How much does a title loan cost? There are some articles attempting to answer this question, with a lack of information and some misconceptions about title loans in general. In this post we’ll provide some real examples to show how much different title loans cost.

The first misconception is that all title loans must be repaid in 30 days. This is not completely accurate as many states now offer monthly term loans with repayment terms of up to several years. Another misconception is that all title lenders charge triple digit interest rates and excessive fees.

While many lenders do, there are plenty of title lenders that charge significantly lower rates than others.

So what does a Title Loan really cost? This is a great question with a slightly more complicated answer than other loans. We provide three examples in this article, but first let’s go over what drives title loan costs.

Title loan costs depend on a number of different variables including interest rates, length of the loan, fees, and payment terms. So what are the interest rates and fees? Who decides these rates?

This is the most important question related to what a title loan really costs. The Answer: The lender determines the interest rates and fees.

All Lenders are not Equal

The Title Loan industry is one of the few where competition does not seem to affect costs. There are plenty of lenders charging the maximum allowable interest rate, regardless of how many other lenders operate in the same space.

There are, however, some lenders that do charge reasonable rates when compared to the large lenders. Now that you know you have a choice when it comes to getting a title loan, let’s discuss what title loans actually cost and why.

Title Cost Drivers:

There are three main drivers that will determine the cost of a title loan: Interest rates, fees, and loan term. The interest rate and fees will be directly connected to the lender you choose and will make the biggest difference.

Some lenders still operate with minimal investment in customer service and charge very high rates; and can charge the Maximum allowable rate. These are the types of lenders you will want to avoid if cost is an important factor to you.

Title Loan Interest Rates:

The biggest factors when determining how much title loans cost are the interest rate and loan term. Different states have different maximum rates and different lenders charge different rates. This is one aspect where Title loans are very different than payday loans. This is why it pays to do a bit of research and shop around for the right lender.

Interest rates can be as high as 300% APR, and well under 100% APR depending on the state and, most importantly, the lender. Most lenders that don’t disclose their rates charge the state maximum and/or very high rates.

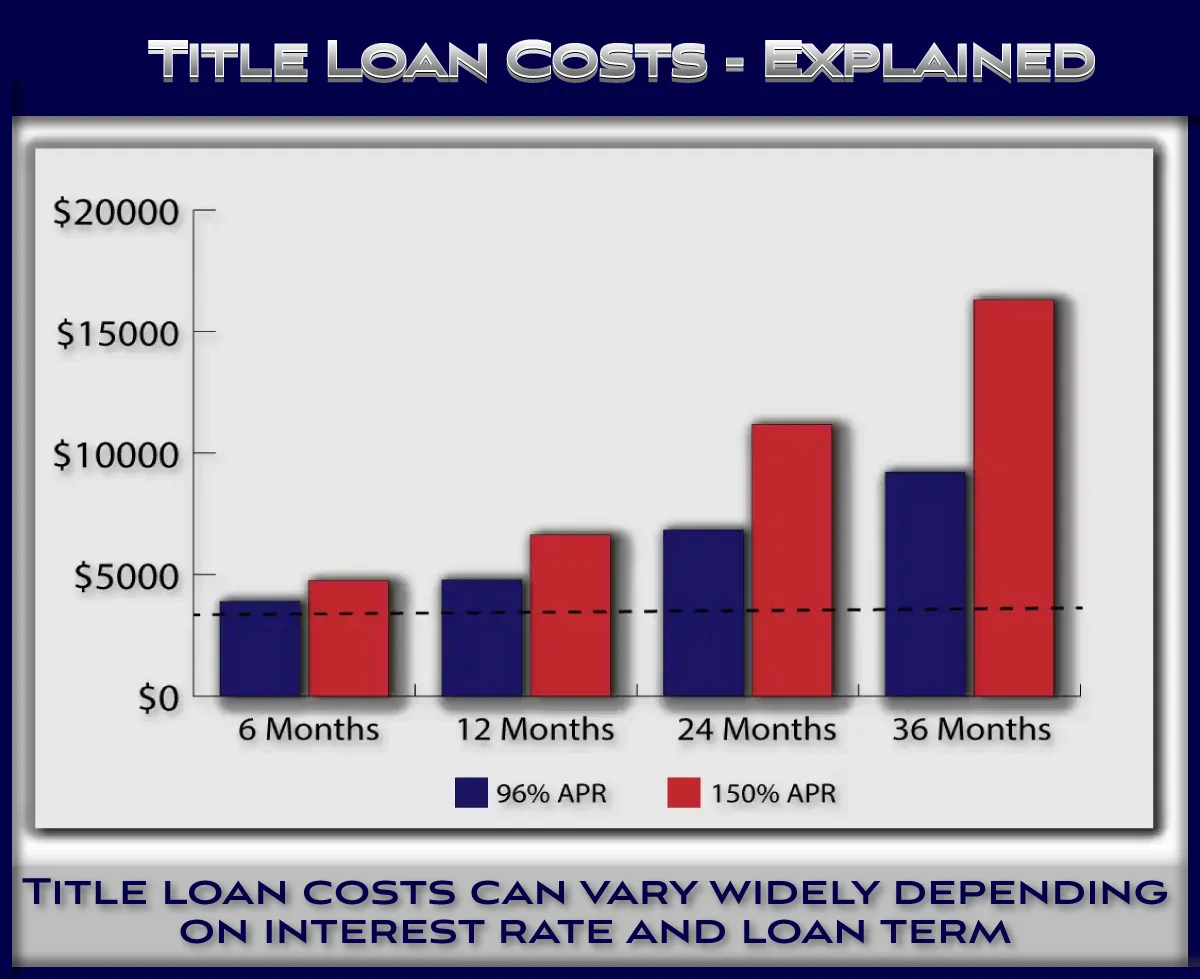

This makes a huge difference in the overall cost of the loan. For purposes of this post we are going to examine 12 month loans.

