Title Loan Refinance

- Save by Refinancing

- Lower Payments

- Renegotiate Payment Schedule

- Simply get a Better Deal

Refinancing a title loan can be an alternate solution for borrowers with a loan that has unfavorable terms. Perhaps the payment is very difficult to make on time or the interest rate is simply not reasonable. When getting a title loan for the first time it is common to rush and not have time to find the best company with the best deal.

Refinancing the title loan provides the opportunity to correct this and get the best deal going forward. Often, this results in a significant savings of hundreds and even thousands of dollars.

Some borrowers are stuck in title loans where they’ve made payments for months without significantly lowering the principal loan balance. This can be frustrating.

Title loans can have very high interest rates and additional fees that may result in a loan that is very costly and difficult to repay. The ability to reduce both your monthly payment and total cost is possible.

Causes of Unfavorable Terms

Car title loans are often used for urgent or emergency expenses. Some borrowers simply don’t have the time to find the best title loan with reasonable payments while dealing with the emergency.

This can, and often does, lead to hurrying to solve a financial problem. Some borrowers simply go to the closest title lender or visit the first search result and move forward. The result of this rushed title loan acquisition can be a very high interest loan that is very difficult to repay.

Finding the best online title loan, with lower payments and no fees, is not always an easy thing to accomplish. This is especially true when you don’t have time to compare multiple lenders.

In these cases, consider restructuring your loan with a title loan refinance. This can be a good way to get a better deal on your existing loan, now that the pressing financial issue no longer exists.

What is a Title Loan Refinance?

A title loan refinance is a way to renegotiate your loan to get a lower interest rate or different term to make repayment easier and to decrease the total repayment cost. This can be done both with your existing lender (in some cases) or with a different lender altogether.

Essentially, you restructure your title loan at a rate that is lower than your current rate. You can also change the length of your loan, if that is permitted in your state. This makes it easier to repay and ultimately ends up saving you money when done right.

It is important to note that refinancing a title loan is not permitted in every state. To find out if you can refinance your title loan simply inquire online.

Type of Title Loans that can be Restructured

Before looking into whether or not refinancing your loan makes sense, it is important to understand the two main types of title loans – those with a single payment and those with monthly installments. Generally, refinancing a title loan with monthly installments is the more common type.

This assumes you are not rolling over your single payment title loan; if that’s the case a refinance may be possible for a single payment title loan to avoid multiple rollovers. As we’ve mentioned roll overs can get very costly.

Monthly Installment Title Loans

Title loans with monthly installments are usually amortized over the loan period. This means the total loan cost is broken into equal monthly payments consisting of both interest and principal. Many loans like car loans and mortgages are amortized.

Title loans can be amortized over a period of any where from a few months to over a year. Amortizing a high interest loan over a longer period often results in an exponential increase in interest costs.

If you signed up for a high interest loan with a long term, then refinancing this title loan may be a good idea. Doing so can significantly reduce your total cost.

