Title loan interest can be confusing, but it doesn’t have to be. You just need to understand a few concepts first to understand how title loan interest works.

Learning how title loan interest works and how it is calculated, does make the loan, and more specifically, the payments, much easier to understand.

Title Loan Interest is Similar to Other Loans

Title loan interest works similar to other loans. Any simple interest loan that is amortized (don’t worry, we’ll explain amortization shortly) works the same way.

If you are considering a title loan, this can also help you decide whether or not one is right for you. Additionally, understanding how title loan interest is calculated makes it easier to predict the costs of the loan over the term.

Important Topics

To gain a full understanding of title loan (or any loan for that matter) interest, in this post we will cover several topics:

- Two types of Title Loans – Single Payment and Monthly Payment

- How Title Loan Interest Works

- Monthly rate versus Annual Percentage Rate (APR)

- How to calculate Interest (for any loan)

- Loan Amortization (for any loan)

- Truth In Lending (TIL) Statements

Two Types of Title Loans

The first simple concept to understand is there are two types of title loans. The type available to you will depend on which state you live in.

The first is a title loan with one single payment, which is due at the end of the loan term. The second is a loan with monthly installments (payments) for a period of months.

Single Payment Title Loans

Title loans with single payments require the full loan amount, plus interest and fees, to be paid in full by the due date. These loans typically have a term of one month or 30 days. These are also sometimes called Title Pawns.

Interest for these types of title loans is very easy to calculate because there is only one payment. Let’s look at an example to illustrate this.

