loan because no title loan exists yet. This is often easier because it is not considered a title loan refinance.

Title Loan Payments

If you are still making payments on a car title loan, then getting another title loan will require refinancing the existing title loan. This is possible but not available in all states. Contact your lender to see if it is available to you.

Three ways to get a Car Title Loan while still making Payments:

- Satisfy the existing loan prior to the new one

- Get a 2nd Lien Title Loan

- Refinance the existing title loan

The first way to get a car title loan while still making payments is to satisfy the existing loan and have the lien removed.

The fastest and easiest way to accomplish this would be to borrow the money needed to satisfy the existing loan from a friend or relative, and pay them back as soon as you title loan is funded.

This is not an option for everyone, so we’ll go over the next two methods.

1. Removing Liens by Paying off Loans

In some cases, title lenders will pay off your existing loan, have the lien removed, and add their lien to your title. This depends on several factors including what state you live in, how much you still owe, and the current value of your vehicle.

Some states require title lenders to record the lien on the physical title. Others allow the lender to place an electronic lien on the title. If the lien on your vehicle is electronic, and the title lender can place the lien electronically, then the process may be fairly easy.

2. Second Lien Title Loans

A second lien is a lien added to a title with an existing lien. It is not common for title loan companies to add a lien to a title as the second lienholder.

Most of the time, the first lienholder needs to grant permission for the title lender to be added as the second lienholder. You can probably guess how many banks and finance companies will allow this.

Second lien title loans, by name, are a bit misleading. Most title loan companies that make loans to customers with existing liens will either satisfy the lien using proceeds from your loan, or don’t record their lien.

They call the loans second lien title loans, but do not necessary record the second lien. This is not permitted in every state.

Qualifying for a Second Lien Title Loan

To be able to apply for, and be approved for, a car title loan while still making payments on another loan you will need to meet some minimum qualifications.

First, you will need to meet the requirements for a title loan (obviously) including being 18 years of age, having a valid ID, insurance, etc.

Beyond the regular title loan requirements you must have enough equity in your vehicle to both cover your existing lien and support the amount you want to borrow for your title loan.

How to get a 2nd Lien Title Loan Online

Before getting any title loan, including a 2nd lien title loan, we recommend preparing. This includes finding the lender with the lowest rate and making sure you budget for the payments. Find a payment schedule that you are sure you can stick to.

3.Refinancing a Title Loan

One of the easiest ways to get a title loan while still making payments, without coming up with extra money, is to get a title loan refinance. In this case, the lender that does the refinance will pay off the existing loan.

Cleanest way to get a Title Loan with a Lien

We have already mentioned it, but it is worth mentioning again. The cleanest way to get a title loan is satisfying the existing lien first. The fastest way to satisfy the lien is to repay the loan in full.

Obviously this is easier if you are closer to the end of the loan. Depending on how much your vehicle is worth, and how much you still owe, the title lender may be willing to pay of your existing loan to make the loan.

Getting a Car Title Loan while still making Payments – Examples

If you have an existing lien and find a lender willing to satisfy the existing lien, here are a few examples of what your loan would look like. A portion of the loan would go towards paying off your existing car loan.

The remainder would go to you as the borrower. This means your existing car payment would be gone, and replaced with a payment to the title lender.

| Car Value | Existing Loan Amount | Title Loan Amount | Net Proceeds |

|---|---|---|---|

| $10,000 | $2,000 | $5,000 | $3,000 |

| $10,000 | $3,000 | $5,000 | $2,000 |

| $15,000 | $4,000 | $7,000 | $3,000 |

| $15,000 | $2,000 | $7,000 | $5,000 |

How to get a Lien Released

If you recently paid off your existing car loan, your lender should send you a free and clear title. Sometimes this process can get delayed. This delay may come at a time when you need your title for a title loan.

Contact your lender and find out where they are in the process of releasing your lien and sending you your title. If you’re still having problems, contact the DMV and follow their recommended process.

Make sure to keep of the final payment to your lender to show that you satisfied your financial obligations.

Cost of a Title Loan while still making Payments

The costs of getting a title loan while still making payments will depend on which lender you choose and what they charge. To get an idea of car title loan costs use our car title loan calculator. If you are refinancing a title loan, you can get an idea of how much you may be able to save.

Summary

It is possible to get a title loan while still making payments on a car loan. This is only recommended if the amount owed on the existing car loan is very small compared to the value of the car. Car title loans generally have much higher rates than regular car loans.

So rolling your existing car loan into a title loan balance will likely be comparatively expensive. To get an idea of how much the title loan will cost you can use our title loan calculator to compare different loan amounts and terms.

You can get a title loan while still making payments on a current loan as long as you have enough equity in the vehicle to support the loan.

To get a title loan while still making payments first gather the documents related to the existing loan. Next apply for a title loan refinance with a title loan company that offers these types of loans.

Second lien title loans are available is some states but are not common. Many states do not permit second lien title loans, and those that do require permission from the first lien holder. Because of this most title lenders will pay off the existing loan as a part of the title loan refinance process.