When you make a title loan longer, the cost increases significantly. This is detailed in the graphs here. Let’s look at three examples of the same $2,000.00, 12 month loan with a 96% APR, a 180% APR, and a 300% APR:

Title Loan Cost Example 1:

In the first example, we’re looking at a $2,000.00, 12 month title loan with a 96% APR. The monthly payment is $265.39 with a total finance charge, or the cost of the loan, is $1186.68. The total of payments is $3184.68 .

Title Loan Cost Example 2:

In the next example we are looking at the same $2,000.00, 12 month title loan with a 180% APR. The monthly payment is $368.96 with a total finance charge, or the cost of the loan, is $2427.54. The total of payments is $4427.54. This means it will cost you over $4,000.00 to borrow $2,000.00. This is also significantly more than the loan with the APR of 96%.

Title Loan Cost Example 3:

In the final example we are looking at the same $2,000.00, 12 month title loan with a 300% APR. The monthly payment is $536.90 with a total finance charge, or the cost of the loan, is $4442.74.

The total of payments is $6442,74. This means you will need to repay over $6,000.00 to borrow just $2,000.00. This is why it is critical to read to loan agreement and find out your costs. It is not unusual for title lenders to charge this much.

Title Loan Cost Example 5 – Calculate other Amounts:

We recognized the importance of transparency and developed our car Title Loan Calculator. The calculator allows you to enter any loan amount and term, and calculates the full payment schedule with a detailed breakout of interest and principal payments as well as totals. Use our car title loan calculator to determine the actual cost of a title loan.

Title Loan Fees:

Another cost driver for title loans are fees. Considering the amount of interest from the triple digit rate APR loans we looked at in the previous examples fees may not seem like a big deal.

You still need to take them into account, especially for 30 day Title loans. These loans are structured similar to payday loans with a fixed fee due at the end of the 30 days.

The APR related to these fees can be substantial and higher than 300% in some cases. Additionally, the entire principal is due back at the end of the 30 day period.

If you only pay the fee and “roll over” the principal for another month, this can add up quickly and you may end up paying for months without reducing your principal.

This means if you borrowed $2,000.00 and only make the fee payments, you may still owe $2,000.00 after making several payments.

Loan Terms:

The final major cost driver related to title loans are the loan terms. As mentioned in the previous section, single payment loans are structured very different than monthly term loans and can leave you still owing what you borrowed after repaying a significant amount.

Monthly term loans, on the other hand, apply a portion of every month’s payment towards the principal, ensuring you reduce the amount you owe every month. This can still be very costly if the APR is very high as we saw in examples 2 and 3.

Late Payments:

An important aspect of keeping title loan costs under control is making your payments on time. Paying late will not only add a late fee to your costs, but interest continues to accrue. For every day you are late, that is another day of interest that is charged on your outstanding principal.

A day or two won’t make a significant difference, but a week or two may. A portion of your payment is applied to your principal, and if that payment is late your principal is not lowered on the date in the payment schedule. This effect will add up if you make multiple late payments.

How to save on Title Loan Costs:

Car Title Loans are very different from PayDay loans with respect to being able to shop around for the best deal. Interest rates vary widely and finding a lender with lower rates will save you a significant amount of money on your next title loan.

It is possible to get a title loan that avoids some of the very high rates discussed here. First, take some time and do your homework by researching different lenders and getting multiple quotes. Find the lender’s disclosure and what a sample loan from them looks like.

For example, many larger lenders charge rates up to 300% APR. These are the very high rates we went over at the beginning of the post.

That means you may end up paying over triple what you borrowed with these lenders. These are the lenders you will want to avoid to get the best deal on a title loan.

Read their reviews from Ripoff Report and the Better Business Bureau. Learn from others’ experiences with lenders about which ones to avoid.

Make Additional Payments

Whether you find a decent lender or get stuck with a poor lender, one way to help save a significant amount of money on a title loan is to make early payments, additional payments, and pay more than your monthly payment. If you have a lender you don’t trust, make sure to get a receipt for every payment.

Making early payments has the opposite affect of the late payments discussed in the previous section and reduces your principal, which reduces the amount of interest that accrues.

How can I find a reasonable Lender?

The good news is there are some decent lenders now and it is not as hard to find a reasonable rate as it used to be. Simply take your time and do not rush to the closest lender assuming they are all the same, this couldn’t be further from the truth.

Remember, read the loan agreement in full before signing and make sure you are comfortable with the commitments.

Title Loan Costs – Trust your Gut

If you find yourself in the process of getting a title loan and something doesn’t feel right it probably isn’t. You have to trust your own intuition. Maybe you are asking the same question multiple times and not getting a direct answer.

Maybe you can’t get the details about how to make your payments or what the fee is for a late payment. Or, maybe you found a great lender and everything feels right. Do your research, read the agreement, and go with what works best for you.

Conclusion:

Car Title Loan costs can be reasonable or they can be excessive. This depends on how much you agree to pay for the loan, how long you keep it, and whether or not you make your payments on time.

If you are considering a title loan and aren’t sure if you make a good candidate, read our post on how to get a title loan. When shopping for a title loan remember you are the customer and absolutely have a say in the loan.