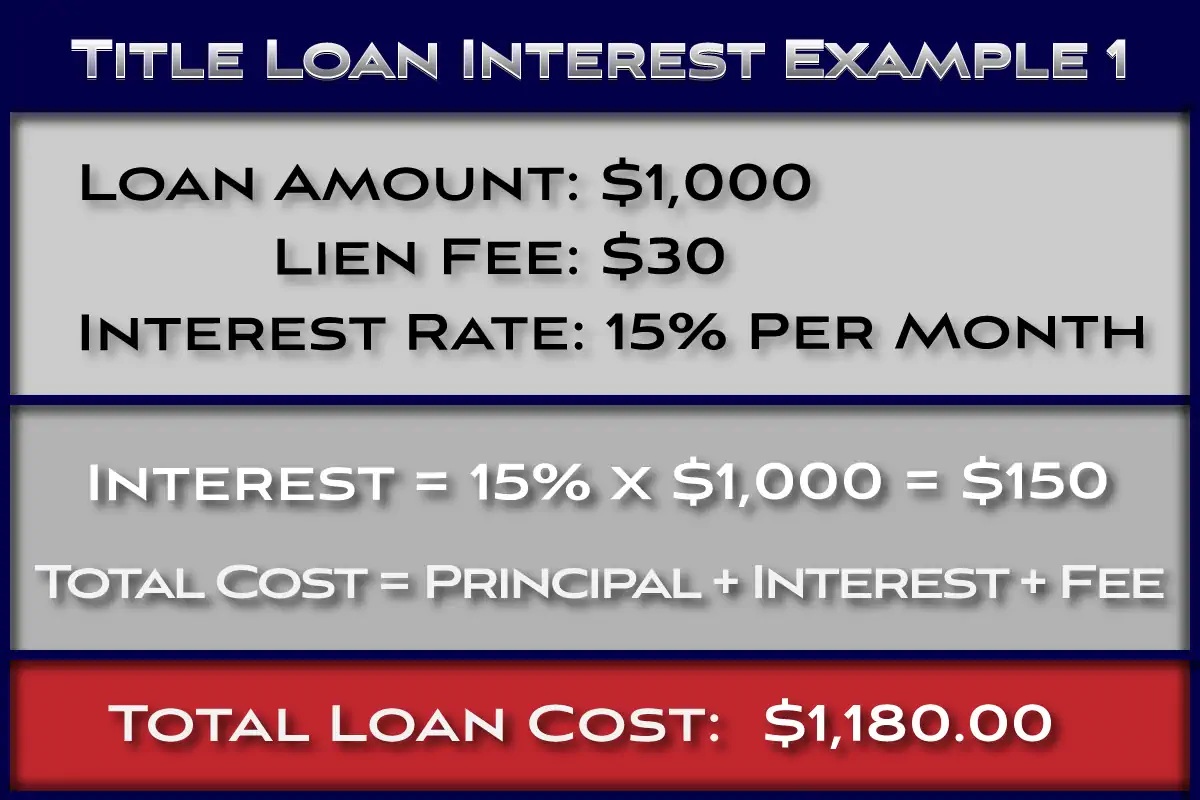

Single Payment Title Loan Example

For example, let’s say we borrow $1,000.00 for one month at a Monthly Rate of 15% with a Lien fee of $30. The loan is due in one month, and we are required to pay the loan in full.

Because there is only one payment, there is no need to amortize the loan (more on amortization later). We simply need to figure out how much we will owe at the end of the one month.

To calculate the interest we simply multiply the Principal Amount times the Monthly Rate plus the Lien Fee. We have the principal amount (the $1,000.00), we have the monthly rate (15%), and we have the Lien fee ($30). So the interest accrued during the loan term is:

$1000.00 x 15% = $150, and the Lien fee is $30, bringing our total of interest and fees to $150 + $30 = $180. This means we will need to repay the principal amount, plus the interest and fee, by the due date.

Paying Single Payment Loans Early

What if we want to pay the loan before the due date? How do we know how much interest is due if we pay the loan 10 days early? Or 15 days early?

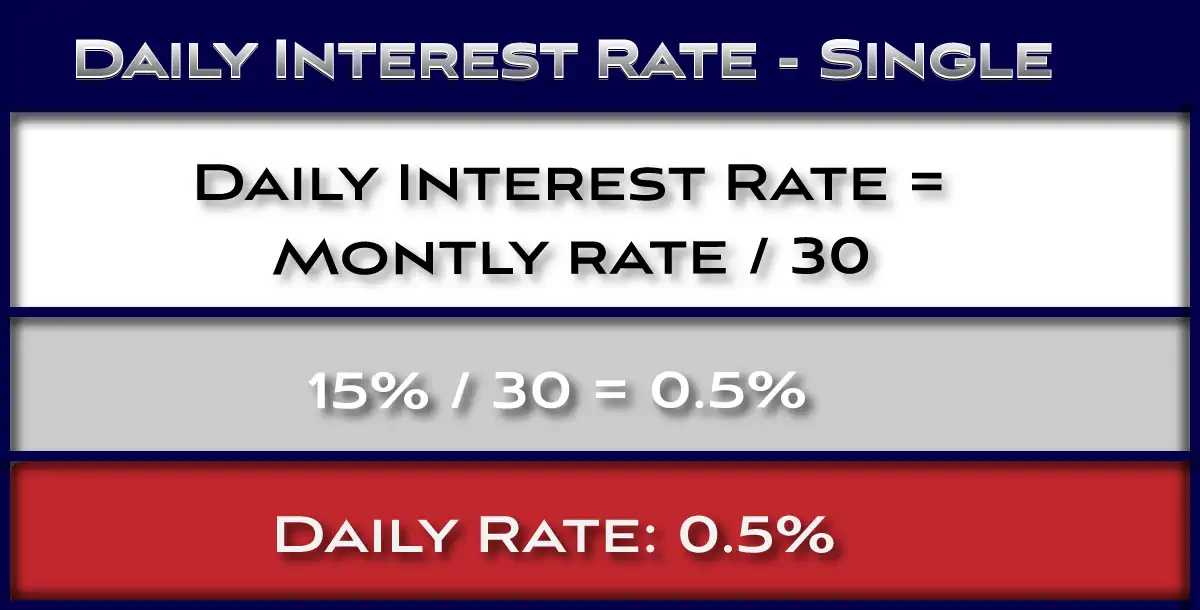

To find out how much we would owe if we wanted to pay the loan early we need to get the daily rate of interest. The daily rate is simply the rate at which interest accrues each day. This lets us calculate the amount we will owe on any given day between when we open the loan and close it. This assumes there is no pre-payment penalty.

