A “Truth in Lending Statement” is a statement informing consumers of the actual cost of credit. This is important because it allows you to compare the actual cost of different types of credit, different lenders, and different loan types.

Understanding the Truth in Lending Statement

Usually, on the first page of your loan agreement, you will notice a table with four cells on the first line. This is the Truth in Lending Statement. Once you are familiar with how to quickly interpret one, comparing different loans becomes much easier.

Boxes in the TIL Statement

Every TIL Statement has four boxes on first line. The first two have a thick outline to stand out. These are important and the requirement is for a thick border to make them easy to find.

TIL Statement Boxes 1 and 2

Box one is the Annual percentage Rate (APR) of the loan. This is a standardized rate that communicates to overall cost of the loan. You may notice most title loan are advertised using the monthly interest rate. For example, 8% per month or 12% per month. Even with a title loan, the TIL Statement requires the APR to be displayed in box one.

Box two is the Finance Charge. This is another standard box every type of loan including title loans. This is what the credit will cost you in dollars. Understanding how to quickly look at these two boxes on a TIL statement will make evaluating loans easy. We’ll look at a few examples below.

TIL Statement Boxes 3 and 4

The third Box is the Amount Financed. In the case of a Title Loan this is the amount you are borrowing plus any fees you are being charge for the loan. This is also standard for all loans and represents the amount you are borrowing from the lender. There should be no surprises here.

The fourth box is the Total of Payments. This is how much you will pay in total. This includes both the amount you borrowed plus all interest and fees. This is the total dollar amount you will have paid assuming you make every payment as scheduled. The nice thing about these statements is that every most lenders are required to provide you with one in the same or similar format; if they don’t, you are allowed to ask for one.

Monthly Rate versus APR for Title Loans

When looking at Title Loans, it is important to note the difference between APR and the Monthly Interest Rate. Most Title Lenders use monthly interest rates; however the APR will be listed on the Truth in Lending Statement. The APR is simply the Monthly Interest Rate times 12.

A Monthly Interest Rate of 15% would equate to an APR of 180% (12 times 15). An APR of 240% would equate to a monthly interest rate of 20% (240 divided by 12). For every 1% increase in the monthly interest rate, the APR increases by 12%, which can add up quickly.

Because the Truth in Lending Statement requires the APR to be listed, in an obvious display, your ability to compare lenders is made much easier. You do not need to understand any complex financial equations or terms.

TIL Statement Examples

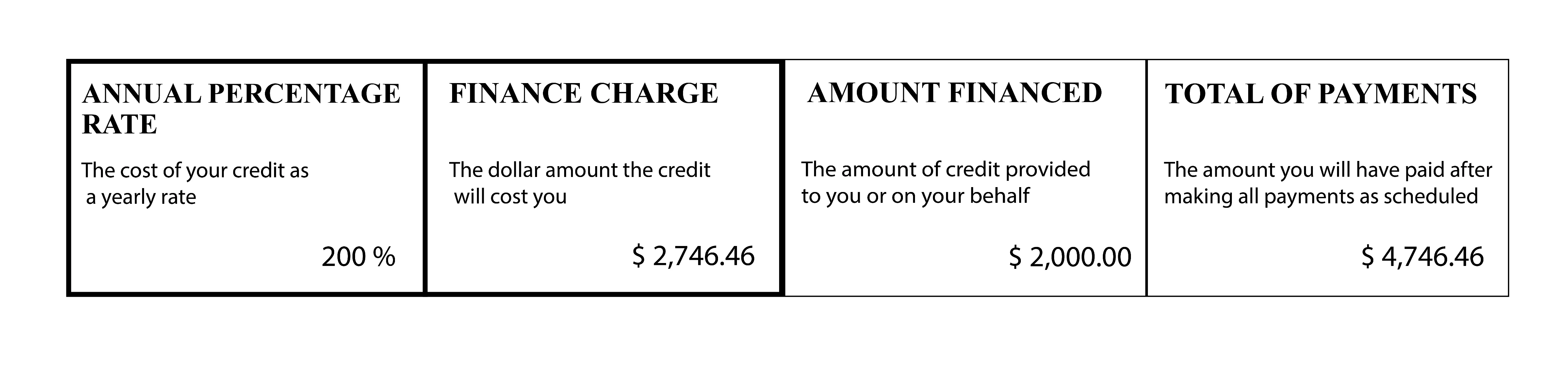

For example, let’s look at the four items from a Truth in Lending Statement for a $2000 loan with a 12 month term and an APR of 200%:

As you can see in this statement this loan would cost you $2,746.46 to borrow $2000. Your total payback amount is $4,746.46. In simple terms, this is a very expensive loan, you are paying back much more than you originally borrowed. Now lets look at the same information for the same loan with an APR of 96% (8% per month):

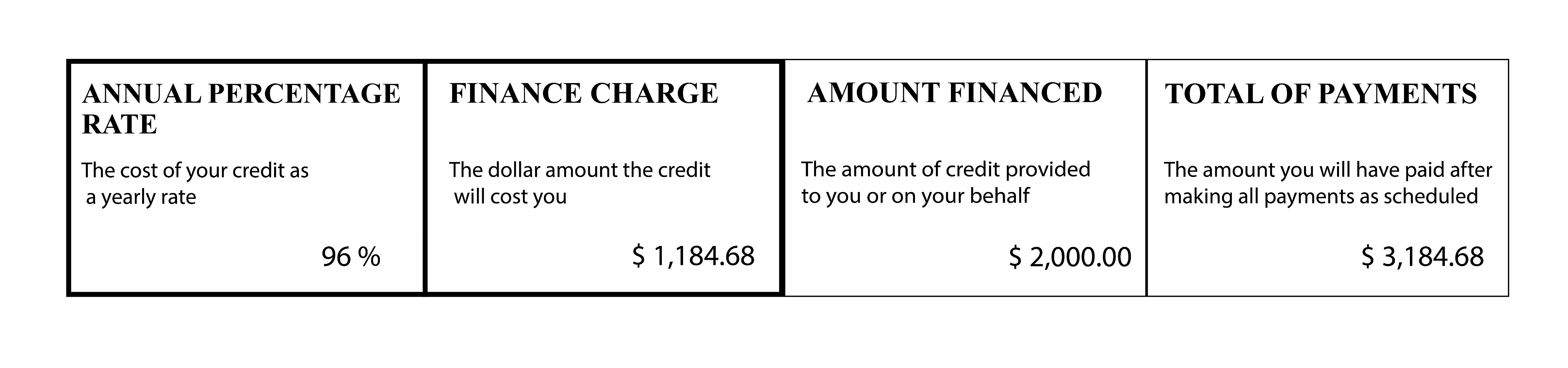

As you can see in this statement this loan would cost you $1,184.68 to borrow $2000. Your total payback amount is $3,184.68. Instead of paying $2,746.46 in finance charges you are only paying $1,184.68; a difference of $1,561.78 or over $130 a month. On a $2,000 loan this is a significant difference. The finance charges on the 8% per month loan are significantly less than half of the finance charges on the 16.67% loan.

Summary

Use the information provided to you by the Truth in Lending Statement to make sure you understand exactly what the lender is charging you for the loan. And, as always, if you are not comfortable with the terms, don’t be afraid to walk away from the loan.