Car title loans can be a fast and easy source of funding when you need it most. If you are new to title loans you may not understand the intricacies involved with them, and, specifically, how to get a title loan.

Further, it is important to learn the differences between title loan companies and how to get a good deal on a title loan.

Options for Fast Cash

On the one hand, these loans can be a lifeline for many consumers without other credit options. They can provide a much needed bridge in cash flow for a short period during an emergency.

Need to be used Wisely

On the other hand, title loans can become the source of more financial problems if taken out for the wrong reasons or without understanding how they work. You’ll want to avoid these types of situations.

Doing so requires understanding when one makes sense and when it doesn’t. It is very important to point out that car title loans are short term solutions and should not be used to try to solve long term financial problems.

Car Title Loan Information

The very first part of getting a title loan involves finding useful up to date information. Today, much of the information published online related to title loans is either incomplete, inaccurate, biased, or outdated.

If you read anything published by most title lenders, they make it sound like a title loan is a great choice for everyone.

If you read something published by competitors to title lenders; they make it sound like title loans should be avoided at all costs.

As with most things in life the truth is somewhere in the middle. Fast Title Lenders tries to make a point of providing facts to customers. This is so they can make the best decision to improve their situation, even when this is not a title loan.

This means telling some people a title loan is not the best option. To help educate and inform those seeking a title loan, we published this Complete Guide on How to Get a Title Loan.

Shopping for a title loan can be and often is confusing, especially given the number of lenders and financial writers publishing conflicting and incomplete information.

Shopping for and learning how to get a title loan can be a daunting task; even more so if you are new to title loans. This complete guide to how to get a title loan is designed to provide useful information to quickly learn how to go about finding the best title loan and initiating the process.

Complete Guide on How to Get a Title Loan

In this complete guide detailing How to Get a Title Loan we will cover the entire title loan process. This includes everything; not just the part that involves the lender.

The full process of getting a title loan should begin well before finding a lender. Our guide begins with how to determine if a title loan is right for you (it is not always the best choice); and ends with how to save on your title loan during the repayment period should you choose one.

Title Loans have a wide range of interest rates and fees. Making sure you understand the costs associated with the loan, and how interest works, is critical to being sure of your ability to repay the loan on time.

Fast Title Lenders was founded on the principles of transparency and honesty and has made it a goal to inform title loan customers with accurate information related to car title loans.

Sometimes this results in customers finding an alternative to a title loan that better suits their needs. This is far better than getting stuck in a loan that is not right for their situation.

Regardless, it is our belief that an informed customer makes the best customer. We also include getting your title back and also title lender tactics to be aware of.

We go over how to get the best deal on a title loan, so you can avoid overpaying. Title loans are very different from Payday loans and other car loans.

It is important to fully understand how title loans work, and what they cost, before entering into one. Before we discuss how to get a title loan, first we need to understand what a title loan is.

What is a Title Loan?

First, what is a title loan, and why would anyone need one? The simple answer is a Car Title Loan is a way to borrow money using your vehicle as collateral. You pledge your vehicle as collateral for the loan.

Sometimes they are called Title Pawns, Pink Slip Loans, Registration Loans, and Auto Title Loans. They are all very similar loans secured by your vehicle. This makes them secured loans. So, what is a secured loan?

What is a Secured Loan?

As mentioned title loans are secured loans. A secured loan is a loan that is backed by collateral. To receive the loan, you pledge property, in this case your vehicle, as collateral for the loan.

If you default on the loan the lender has a claim on the collateral. In the case of a car title loan this may lead to repossession.

The fact that the loan is secured by collateral (the vehicle) is what makes car title loans easy to qualify for. This is also the reason why your credit score is not an issue with most lenders.

What is an Unsecured Loan?

An unsecured loan is a loan with no collateral. It is based on your credit scored. Common unsecured loans include credit card accounts and lines of credit.

If you default on the loan, the lender has to try to collect. This is often in the form of a civil judgement. An example of unsecured loans includes Payday loans and credit card cash advances.

Borrowing Money using your Car

Car title loans allow you to borrow money using your vehicle as collateral for the loan. Keep in mind, however, that this means if you default, the lender can repossess and sell your vehicle to recover the cost of the loan.