Monthly Installment Loan Costs

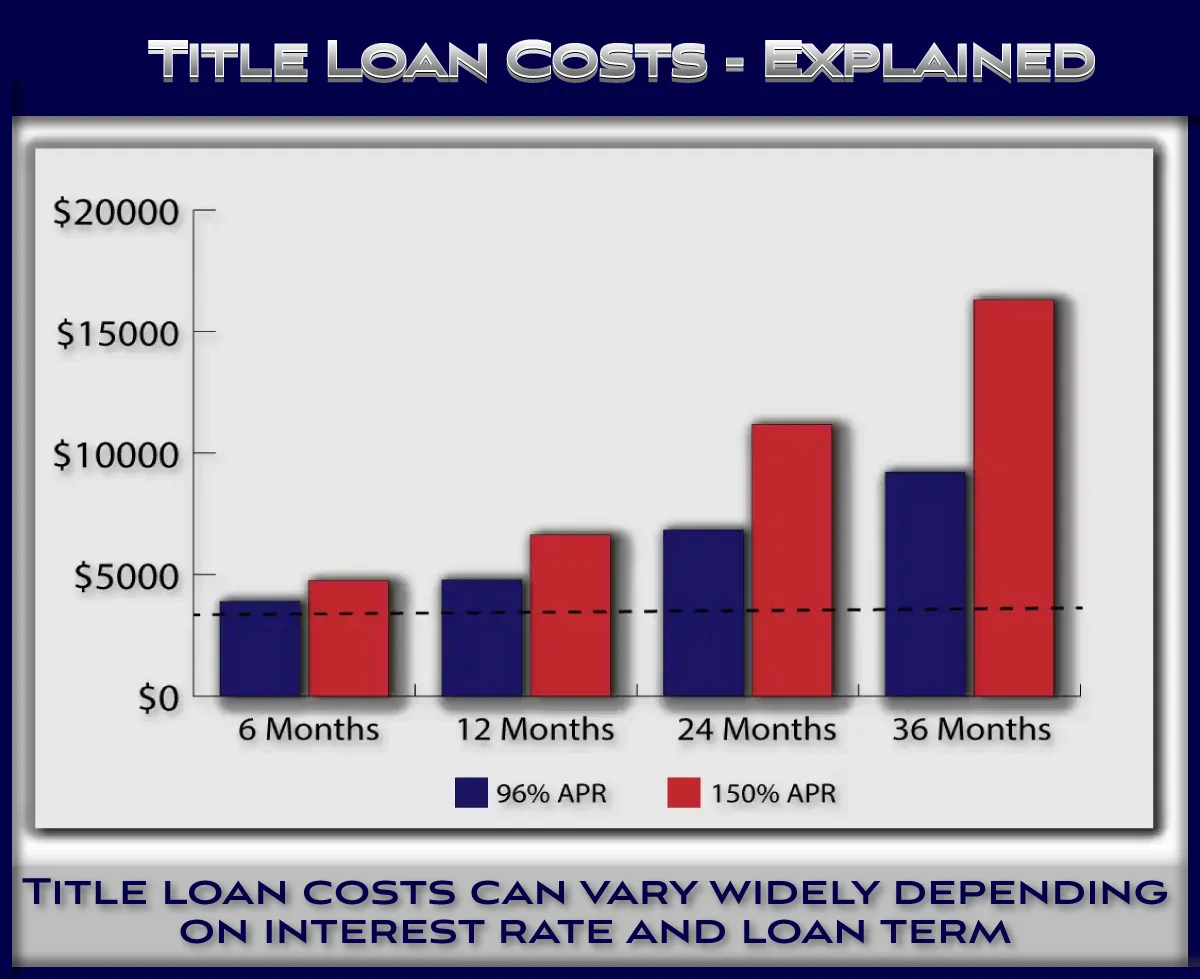

As mentioned, amortizing a title loan over a longer period can increase costs significantly; especially if the interest rate is high. To illustrate this, take a look at a $3,000.00 title loan, amortized over a 6, 12, 24, and 36, month period.

To further provide an idea of how the interest rate effects the cost we included both a 96% and a 150% title loan. There are many title loans with interest rates higher, in some cases much higher than 150%.

To illustrate the costs associated with these loans, and the difference between them and new one at a lower rate, we created a refinance calculator. This allows you to get an idea of what they can potentially save by refinancing. It will require time and effort so it does need to be worth it.

Single Payment Title Loans

The other type of title loan is one with a single payment due at the end of the term instead of monthly installments. These are generally not refinanced as they are very short term with only one single payment.

Benefits of Refinancing a Title Loan

Refinancing a title loan has numerous benefits, including:

- Lower Interest Rate

- Reduced Total Loan Cost

- More Affordable Monthly Payment

- More Favorable Terms

- Better Title Loan Company

The main benefit of refinancing is a lower monthly payment and total loan savings. This makes the title loan easier to repay and ultimately more affordable.

For many borrowers the main reason for wanting to complete this process is to lower the interest rate and therefor lower the monthly payment and total cost.

There are title loan companies today offering title loans at much better rates than many of the larger lenders charging the maximum allowable rate in that state. Many borrowers rush in to these loans and are now looking for a better alternative.

Getting a Title Loan Refinance to Save Money

The purpose of a refinancing a title loan is to save money and lower payments. Before moving forward with one most borrowers would like an idea of how much they could save. This allows you to determine whether or not the refinance is worth the time and effort.

Just like with a regular title loan, a cost benefit analysis makes sense for a refinance as well. The benefit (amount saved) should outweigh the cost (time and effort spent) for the transaction to be worth it.

Title Loan Refinance Savings Calculator

The title loan refinance savings calculator provides an estimate of how much you might be able to save. This assumes you know your current loan amount and interest rate, and have an idea of what interest rate you can get with a refinance.

Simply enter the values and take a look at the results. To get a more accurate quote simply apply online when ready.

How to Renegotiate a Title Loan

Refinancing a title loan is generally a fairly easy process, similar to the process of getting the loan in the first place. Contact the lender you want to deal with and apply for a title loan refinance with them.

