Car title loans can be confusing. This is especially true if you have never had one before and don’t know how they work. When researching and reading about car title loans you may come across the term “roll over”.

So what exactly is a car title loan roll over and why are they not a good idea?

Car Title Loan Roll over Explained

A title loan roll over is an extension of the title loan for an additional term. The term is usually 30 days but can vary from state to state. The most common use of roll overs is on single term, single payment title loans.

As you may have found through reading about title loans, some states and online title lenders are now offering loans with monthly payments. Because this post is about roll overs, we’ll stick to discussing single payment loans.

Rolling over the loan consists of making the interest and fee payment at the due date, but “rolling over” the principal amount for another term. This is typically not a good idea, as explained by the FTC in a post about roll overs.

What is a Single Payment Title Loan?

A single payment title loan is fairly simple and only gets complicated if you “roll over” the loan. Basically, you borrow a fixed amount of money at a monthly interest rate.

You are required to repay the amount borrowed plus interest and fees by the due date. To make it easier, let’s look at an example:

Single Payment Title Loan Example:

Example: a $1,000 loan due in 30 days at a monthly rate of 25% and with a fee of $30.

In this example, we will owe the amount borrowed plus interest and fees 30 days from the date of the loan. In this case the amount borrowed is $1,000. The interest due is the amount borrowed times the monthly rate:

Interest due = $1,000 x 25% = $250. The fee is $30. So the total due is:

Total due = $1,000 + $250 + $30 = $1,280.

So a payment of $1,280 is due on the 30th day following the loan origination to close out the loan and get our title back. If we pay the $1,280 on the due date, we get our title back and move on with life. If this is the case it was a rather simple transaction and we still have our car and title.

What if we don’t have $1,280? After all, it has only been 30 days since we needed the loan. We may not have had time to save that much. This is where roll overs come in. We’ll see why they are not a good idea shortly.

Car Title Loan Roll Over 1:

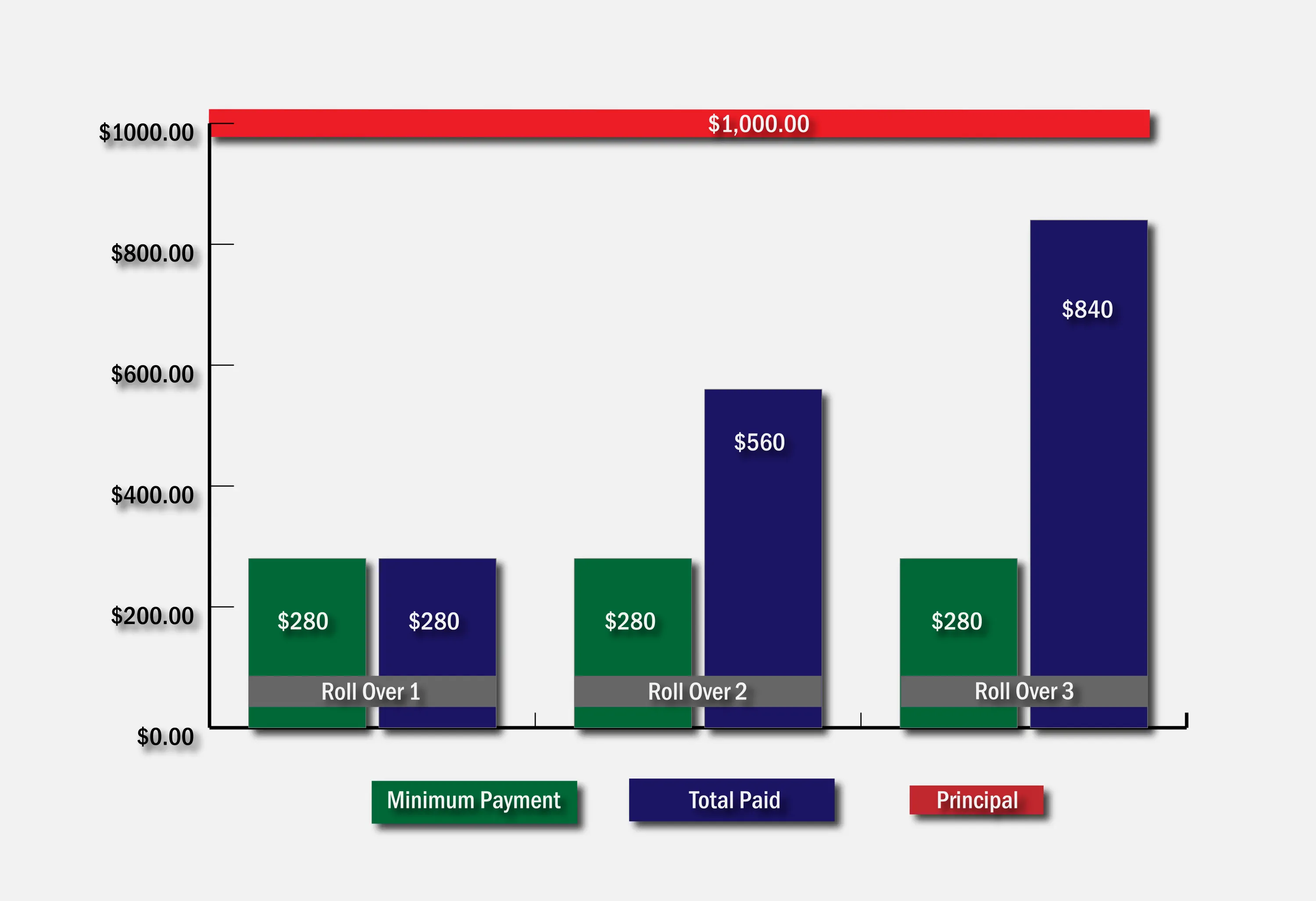

In many cases the title lender will allow you to roll over your title loan for another 30 day period if you pay the interest and fees due. In our example, the interest and fees due equal $280. This is certainly easier to repay the $1,280.

So, to avoid losing our vehicle, like many borrowers, we opt for this choice and roll over the loan. In our example we’ll pay the $280 and roll over the loan for another 30 days. Now, we’ll owe the same amount and we have another 30 days to come up with the money.

Car Title Loan Roll Over 2:

Now the payment is due for the first roll over. We want to close out our loan and get our title back. To do this we need to pay the amount borrowed plus interest and fees.

In our example this is $1,000 (the original amount borrowed) plus the $280 in interest and fees for a total of $1,280. You’ll notice it is the same amount as the previous month. This is how single payment title loans work.

We will need to come up with $1,280 to get our title back, and if we can’t the lender can repossess the car. Unfortunately it has only been 60 days since we needed the title loan. Last month we had to pay $280, so we still haven’t had enough time to save $1,280.

To avoid losing the vehicle, we decide to pay the $280 in interest and fees to roll over the loan for another month. Now we have paid $560 and at the end of a month will owe $1,280 to get the title back. The interest and fees are quickly adding up.

Even worse, the principal amount owed on the loan is still $1,000. So, none of the $560 we have paid has gone towards reducing the principal. This is the reason roll overs are strongly discouraged.

Car Title Loan Roll Over 3:

After the second roll over, by the due date, the same payment is due in full to close out the loan. We want to close out our loan and get our title back. To do this we still need to come up with $1,280 just like the previous month.

Again, because we spent $280 last month we still haven’t had enough time to save $1,280. Again, to avoid losing our vehicle, we decide to pay the $280 in interest and fees to roll over the loan for another month.

As shown in the chart above, now we have paid $840 and we still owe the original $1,000 we borrowed to open the loan. This is quickly getting costly and we are no closer to getting our title back. Let’s continue our example.

Additional Roll Overs:

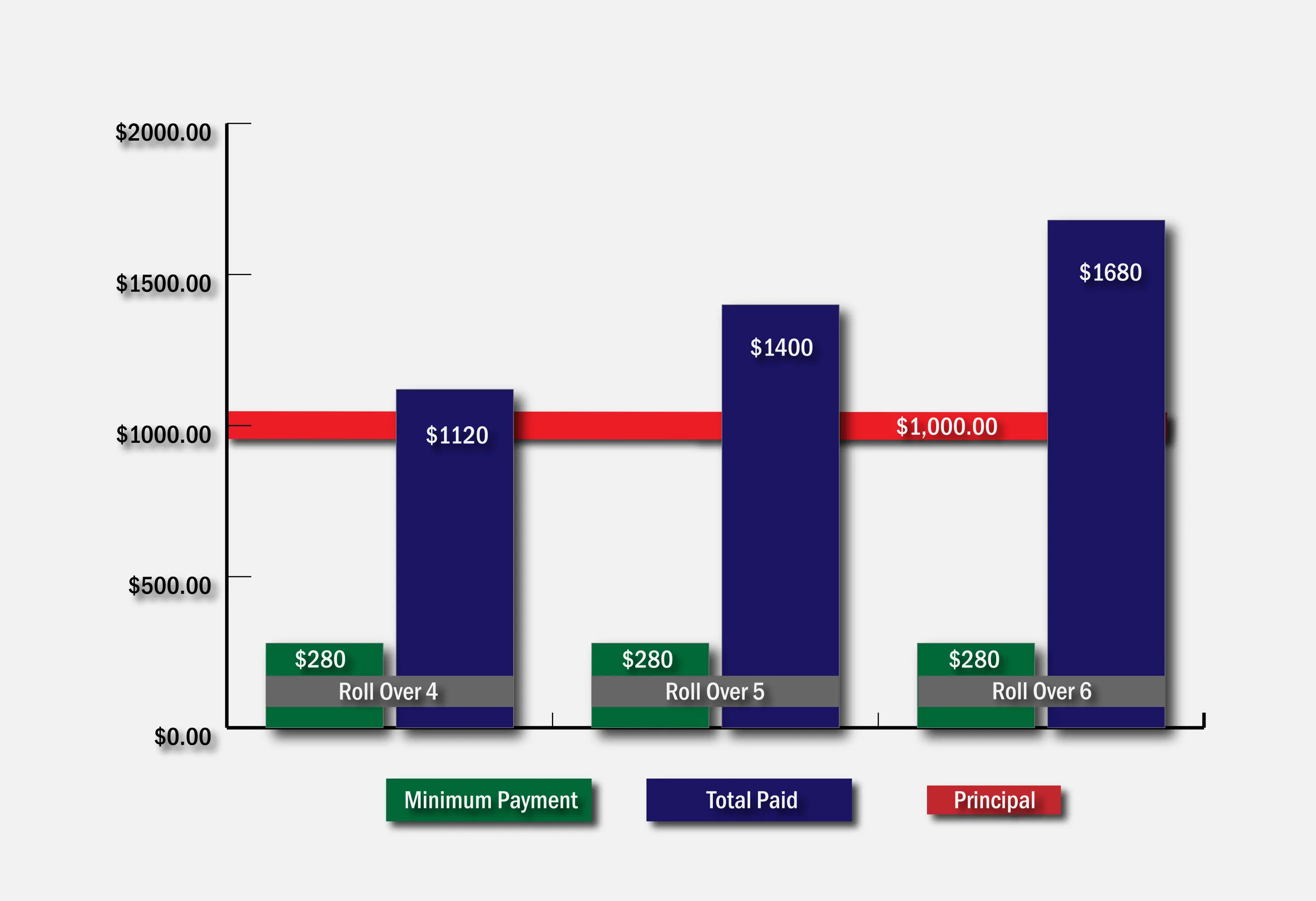

At the end of the third month, if we can’t repay the entire $1,280 then we may need to roll over the loan again by paying the $280 in interest and fees. If we continue to do this it can become an endless cycle. After six months, a chart of what we paid each month and in total is shown below:

As you can see, by the 6th month we have paid a total of $1,680 in interest and fees. And, what is worse is the fact that we still owe the original principal of $1,000 to get our title back. That makes a 6 month loan for $1,000 cost $2,680 to repay. Roll overs are not recommended for this reason.

It is important to note that not all states allow roll overs. Additionally, some states have limits on the number of roll overs. Make sure to find out the title loan laws in your state before signing any loan agreement.

How does the Roll Over Cycle End?

The roll over cycle has to end at some point. So, how does it end? There are two ways. The first is we come up with the total amount owed and get our title back.

This means we need to find the original $1,000 borrowed plus the $280 in interest in fees. In our example, this is after we have paid $1,680. This can be challenging so what happens if we can’t?

The second way roll overs end; we fail to come up with the total owed and lose our vehicle to the lender. Depending on the state, the lender may be required to pay us the surplus from selling the vehicle, or, in some states the lender keeps the surplus. This means we may have paid $1,680 and lost our vehicle.

Limiting the Cost of Title Loans

If you get a single payment title loan make sure you can repay the loan in full by the due date. If something happens and you absolutely have to roll over the loan pay as much as you can to reduce the interest charges.

For monthly term loans, make sure to understand how those costs are calculated. Our post on the true cost of title loans explains these costs.

Looking at our example again and pay an extra $300 the first and second month, the amount due at the end of the third month is roughly $411 instead of $1,280. Additionally, make early and extra payments as much as possible to limit the amount of interest accruing.

It is worth looking into other loans if you need a fast loan. A couple of other examples of fast loans are payday loans and cash advances. Always consider any alternatives prior to proceeding with a title loan.

Summary

Car title loan roll overs are not recommended for the reasons we have discussed. Some states have taken action and moved to monthly term loans where a portion of the payment is required to be applied to the principal of the loan. For many borrowers this is better than owing the entire principal every month.

Regardless, car title loans are generally high interest loans, even from discount title lenders. If you do need to get a title loan, find a lender with a reasonable interest rate and make sure you can afford to repay the loan according to the terms of the loan.

While it is not always available in every case, refinancing a title loan may be an option to lower payments if you are stuck in a high interest loan.