This means it is very important to make sure your income can support the payments for the loan. We’ll cover this in more detail later.

Additionally, some lenders tend to complicate the loan agreements with terms and conditions that can end up costing a significant amount of money. It is important to understand these terms; a topic we’ll also cover.

Complete Guide on How to get a Title Loan – Key Topics:

In this complete guide on how to get a title loan we will cover the key topics detailing how to get a title loan, starting at the beginning of the process and continuing all the way through getting your title back.

These key topics related to how to get a title loan include:

- What makes a good title loan candidate – Before applying for a title loan you need to make sure you make a good candidate. Not everyone does, and we prefer to let our customers know if they do not make good candidates. Factors we’ll discuss include:

- Immediate Financial need

- Length of financial solution

- Vehicle specifics

- Types of income

- Title Loan Requirements – To qualify for, apply for, and receive a title loan you will need to meet the title loan requirements. While certain requirements may vary depending on the lender, the following are usually consistent:

- Lien free Title

- Drivers License

- Proof of Insurance

- Other, lender specific

- Steps -How to get a Title Loan. In this section we go over each of the steps required to get a title loan in detail. We also cover one very important step most other lenders leave out; choosing your lender. This step will have the biggest impact on your title loan cost and experience.

- Finding a lender

- Applying for a title loan

- Determining the loan amount

- Getting your funds

- Making payments

- Getting your Title back

- Ways to save on Title Loans – Similar to choosing your lender, ways to save when learning how to get a title loan is something other lenders do not talk about. We think it is important to keep your loan costs at a minimum. A title loan is already costly enough, use these recommendations to keep your title loan as cheap as possible. Cost related topics we cover include:

- Interest Rates

- Payments

- Title Loan fees

- Common Mistakes to avoid – Learning how to get a title loan can be confusing. We cover common mistakes many borrowers make so you can avoid them.

- Title Loan mistakes

- Online Title Loan Options – there are now ways to get a title loan completely online with no store visit. There are pros and cons to this, so make sure you understand how online title loans work versus in-person loans.

Preparation Steps for How to get a Title Loan:

The first part of getting a title loan is preparation. This is a very important part of how to get a title loan that is often overlooked.

When this is overlooked, borrowers tend to quickly search for “title loan places near me” and rush in to a title loan without any preparation or research.

This can lead to overpaying for a title loan or agreeing to a loan with terms that are difficult to repay. These agreements may also have prepayment penalties, excessive fees, and other terms and conditions that do not favor the borrower. Preparation for a title loan can be broken into simple Steps:

Preparation First Step – Is a Title Loan right for me?

The first step during title loan preparation is determining whether or not a Title loan is right for you. For some, Title Loans are an excellent source of short term funding that can solve difficult financial problems.

For others, they are the start of longer term financial problems and can lead to repossession. Before applying for a title loan, you will want to make sure it will improve your situation by solving a problem.

Title Loans are unique when compared to other forms of credit and are not the best choice for everyone. This means not everyone is a good candidate for a title loan.

At Fast Title Lenders, if you are not a good candidate for a title loan, we tell you. Unlike other lenders that will lend to anyone, we prefer to make sure the loan is in the best interest of the borrower.

Before applying for a title loan, you will want to make sure getting the loan will improve your situation and not make it worse.

There are several factors involved in determining whether or not you are a good candidate for a title loan. Before we discuss the process for getting a title loan, let’s make sure you are a good candidate first.

What makes a good Title Loan Candidate?

Generally, to be a good candidate for a car title loan you will need to:

- Own your vehicle, free and clear

- Have an immediate or urgent financial need

- Have a means of repaying the loan

- Live in a State that allows Title loans

- Have a short term financial problem

- A vehicle that supports the loan value

If you are reading this, you probably have an immediate financial need and a vehicle. You must also make sure you have a means of repaying the loan.

This is usually using income from a job; but it can be any source of income as long as it is reliable. Remember, a title loan uses your vehicle as collateral, so if you default you can lose your car. If you can’t repay the loan, it does not make sense to apply for one.

Additionally, if you still have an existing loan on your vehicle, you will not be able to get a title loan and should seek a title loan alternative. If you own your vehicle and have a means of repaying the loan, you may be a good title loan candidate and can continue learning how to get a title loan.