The application will be reviewed and either approved or denied. In some states refinancing a title loan is not permitted. Once your application is approved, the loan will be processed similar to when you got the original title loan. Make sure to have all of your information available to ensure the process can be completed quickly.

You will be provided with a loan agreement. Make sure to read and understand the entire loan agreement. This will define your payment schedule, interest rate, fees including late fees, loan default definition, and other critical information about how your loan will be governed.

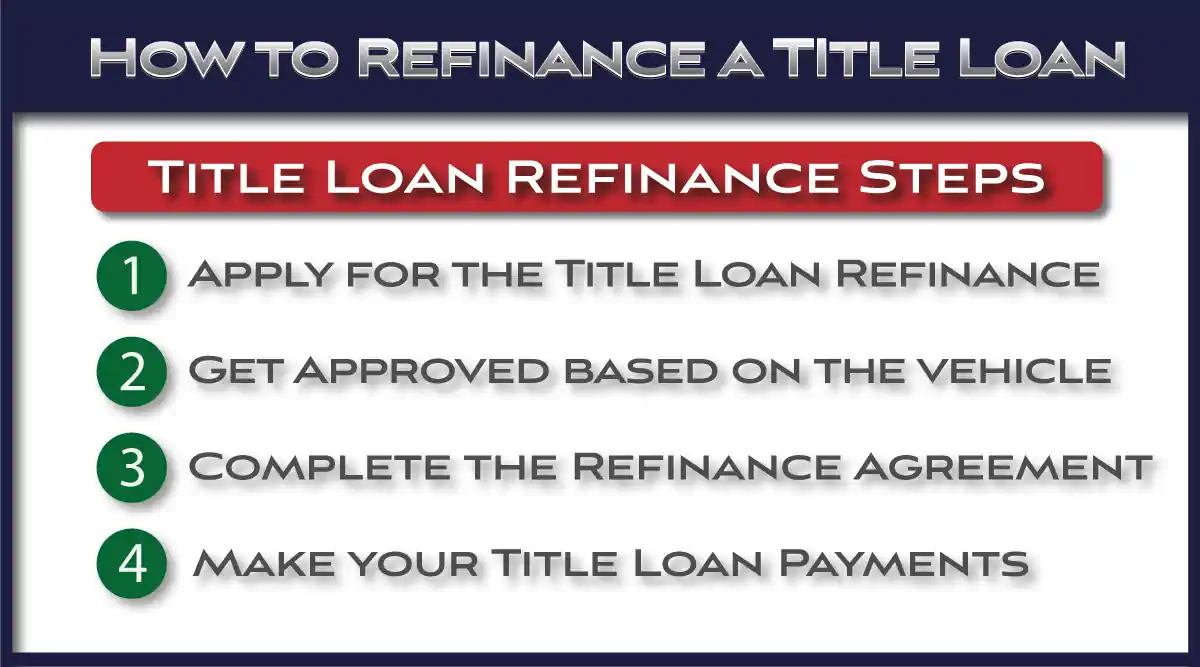

As shown there are four simple steps to a title loan refinance:

- Apply for the title loan refinance

- Get Approved based on the vehicle value

- Complete the refinance agreement

- Make your payments

As with any other loan proper preparation is recommended.

Making Payments

Title loans are secured loans with the collateral being the vehicle used for the loan. This means defaulting on the loan can result in repossession. This is one of the reasons for refinancing the title loan and the last thing any vehicle owner wants.

Make sure to make your title loan payments on time to avoid any possibility of default. Paying on time also avoid late fees and extra interest charges.

Refinance a Title Loan Online

The same online options are available for refinances as they are for getting new title loans. This includes completely online title loans with no store visit. These options may have an electronic title loan agreement. Regardless, make sure to read the loan agreement in full before signing.

The fact that you already have a title loan may make the process of refinancing easier. You should have all of the information you had when you applied for the original loan ready when applying for the refinance online.

Summary

Having a title loan that is too expensive and/or simply not affordable is not a good situation. It may be possible to improve things by considering refinancing the loan.

Finding a lower rate lenders, with better interest rates and lower or no fees, can significantly reduce your title loan payment and cost. For those stuck with a very high interest loan it is definitely something worth looking in to.

FAQs

In most cases you can refinance an existing title loan assuming the loan is in good standing. To get a title loan refinance you will follow a similar process to getting the original loan.

There are a few benefits to refinancing a title loan. The main benefit is being able to get a loan with a lower interest rates. Some title loans have very high interest rates. The ability to get a lower rate can save a significant amount of money.

A title loan refinance can be done both in person and completely online. Find the best title loan company and make sure they offer completely online title loans.