And why Title Loans are NOT Long term solutions.

Car title loans are generally more expensive than most other loans, there is no getting around that fact. Even the best car title loans usually cost more, sometimes significantly more, to repay, than many other loan types.

This doesn’t mean you can’t find an affordable car title loan. There are affordable title loans available should you decide one is the right choice for your specific financial situation.

Car title loans are short term solutions to immediate financial needs that cannot be met with other lower cost options. Car title loans are NOT long term solutions to financial problems. They should not be used as long term solutions.

In fact, car title loans are defined by Investopedia as short term loans, we concur with this definition. Additionally, many states require title loans to be short term loans.

Why? What will happen if you try to use a title loan as a long term solution? Then answer is simple. Title loans have high interest rates when compared to other forms of credit.

Amortizing a relatively high interest loan for a longer period of time exponentially increases interest charges. We provide some examples below to better illustrate this.

When this results in an excessively expensive loan it is more likely to cause a problem than solve one. The last thing any borrower wants to do is make a financial situation worse by trying to solve it.

This is why understanding how car title loans work and how interest is calculated is important.

Car Title Loan Costs

Car title loan costs, specifically title loans with monthly payments, like many online car title loans, are directly related to two variables:

1. The interest rate, and

2. The loan term.

It is common knowledge that getting a loan with a longer term will have a lower monthly payment. What may not always be communicated is the fact that this will also increase the total amount of interest paid.

As the loan term increases, so does the amount of interest accrued. With a very low interest loan, the amount may be tolerable or even negligible.

As the interest rate increases, the loan term has a much larger affect on the interest accrued over the life of the loan. The difference, which we will show below, can be staggering.

To fully understand, let’s take a look at three different car title loan amounts, amortized over 6 months, 12 months, 24 months, and 36 months.

Car Title Loan Cost Examples

The following are three examples of title loans for $1,000.00, $3,000.00, and $6,000.00. The two interest rates used to calculate these amounts are 8% per month (96% APR, which is low for a title loan) and 15% per month (180% APR, which is average for a monthly term title loan).

Considering some title lenders charge 20% per month or higher, the graphs shown below would be even more extreme with a rate higher than 15% per month.

