How long is a Title Loan? Perhaps a better question is “How Long should a Title Loan be for?”

Car title loans are often thought of as very fast and often very short term. With the addition of more online title loans many include longer loan terms that have monthly installments.

Some lenders are making these loans with longer terms (lengths), which is not necessarily a good thing. Longer loans mean more interest payments. In some cases this can result in an excessive loan.

Car Title Loan Length in Online Title Loan Articles

Unfortunately finding accurate and factual information about car title loans online can be challenging and confusing. Many of online articles about title loans that are written and published by title loan competitors (like Credit Card related companies) say that title loans are 30 days long with very high (300% APR) interest rates.

The truth is that this is simply not accurate for many online title loans. This can be confusing for those that are looking for a title loan online.

Conflicting information is prevalent and causes confusion. We recommend finding several sources and checking everything you read.

It is unfortunate that you can’t trust companies but the fact is they make money when people get credit cards and not title loans.

With that said title lenders aren’t exactly know for their honesty in advertising either which certainly doesn’t help with confusion.

And that is what most blog posts are, a form of advertising. The fact is title lenders and their competitors like the credit card industry often publish articles with conflicting information.

They publish what they want borrowers to think that benefits them and their advertisers.

How Long are Car Title Loans?

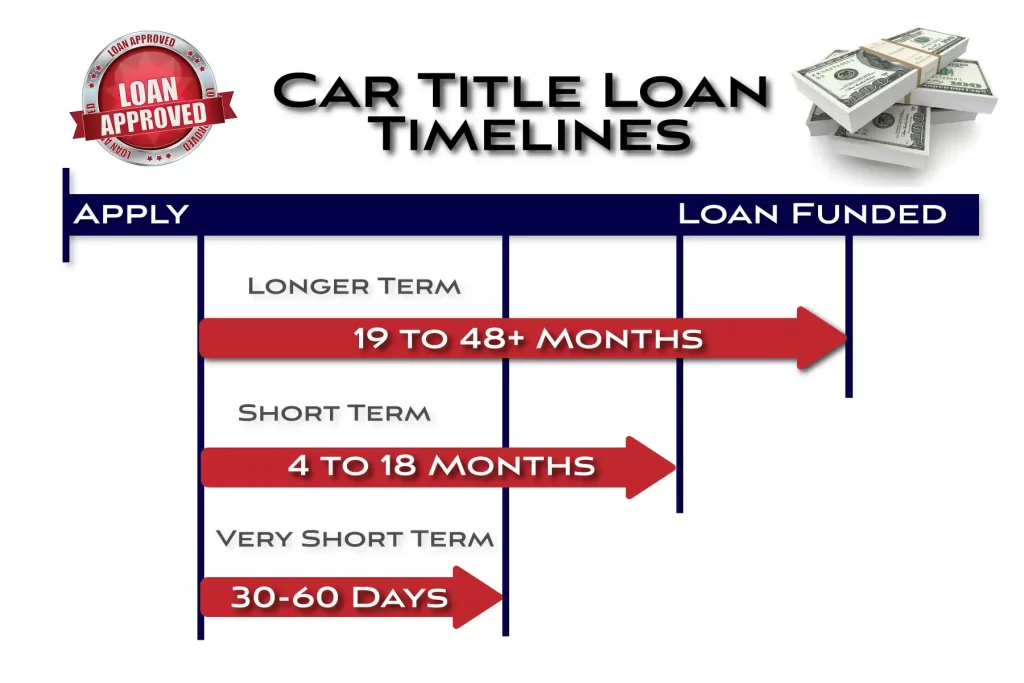

The truth is car title loans have lengths that vary from 30 days to several years. Car title loan lengths can be categorized as very short term, short term, and longer term.

By definition title loans are meant to be short term loans. We say meant to be because there are some online title loan companies making longer term title loans.

This is not advisable and the total loan cost can get excessive when any title loan exceeds 12-18 months. This is illustrated in the graphs in our title loan costs article and in the chart below.

The reason is simple: Amortizing a high interest loan for a long term is extremely costly. As shown in the example below it can cost 4, 5 and even more times the original principal to repay a long term title loan.

We categorize car title loans using three high level terms:

- Very Short Term Loans

- Short Term Loans

- Longer Term Loans

Very Short Term Title Loans

There are very short term title loans is some states. These are typically for 30 days with the full amount due by the 30th day. These loans are usually for a smaller amount and are also know as title pawns in some states. Car title loans in Miami Florida, for example, have 30 day repayment periods.

As mentioned, the state you reside in will dictate what length title loan you can get. The laws vary from state to state and some states have minimum and maximum terms.

Very short term loans usually have a high interest rate and typically only start to cause problems when you roll them over. Rolling over a title loan can lead to excessive costs.

Short Term and Longer Term Title Loans

The next category of loan length is short term and longer term. We define them with the following:

| Term: | Length: |

| Short Term | 4-18 months |

| Longer Term | 19-48+ months |

By definition both of these loan lengths would be for monthly installment loans.

Monthly Installment Title Loans

Both short term and longer term title loans have monthly installments. These are similar to other car loans where you make monthly payments to pay down the principal over time.

It is important to note that car title loans are not meant to be long term loans. They are defined as, and designed to be, short term solutions. This if for good reason. The interest rate for a title loan is usually higher than for other monthly installment loans.

Title Loan Amortization

When a loan is broken into monthly installments this is called amortization. There is a formula for determining the monthly payment for any loan that requires the principal loan amount, interest rate, and loan length.

With that said, there is a cost to extending a title loan beyond 6 months. This cost increases significantly as you extend it. Learning how title loan interest works helps understand this.