Title Loan Candidate Factor – Location

Car Title loans are regulated at the state level and are not readily available in all states. To be a good candidate you will need to live in a state that allows title loans. To find out whether they allow title loans where you live, check the laws in your state here. The link will open a map and chart.

Check the laws for the state you live in. While you are doing that, write down the amount in the Max Loan column and the percentage in the Cost Limits column for use later (we’ll go over why shortly).

If you live in a state that allows title loans, you may be a candidate and we can move on to the financial portion of the article. If you live in a state without title loans, you may still be able to get an online title loan.

Title Loan Candidate Factor – Immediate Financial Need

Title Loan candidates usually have an immediate, or imminent, financial need that can not be met through any other means. Other means could include savings, home equity, or existing credit cards.

If you have access to these types of funds, you will want to explore those first. The interest rate will likely be lower than the rate with a Title Loan.

If you choose a lender quickly the interest rate may be very high (usually the maximum allowable rate); so explore all other options first. Even with a low rate title loan at 8% per month is 96% APR.

This is a fraction of what many lenders charge, but still higher than other forms of credit.

You should explore all available options before choosing a title loan. Assuming these other means are not options, a title loan may be a viable option so we’ll move on to the next criteria; the loan term.

Loan Term – Title Loans are not long term solutions

Title Loans are designed to meet short term financial needs and are not long term financial solutions. With that in mind, there are many states now offering monthly term loans that can range from a few months to a couple of years.

This is contrary to most of the articles stating that title loans must be repaid in full within 15-30 days. There are still states with 30 day loans, so you will need to check your state laws to see what is available where you live.

If you need a loan with a repayment term of between 30 days to 24 months, you may be a good candidate for a title loan.

Regardless, no title loan is meant to be a long term solution, if you need a long term solution you are not a good candidate for a title loan and should seek an alternative.

When you try to extend a title loan beyond 24 months it has little impact on lowering the monthly payment and a huge impact on the total costs.

Vehicle for the Title Loan

You will need to make sure you have a vehicle that can be used to secure the loan and that the vehicle is sufficient for your specific loan requirement.

Obviously, you will need to own the vehicle with no liens. Many lenders have year and mileage restrictions with regards to the vehicles they can lend on.

Some do not, these tend to have the highest interest rates. While we do not have any age or mileage restrictions, we do require vehicles to have a fair market value of $5,000.00.

Many older (classic) cars are worth more than $5,000.00 but are older than 15-20 years, so a year cutoff does not make sense in our opinion. Classic car title loans are one of our specialties.

To determine how much you can borrow, take the percentage form the previous exercise (from the Max Loan column, if there is no percentage use 50%) and multiply by your vehicle’s value.

For example, if your vehicle is worth $6,000.00 and you live in Illinois, the maximum loan amount is $3,000.00. To figure out what your vehicle is worth, perform an honest assessment of the condition.

This includes the interior, exterior, and mechanical condition. Also consider whether the vehicle has been in an accident. Use an online vehicle valuation tool like the one available at Kelley Blue Book.

Does the Vehicle Value support the car Title Loan Amount?

Now that you know what the maximum loan amount your vehicle can support, is that amount enough to meet your immediate financial need?

If yes, you may be a good candidate. If no, a title loan may not be the answer for you. Assuming the vehicle meets the need, the next step is the income type.

Income Types – What income do I need for a Title Loan?

Different people have different forms of income, not all make good candidates for title loans. For a monthly term loan, you will want to make sure you have steady income to support the monthly payment.

Remember, you can lose your vehicle so it is important to make sure you can make at least the minimum payment every month.

If you are paid on commission, and your income fluctuates significantly from month to month, you need to take this into consideration.

One of the biggest mistakes borrowers can make when getting a title loan is not making sure they can easily afford at least the minimum monthly payment every month.

This can lead to late payments, late fees, missed payments, and in the worse case repossession.

Some forms of payment that make good candidates for title loans include:

- Salaried pay that is the same every month

- 1099 Employees with outstanding invoices (hours already work but not paid)

- Sales/commissions already made but not paid

- Annuity payments and other guaranteed sources of income

- Tax returns

Now that you have gone through and met the criteria for being a good candidate for a title loan, we can continue with how to get a title loan and go over the specific steps you will need to take to get one and have it funded quickly. This will include how to find the best lender and not overpay for the loan.