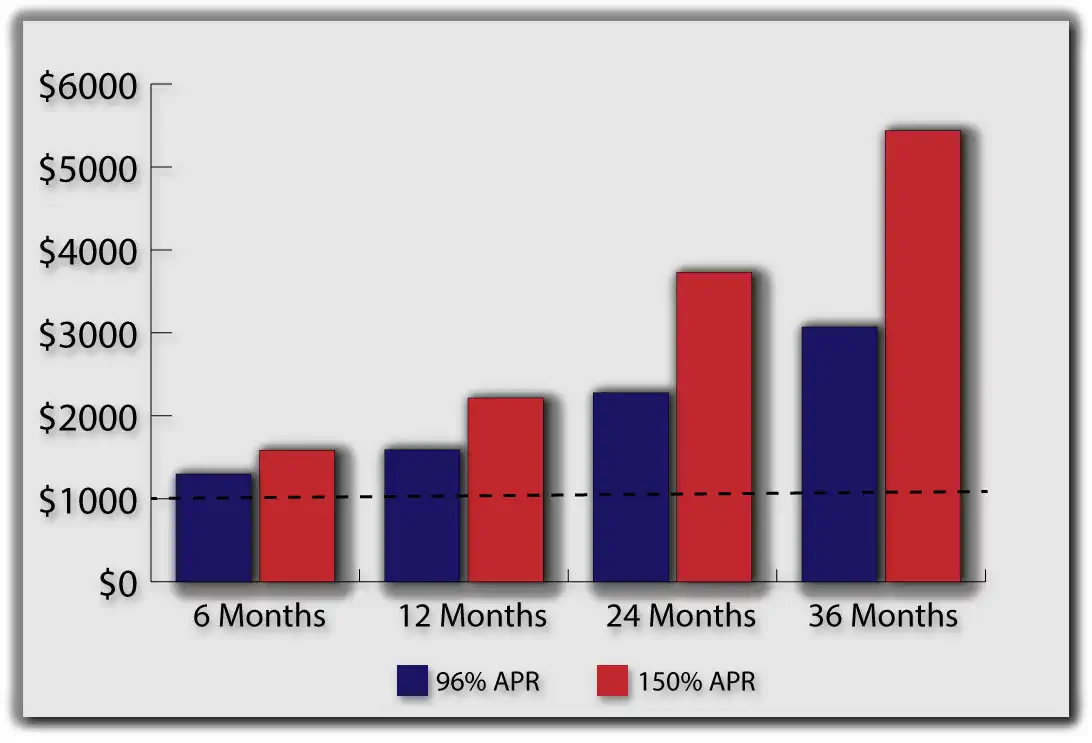

Cost Example 1 – $1,000.00 Car Title Loan

The figure below shows a $1,000.00 Title Loan amortized over 6 months, 12 months, 24 months, and 36 months:

As you can see, the cost of the loan increases significantly as you extend the loan. The difference is also more noticeable as the interest rate increases. This is the primary reason title loans are not long term financial solutions. It is not advisable to get a title loan for more than 12 months unless you can get a very low interest rate.

While a 24 or 36 month loan may lower your monthly payment, they will significantly increase the amount you will repay. A 48 month title loan is also shown as an example and is not advisable. Since most title loans do not have prepayment penalties, getting a 24 month loan and paying it off early is a better compromise than getting a longer loan.

As you can see from the graph, a $1,000 36 month title loan with an 8% per month interest costs over $3,000.00 to repay. And with a 15% per month loan it would cost over $5400 to repay (more than 5 times the loan amount). We would not recommend a 36 month (or longer) title loan for anyone.