Reducing the Monthly Payment

The main reason for extending a title loan beyond 6 months is to reduce the monthly payment to make the loan affordable. The goal should always be an affordable title loan that solves a financial problem.

The risk with extending the loan to reduce the monthly payment is that doing so increases the total loan cost. In fact, extending any title loan beyond 24 months significantly reduces the total loan cost without significantly reducing the monthly payment.

In fact, there is a point where increasing the loan term does not make any sense. It is critical to understand where that point is before you sign a loan agreement.

No Pre-Payment Penalty

Some online title loan companies are providing loans that last for 3-4 and even more years. These loans will undoubtedly have excessive total loan costs. Always make sure that any title loan agreement you sign has no pre-payment penalty.

This means if you do happen to get stuck in a longer loan with excessive total loan costs at least you can pay it off early. There is more to finding the best online title loan including researching the lender.

What is the Optimal Title Loan Length?

To answer this question we need to know what loan length will result in:

- An affordable monthly payment

- A reasonable total loan cost.

Find a balance between the length of the loan, monthly payment, and total loan costs. To get an idea of what some title loans that are longer than 12 months, see some examples of what title loans cost.

Prepare for your loan and decide how much you need to borrow. Value your vehicle and make sure the value supports the amount you want to borrow. Then, use the title loan calculator to find the optimal payment and total loan cost.

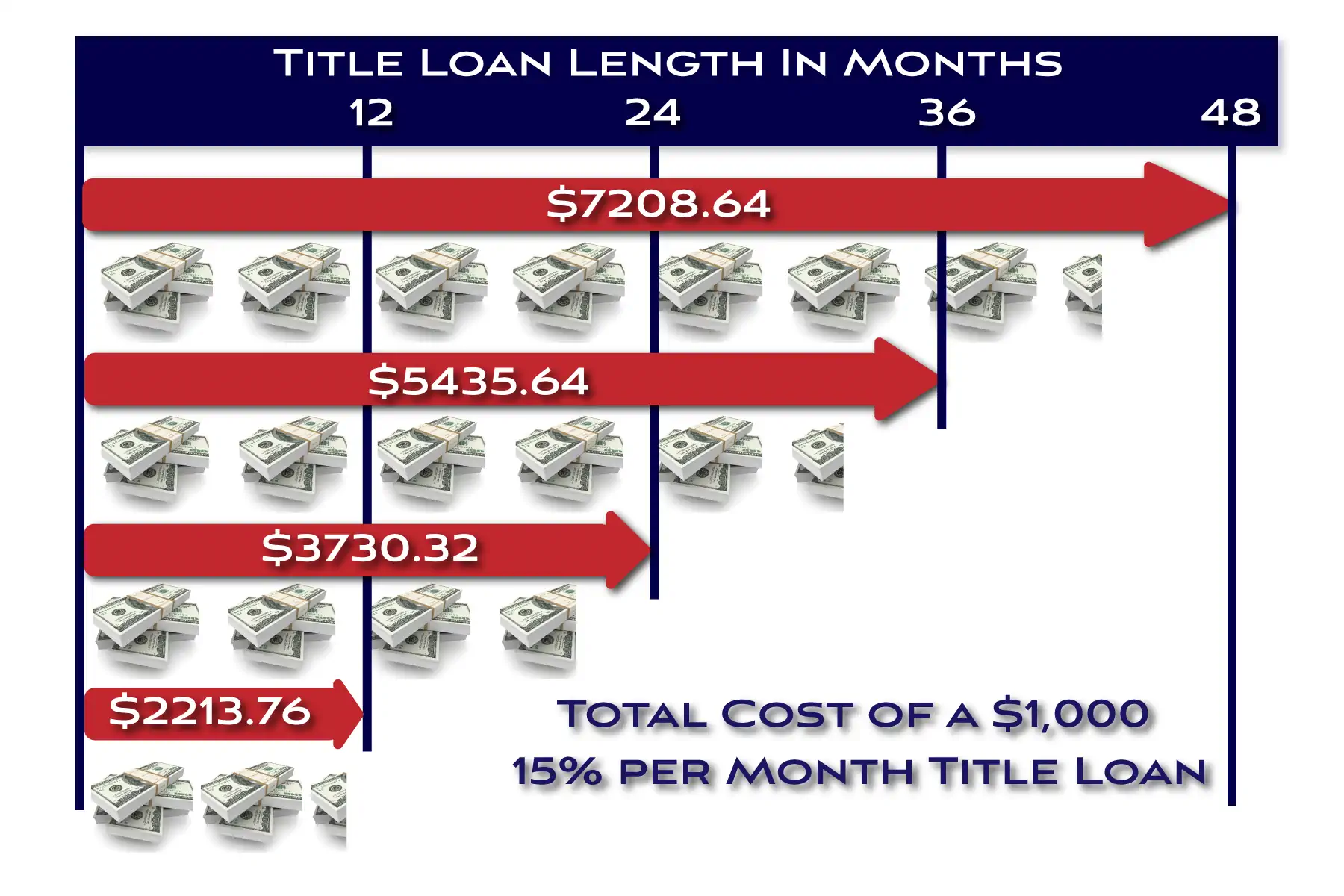

Car Title Loan Cost Example – 12- 48 Month Loan

To illustrate the point about keeping title loans short term loans, the following shows the total loan cost for a $1,000 loan with a 15% per month interest rate. The loan is amortized over 12, 24, 36, and 48 months.

As you can see the costs get significantly higher the longer the loan is. If you make only the minimum monthly payment on a 48 month loan, the total loan costs exceed $7,000.00, or seven times the original principal. This is not a reasonable loan and should be avoided.