Preparation Step 2: Determine How much you need to Borrow

Next, you will need to decide on the right title loan amount. The Title Loan amount should cover your immediate expenses AND result in a payment you can afford each month.

As stated, you should be certain you can afford at least the minimum monthly payment before proceeding with a title loan. If the amount doesn’t meet your needs, or the payment is more than you can afford, a title loan is probably not right for you.

Determine the amount you need to borrow to cover your immediate expense; and the amount you can afford to repay each month. Use or Title Loan Calculator and adjust the loan term (months) until you find a payment that meets your needs.

If you can find a loan amount that meets your needs and a term that results in a monthly payment you can afford, you may be a good candidate for a title loan.

Title Lenders’ Rates

My lender won’t tell me how much they charge, how do I figure out what my payment will be? This question is asked often, unfortunately most title lenders prefer to keep there actual costs very difficult to figure out.

Our suggestion: Take the rate from the previous exercise (the percentage from the Cost Limits column) and use our Title Loan Cost Comparison Calculator. Fast Title Lenders supports the principles of honesty and transparency.

As such, we developed a tool that allows you to calculate a full payment schedule. It includes interest summaries, for any loan from any lender. Plug in your loan amount, the lender’s rate or state maximum, and you’re able to view the payment details. Once you have the monthly payment you can afford, for a loan amount that meets your needs, we can move on to the next criteria: the vehicle.

A key point to remember is that just because you qualify for a certain amount does not meant that is the amount you should borrow. Most title lenders try to convince you to borrow the maximum amount you qualify for. The reason is simple. The more you borrow the more interest you pay and therefor the more money the lender makes.

This is why going through the previous exercise determining how much you need to borrow is essential. With a title loan, it is always best to borrow the least amount necessary.

Title Loan Cost versus Benefit

Now that you know how much you need to borrow to cover your expense, and have determined the optimal loan term in months, you have an idea of the total cost of the loan.

To make a title loan worth the expense, the benefit you receive from the loan needs to outweigh the cost.

This is not always easy to determine as not all benefits have a dollar value assigned to them. The three examples we used in our post ‘Are Title Loans worth it?’ were covering an emergency expense, paying for a car repair, and reducing outstanding credit card debt to make a large purchase.

Essentially, you want to try to quantify the benefit you receive from the title loan to make sure it is worth it.

Title Loan Cost/Benefit Example

As an example, let’s look at a car repair costing $1,000.00. Let’s say it would take 3 weeks to save the money to pay for the repair. During those three weeks, you would need to find alternate transportation to work. How much would that cost?

Obviously, it varies depending on where you live and where you work. If you can find an affordable alternative for getting to work during those three weeks, such as a carpool or borrowing a car; then a title loan is probably not worth it.

If you have to rent a car, then a title loan might worth it. This is the type of analysis you should perform before getting a title loan. See our page for more information on how to perform a cost benefit analysis.

Preparation Step 3: Find The Best Title Loan Company

The next step when preparing for a title loan is one of the most important steps. If you decide to skip all others make sure to at least perform this step.

When finding out how to get a title loan finding a good lender can make the difference between a great experience and a horrible one. Title loans have a negative stigma for a reason.

Many title loan companies charge very high rates and have been known to treat their customers poorly. These are the companies you should avoid. Sometimes you can tell just by visiting their website.

Title Lender Reputation:

When choosing your lender you will want find find a title loan company that treats their customers fairly and has a good reputation. Reading customer reviews used to be an easy way of doing do.

Unfortunately, it is not quite as easy to find accurate reviews for title loan companies anymore. Many of their customers started leaving poor reviews, and they took notice.

Now, it is common practice for some lenders to ask the customer to fill out a 5 star review right before they give them the check for their loan.

The borrower is ready to leave and doesn’t want to jeopardize getting their check, so they leave the review. The sad part is this review does not represent their full experience with the lender and by the time they have made a few payments it is too late to go back and change the review.