To get the daily rate for a single payment loan with a period of 30 days, we simply divide the Monthly rate by 30. We have the monthly rate of 15%, do the daily rate is:

Daily rate = 15% / 30 = 0.5%. Now that we have the daily rate, we can easily find out the interest that is due on any given day if we want to pay our loan early.

If we pay the loan after 20 days, instead of owing the $150 in interest, we will owe the Principal Amount times the Daily Rate times the Number of Days. So:

Interest = $1,000.00 x 0.5% x 20 = $100. If we repay the loan in 20 days instead of 30, we will owe $100 in interest instead of $150. We can use this same formula for any number of days.

Using the Daily Rate

We can also take the daily rate and multiply it by the Principal Amount to get the amount of interest that accrues each day in dollars. For our example loan our Principal is $1,000.00 and our Daily Rate is 0.5%. $1,000.00 x 0.5% = $5.00. This means each day the loan is accruing interest of $5.00. So, each day we keep the loan, we owe another $5.00.

Using the daily amount we can quickly and easily calculate how much interest we will owe on any day. After 12 days, we will owe 12 x $5 = $60. After 17 days we will owe 17 x $5 = $85. Now that we know how to calculate the interest accruing on our loan there will be no surprises as long as we make our payment on or before the due date.

Monthly Installment Loans

The second type of title loan is one that has monthly installments; sometimes called monthly term loans. Interest works the same for these loans as it does for other monthly installment loans. Think of a new car loan or a mortgage.

The remainder of this page is dedicated to explaining how interest works for title loans with monthly installments. The process of breaking a loan into equal monthly payments is called amortization.

You don’t need to memorize the formula, but it does help to understand how amortization works.

Similar to the single payment title loans, monthly installment title loans also accrue interest at a daily rate. The difference is a payment is made each month, so the principle is reduced each month.

As a result, if we want to get the daily interest amount in dollars we need to recalculate it every month.

How Title Loan Interest works:

Title loan interest works the same way any other simple interest monthly installment loan interest works. So at a very high level, you pay a premium to the lender to borrow money. As a result, there are two key factors that determine the premium you pay and therefor the cost of a loan:

- The Interest Rate – the higher the rate, the higher the daily cost.

- The Term – the length of the loan. The longer the term, the higher the cost.

The combination of these two numbers determine the cost of borrowing. As each one of these increases, the effect on the total loan cost is increased. If the both increase simultaneously, the cost increases at a very high rate. In another post about the true cost of title loans we showed what happens when you extend a title loan for several years.

For this reason, title loans are meant to be short term loans. More on that later.

Is Interest Complicated?

Lenders, in all industries, tend to make things more complicated than they need to be. When we learn how interest is calculated we can better understand our loans; both future and current.

This is applicable to loans of all types. A few key points to help clarify how title loan interest works:

- Car title loans in several states, including many online title loans, are monthly term loans with simple interest. These loans are just like many other monthly term loans (car loans, mortgages, etc.). There are, however, single payment title loans. These have one payment due in full at the end of the loan term.

- Title lenders cannot charge you interest in advance, and can only charge interest on the outstanding principal balance. This is true of most loans.

- Title lenders usually quote the Monthly interest rate, and not the typical Annual percentage rate (APR).

- There are maximum rates lenders can charge, however no minimum, so you can ask for a lower rate.