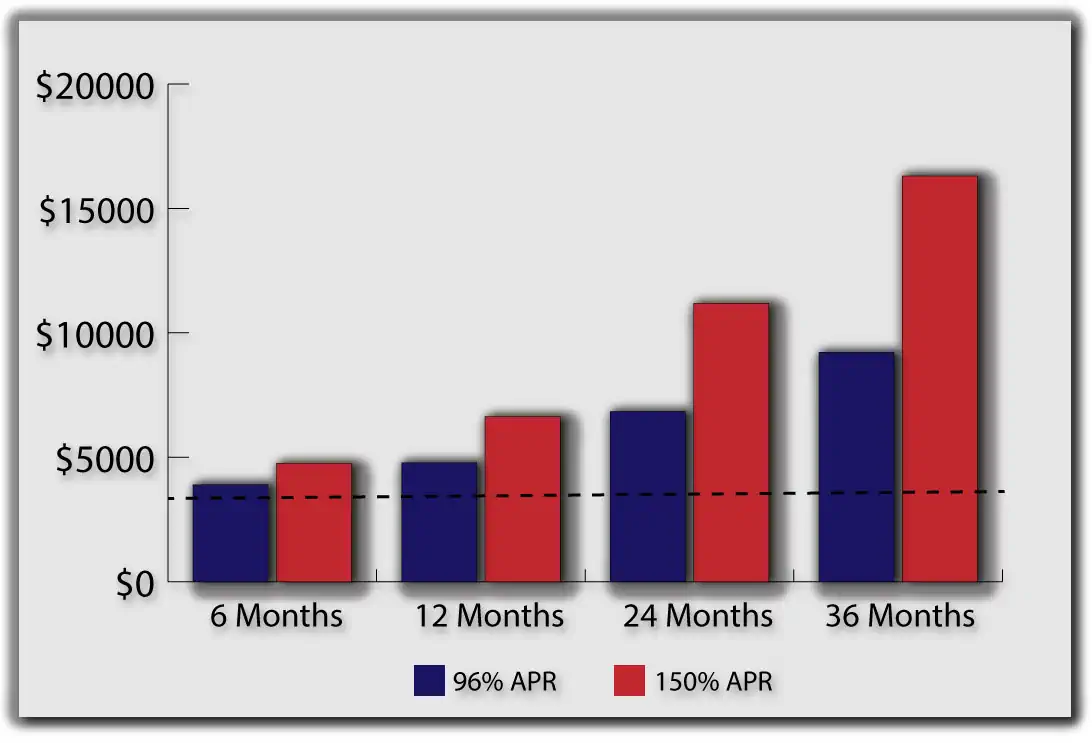

Cost Example 2 – $3,000.00 Car Title Loan

The chart below show a $3,000.00 car title loan with periods of 6, 12, 24, and 36 months.

As you can see, the results are similar to a $1,000.00, only even more significant because the loan amount is higher. The total repayment amount for a 36 month $3,000.00 loan, at 8% per month, is over $9,200.00.

With an interest rate of 15% per month a 36 month $3,000.00 title loan costs over $16,000.00 to repay. This is likely to cause a financial problem, not solve one.

Additionally, this amount may be worth more than the vehicle. Regardless, repaying over $9,200.00 to borrow $3,000.00 is excessive.

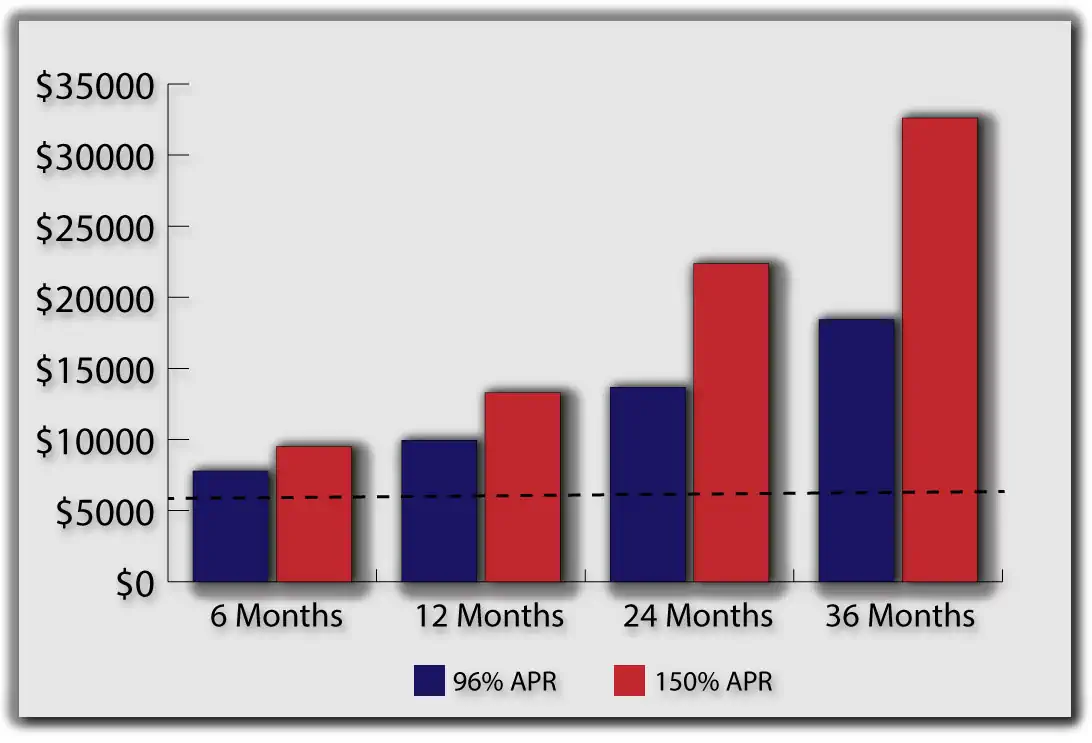

Cost Example 3 – $6,000.00 Car Title Loan

The graph below shows a title loan for $6,000.00 over 6, 12, 24, and 36 months. It shows the same pattern as the previous two loans.