The good news is there are still a few sources where customers can leave comprehensive reviews describing their experience with the lender. These include Ripoff Report and Better Business Bureau. Visit both of these sites, read other experiences, and learn from them.

Title Lender Costs:

The costs of a title loan are a major consideration when choosing your lender. It is not uncommon to see the lender’s costs directly related to their reputation.

Interest rates vary significantly and many lenders charge very high rates. Visit the lender’s site and try to find their advertised rate.

Many of the lenders that charge very high rates do not advertise their rates. If you can’t find their rate, give them a call and ask for a quote.

If they will not give you one, ask for their highest rate and use that for your comparison. We’ll discuss how to find the best lender shortly, for now just be aware of how to find accurate research.

Minimum Loan Amounts and Terms

Car title loans are short term solutions to financial problems. Even the best online title loans can be expensive. It is best to borrow only what you need for the shortest term possible.

Some lenders have high ($2,500+) minimum loan amounts and long loan terms. Title loans are not meant to be long term loans.

When you take a high interest loan and extend the loan term past a year the costs become excessive. These charts show the cost of these title loans.

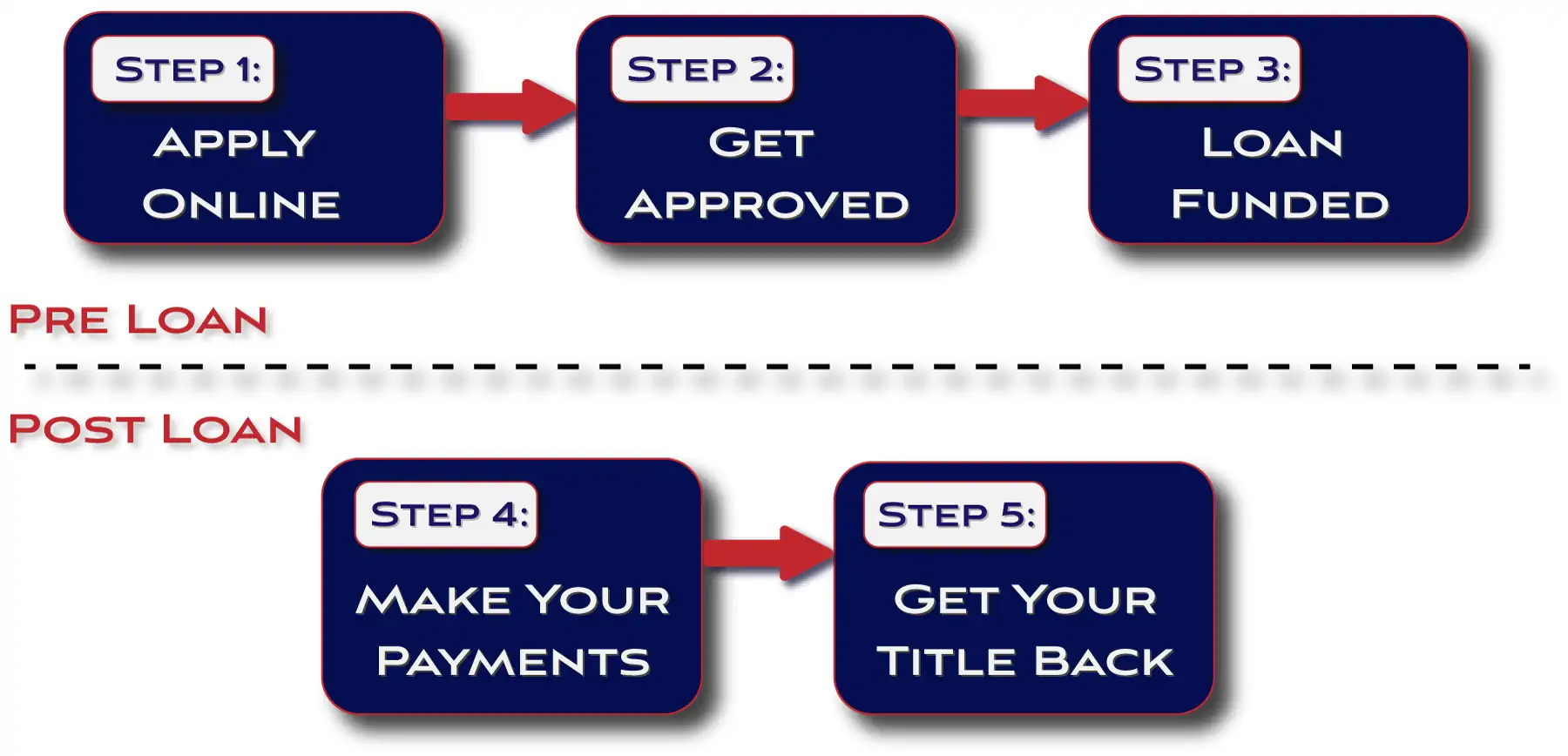

How to get a Title Loan – Full Title Loan Process:

Now that preparation is complete, we have determined you meet all the requirements, and you are a good candidate for a title loan, we can discuss the title loan process.

The process varies slightly depending on the lender, but generally includes the steps detailed below.

Title loans are one of the fastest and easiest loans to get, without the lengthy underwriting process associated with most other loans. The paperwork required to get a car title loan is fairly simple and straightforward. You can even complete some, or all, of the process online with most lenders.

There are also a few lenders offering “online only” title loans; although there are some risks associated with a completely online title loan.

Unfortunately, there is no such this as an “Instant Online Title Loan”. When considering a title loan, however, you need to be careful. We recommend choosing your lender wisely. We go over how to get a title loan following these easy steps:

- Meet the Title Loan Requirements

- Find a reputable Lender

- Apply for the Title Loan

- Get Approved

- Determine how much you want to borrow

- Complete the Loan Agreement and Receive your Funds

- Make your Payments

- Get your Title back

1. Meet The Title Loan Requirements

For the first step in the title loan process is to make sure you meet the title loan requirements. There is no point in spending time applying for a title loan if you can’t meet the requirements.

It often makes the process go smoother when you meet the requirements before applying and have all of your information in one place.