- Truth In Lending statements are usually required for all loans. If you don’t want to learn how to calculate interest, at least learn how to quickly interpret these statements. It will definitely help next time you get any kind of loan.

Monthly Rate versus Annual Percentage Rate (APR):

The first step in learning how title loan interest works is to understand the difference between the monthly interest rate and the Annual Percentage Rate (APR). Title lenders typically (not always) quote their rates using monthly interest terms.

There are a couple of reasons for this. When title loans were first offered they were typically 30 day loans, so quoting the interest rate in monthly terms made sense. As we saw from our Single Payment Loan example, it was fairly easy to calculate the interest accrued using the monthly rate.

The other reason for sticking with Monthly rates instead of APR is simple: most borrowers would not agree to a 250% plus APR loan, but a 22% a month loan sounds OK. 22% a month is actually 264% APR.

Step 1: Estimating the APR

Before we can start to illustrate how interest works with a loan with monthly payments we need to know the APR. If the lender provides that, great, move on to Step 2 below. If you only have the monthly rate you will need to convert it to the APR.

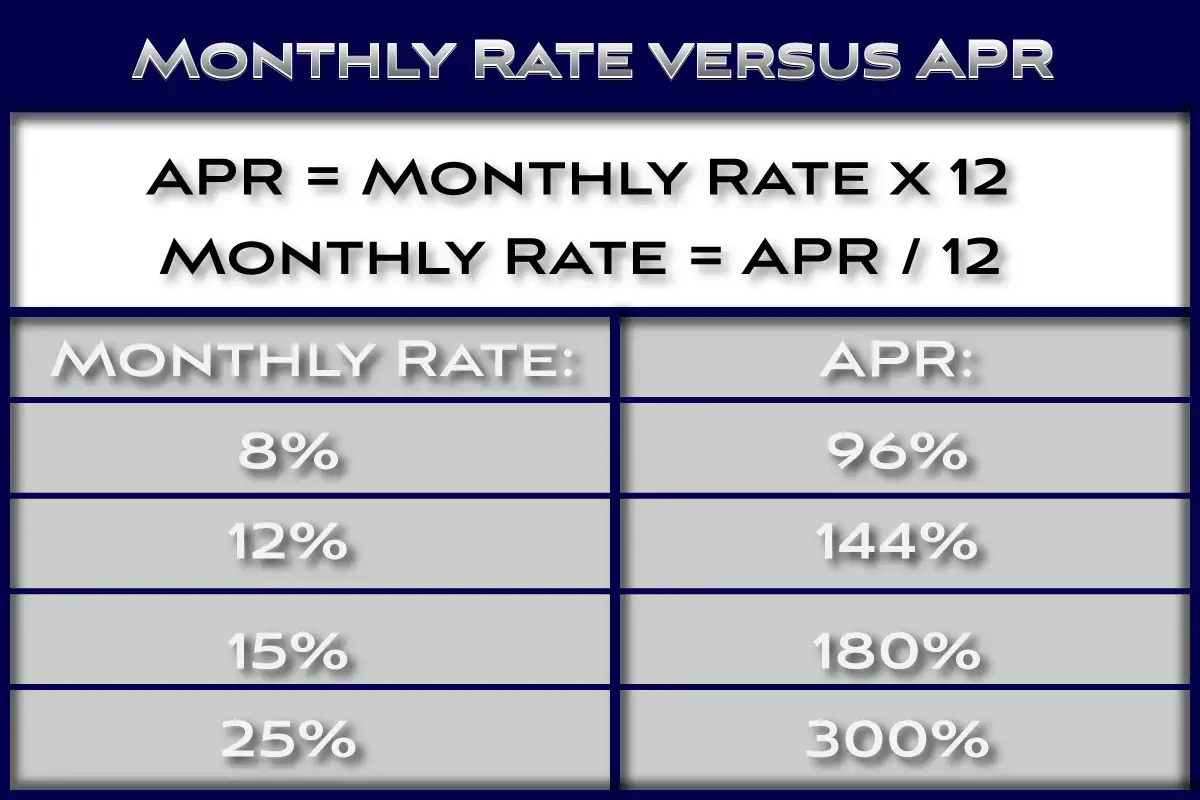

This part is fairly simple. Take the monthly rate and multiply by 12 (for 12 months in a year). For example, a loan with a monthly rate of 8% has a 96% APR (8 x 12 = 96). A loan with a monthly rate of 20% has an APR of 240% (20 x 12 = 240).