As you can see, lengthening the title loan significantly increases the total interest paid. For a 36 month $6,000.00 title loan, the repayment amount is over $18,000.00 for an 8% per month loan and over $32,000.00 for a 15% per month title loan.

This would likely be the cause of a financial problem for anyone and in many cases is probably more than the car is worth. While the monthly payment for the 36 month title loan is lower, the repayment amount is excessive.

How to use the Information

When applying for your next title loan, remember these charts. Fast Title Lenders does not recommend any loan over 24 months.

Some online car title loan companies are now offering 36-48 month loans. Further, some have minimum terms of 24 months.

If a lender wants you to commit to a title loan for a long period of time, that goes against the definition of title loans being short term solutions. You may want to consider finding a lender offering better terms.

Regardless, make sure to fully understand the total costs of a title loan before signing an agreement. It is much better to walk away from a deal with excessive repayment terms than get stuck with it. This can lead to late or missed payments.

Mistakes you can Avoid with a Title Loan

A common mistake many borrowers make, with a title loan or any car loan, is focusing only on the monthly payment.

While it is important to be able to afford the monthly payment, it is more important to make sure the overall loan is affordable.

Always look at the total loan amount and make sure it is affordable. For car title loans, this means keeping the loan as short as possible.

Find a title loan company that specializes in car title loans and provides information readily. The closest car title loan company or the one nearest you is not always the best choice.

What is a Reasonable Title Loan Cost?

The cost of a title loan, and more specifically what borrowers consider reasonable, differs from borrower to borrow based on the benefit received from the title loan. Perform a title loan cost benefit analyses to determine what a title loan is worth to you.

If you are not sure how to perform a cost benefit analysis, we explain how to do so with examples when we answer the question ‘Are Title Loans Worth It?‘.

Also, as a general rule, if it costs significantly more interest to repay the loan than the original principal, that is likely unreasonable unless you are receiving a significant benefit from the loan.

Even the best title loans can be expensive, especially with longer terms.

What is a Reasonable Title Loan Term?

This is another subjective question that depends on your unique situation. It is important to note that car title loans are not meant to be long term solutions and the length of the loan varies by state. Different states have different views on what the maximum and minimum term for a title loan should be.

Some states have no limits. To find out if your state allows title loans and has a maximum check title loan laws by state. A reasonable loan term should provide enough time to repay the car title loan, but be short enough to avoid excessive title loan costs.

As we’ll see later, loan terms longer than 12 months begin to accrue excessive interest. To help show the effects the loan term has on the interest charges for an amortized title loan we created three graphs with three different loan amounts.

How Long are Car Title Loans?

Car Title Loans vary in length from 30 days to several years. Finding the optimal car title loan term, and answering the question “how long should a car title loan be?”, is a good idea prior to applying for one.

Conclusion

Car title loans are meant to be short term loans to cover funding emergencies. Many online title lenders today are making longer term loans. It is a great way for the lender to make money by amortizing a high interest loan for several years.

Unfortunately for the borrower, this means repaying many times the original amount borrowed. That is not a reasonable loan. If you already have one of these loans consider refinancing your title loan to lower your payments.

As you can see from the data, the longer the loan, the more interest. Having to repay $18,000.00 or more to borrow $6,000.00 is not a financial solution. This is why title loans are not long term solutions.

Try to find a lender that offers low interest title loans and keep the term short. Make sure to choose the best title loan for your situation.

Always read the loan agreement in full and keep the loan term as short as possible. If you do end up getting a title loan with a term longer than a year make sure there is no prepayment penalty and try to pay the loan off as soon as possible.