Similarly, a loan with a 180% APR has a monthly rate of 15% (180 / 12). It is important to know which rate (Monthly or APR) the lender quotes when comparing loans. You need to compare the same type of rate to the same type of rate.

Step 2: How to calculate Title Loan interest:

A common mistake when calculating title loan interest is multiplying the APR times the amount borrowed. This is the method many people use to estimate interest for any loan. It does not work for loans with monthly payments.

In fact, some title lenders actually explain interest using this method. Here is why it is not accurate:

Common Mistake: Multiplying APR by Amount Borrowed

So let’s use the same $1000 loan as an example. Instead of 30 days, we are going to look at a 1 year loan with 12 monthly payments. Our Monthly Rate is 15%, so the first thing we need to do is get the APR. We’ll multiply 15% x 12 and we have 180%.

If we multiply $1,000 by 180% (1.8), we get a total of $1800. This makes our total loan cost $1,800 using this method.

We know from using the title loan calculator that a 1 year, $1000 loan, with a monthly rate of 15% has a monthly payment of $184.48 and total cost of $2213.76. The interest for the full year is $1,213.76. This is significantly less than the $1,800 we got when we multiplied $1000 by 180%.

What went wrong and why can’t we multiply APR times the amount borrowed?

The reason we can’t simply multiply APR times the amount borrowed is we are making payments each month. These payments are reducing the principal loan amount and therefore reducing the amount of interest accruing each days.

If we made no payments for a full year and one single payment at the end of the 1 year, then that formula would work. The problem is very few (if any) loans are structured this way. To learn how title loan interest works, we will need to understand loan amortization.

Step 3: Loan Amortization:

When a loan is broken into equal monthly payments or installments, to calculate that monthly payment the loan is amortized. Basically, this means you make the same monthly payment every month, only the amounts that go towards principal and interest change every month.

You only pay interest on the outstanding principal balance. When you make your first payment, part of that payment is applied to interest, and part to principal.

The part that goes towards principal reduces your outstanding principal balance, and the month 2 interest accrued is less than month 1.

For our example, we will use a 12 month $1000 loan at 8% per month (96% APR). Let’s take a look at how this works:

Loan Amortization Example:

A $1000.00 loan for 12 months, with a monthly rate of 8% (96% APR), has a monthly payment of $132.70.

First, we calculate the interest accrued that month. Our monthly interest rate is 8%, and our outstanding principal is $1000. To calculate the interest we accrued over the month, we multiply $1000 by 8%. Remember when using a percentage in an equation to divide it by 100. 8/100 is 0.08.

$1000 x 0.08 = $80.00. A summary of the equation is:

Interest Accrued = Principal Balance x Monthly Interest Rate = $1000.00 x 8% (0.08) = $80.00

So over the first month we accrued $80.00 of interest. Since our monthly payment is more than $80.00, a portion of the payment is applied to the principal, reducing our outstanding loan balance. To figure out how much, we subtract the interest amount from the monthly payment:

$132.70 – $80.00 = $52.70. A summary of the equation is:

Principal Payment = Monthly Payment – Interest Payment = $132.70 – $80.00 = $52.70

So for the first month’s payment $52.70 is applied to the principal balance.

$1000.00 – $52.70 = 947.30. Summarized as:

Principal Balance = Beginning Principal Balance – Principal Payment = $1000.00 – $52.70 = $947.30

Now that we have made our first monthly payment, the current outstanding principal balance is now $947.30, lower than the original loan amount of $1000.00.

Interest for Month 2:

So now that we see how the first month’s payment is applied to principal and interest, let’s take a look at month 2. Remember, interest accrues on the current principal balance. For month 2, the principal balance is now $947.30. Because this is less than the $1000 we started with, the interest accrued will also be less.

We use the same process to calculate the interest for Month 2.

Our principal balance times the monthly interest rate: $947.30 x 8% = $75.78

This is less than month 1, and our monthly payment is the same, so the amount of our payment that will be applied to the principal balance is:

Monthly Payment – Interest = Principal Payment;

which gives us: $132.70 – $75.78 = $56.91

This means $56.91 from our month 2 payment is applied to our outstanding principal balance, giving us:

Principal Balance = Current Principal – Principal Payment: $947.30 – $56.91 = $890.39

Interest for Month 3:

Now our outstanding principal balance is down to $890.39 after making 2 month’s payments. This means the interest accrued for month 3 will be less than month 2, and the amount applied to principal will be more than month 2. Using the same equations we get:

Principal Balance: $830.39

Interest Payment = Principal Balance x Monthly Interest Rate = $830.39 x 8% = $71.23

Principal Payment = Monthly Payment – Interest Payment = $132.70 – $71.23 = $61.46

Principal Balance = Beginning Principal Balance – Principal Payment = $890.39 – $61.46 = $828.93

Interest for Months 4 – 12:

To calculate Month 4 we would do the same thing using $828.93 as the principal balance. Each month we are reducing our principal balance, which reduces the amount of interest that accrues, increasing the portion of our payment that is applied to the principal. This process continues until the principal balance is $0.00. This is the reason you cannot simply multiply the APR times the Loan amount.

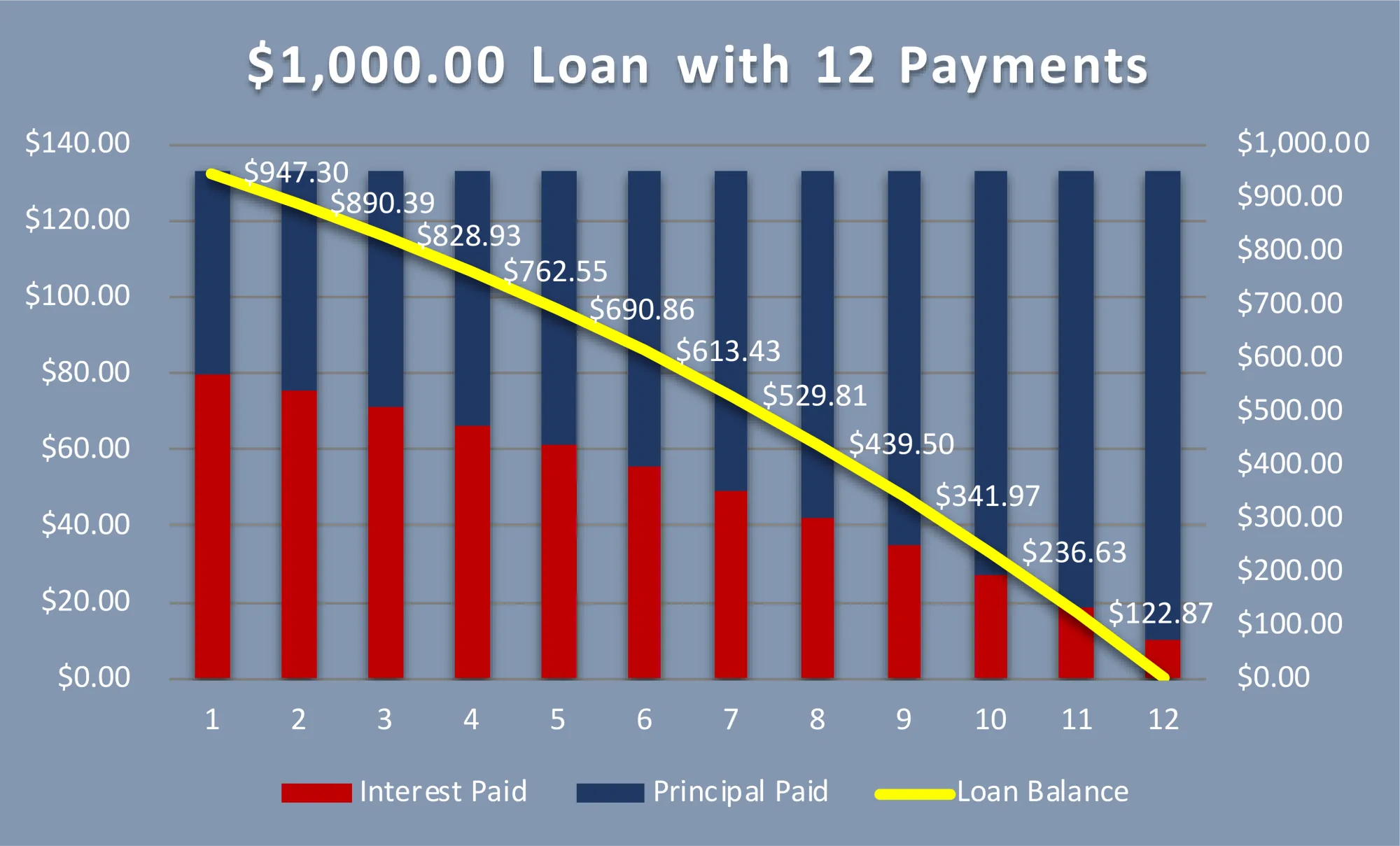

Lets take a look at the full year. Notice how the interest for each month decreases, and the amount applied to principal increases:

Full Year Title Loan Amortization:

The full amortization table for the $1000.00 example loan looks like this:

| Month | Payment | Interest | Principal | Balance |

| 0 | $1,000.00 | |||

| 1 | $132.70 | $80.00 | $52.70 | $947.30 |

| 2 | $132.70 | $75.78 | $56.91 | $890.39 |

| 3 | $132.70 | $71.23 | $61.46 | $828.93 |

| 4 | $132.70 | $66.31 | $66.38 | $762.55 |

| 5 | $132.70 | $61.00 | $71.69 | $690.86 |

| 6 | $132.70 | $55.27 | $77.43 | $613.43 |

| 7 | $132.70 | $49.07 | $83.62 | $529.81 |

| 8 | $132.70 | $42.39 | $90.31 | $439.50 |

| 9 | $132.70 | $35.16 | $97.53 | $341.97 |

| 10 | $132.70 | $27.36 | $105.34 | $236.63 |

| 11 | $132.70 | $18.93 | $113.76 | $122.87 |

| 12 | $132.70 | $9.83 | $122.87 | $0.00 |

| Totals | $1,592.34 | $592.34 | $1,000.00 |

The graph of the loan looks like this:

From the graph we can see we pay most of the interest in the first half of the loan. This is how loan amortization works. As the interest accrued decreases the principal decreases faster.

This is what all those ‘Pay off your mortgage with this simple trick’ sites are. Simply an explanation of loan amortization. In fact, you can use these same techniques to pay off your title loan fast.

Keep in mind that this title loan interest example is related to monthly term loans, like we have in Virginia. Some states have 30 day loans, interest only payments, or other rules.

Make sure to check the laws in your state. To calculate another loan with a different amount and/or interest rate use our car title loan estimate calculator.

A transparent and Reputable Title Loan Company:

As our goal to be the best title loan company transparency is important to us. The purpose of the information on our site is to educate car title loan customers, and anyone wanting to learn about title loans so that they can save on their next loan.

Understanding how title loans work is essential to getting the best deal on a loan, and making sure you don’t get stuck with a loan you cannot repay. Too often we hear about customers with excessive interest loans. Our goal is to inform customers so they can make a better decision.

Daily Interest Accrual Adjustments:

The exact amounts may differ slightly from the above example for a few reasons. The first is the exact day the payment is made. Lenders generally accrue interest daily, so if you make a payment early or late, this affects the amount of interest that accrues.

Additionally, there may be a very small difference based on whether the lender uses a 365 or 360 day year. Finally, there are fractions of a cent that get rounded and can slightly increase or decrease the numbers. For the purpose of understanding how title loan interest works, we assume these variations are very small.

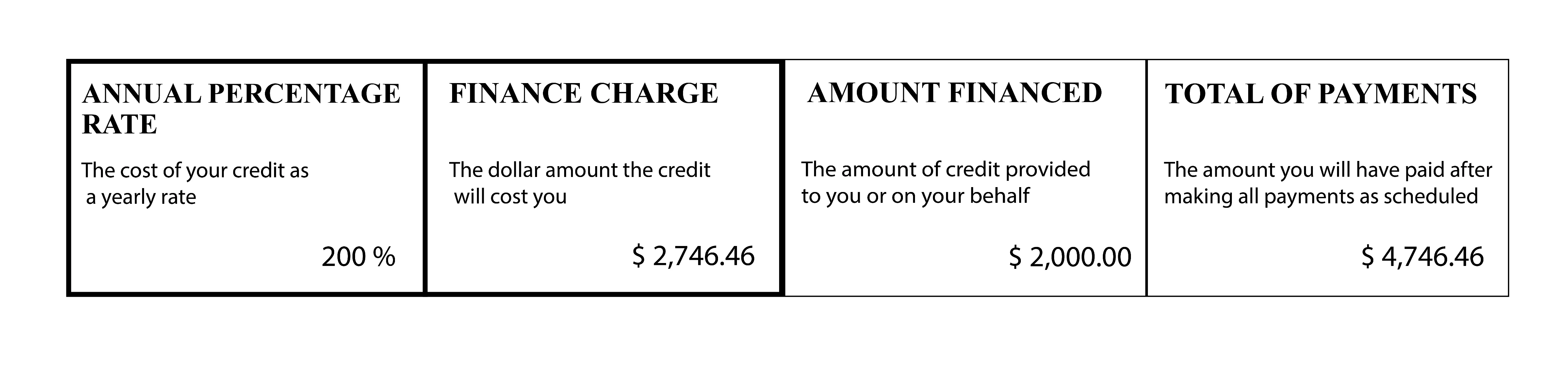

Truth In Lending to Compare Loans

Truth in Lending statements are required by Federal law. This was designed to help consumers understand exactly what a loan would cost prior to entering into the agreement.

Title lenders in most states are required to include TIL statements in the loan agreement; usually on the front page. They include a table with four cells on the first line. The first two have a thick outline to stand out.

Box one is the Annual percentage Rate (APR) of the loan.

Box two is the Finance Charge; this is the amount of interest you will repay.

The third is the Loan Amount (how much you borrowed).

The fourth is the Total dollar amount you will have paid. This assumes you make every payment on time with no early payments.

Most lenders are required to provide you with a TIL statement in the same or similar format; if they don’t, you are allowed to ask for one. Learn how to read a TIL and use one to shop for a title loan.

Conclusion:

Car Title Loan interest charges make up the majority of the costs associated with a car title loan. Once you understand how interest is calculated, charged, and credited, it definitely makes it easier to understand how title loans work. You can apply this to online car title loans as well.

If you are shopping for a title loan, make sure you make a good title loan candidate, We cover this, and many other title loan related topics in our complete guide on how to get a title loan. Learn more about Fast Title Lenders and our history with title loans.