As you gather the documents related to each requirement, put them into a single folder or file. Then, when you are ready to apply, you can do so quickly.

What are the Title Loan Requirements?

Title loan requirements include information related to the borrower (ID, proof of income) and information related to the vehicle (vehicle title, proof of insurance).

Generally, you will need to meet the following requirements to get a Title loan:

- Vehicle – obviously you need to own a vehicle

- Lien free title – You will need a free and clear title

- Drivers License – a valid government issued photo ID

- Proof of Insurance – the vehicle will need to be insured

- Proof of Income – usually the two most recent pay statements or equivalent

These requirements are usually enough to get a title loan with most lenders, including us, although some lenders do have additional requirements.

These can include a spare key to the vehicle, vehicle pictures, a list of personal references, and, in some cases, adding a GPS device to your vehicle.

For title loans online, you will need to provide detailed pictures of the vehicle. Some online lenders also required you to have the vehicle inspected by a third party. These are specific to online only title loans, so we won’t go into detail here since our focus is simply on how to get a title loan.

Once you meet the requirements, and have collected your information and have it in a single place we can move on to the next step; find a lender. This step is critical to getting the best deal on your loan.

2. Choose your Title Lender:

When going through the process of how to get a title loan, one of the most important parts of the process is choosing you lender. Ironically, it is also a step that is overlooked and rarely talked about by lenders.

There is a simple reason for this, they do not want you to know there is a difference, sometimes a big difference, between lenders.

Finding a lender that charges a reasonable rate, versus the typical lender that charges the state maximum, can save you thousands on your loan.

We recently published a title loan costs article detailing the costs that make up title loans and provide several sample loan amounts and terms. It is worth reading if you do not understand how title loan interest works.

How do I find the best Title Loan Company?

We suggest taking a cautious approach to choosing your lender, it may save you a lot of money and hassle. We talked about going over how to get the best deal on a title loan, and choosing the lender is by far the most important part of getting the best deal.

This is a step that is often rushed or overlooked and may result in a very expensive title loan with terms and conditions that do not favor you as the borrower.

Many lenders, including the largest and most well known, charge very high rates. In addition, they are not well known for customer service and can leave borrowers unhappy with nowhere to go when they have problems. Spending a little time on this step will have the biggest effect on your loan outcome.

Research your Lender’s Reputation

We also recommend taking at least a few minutes to read about the lender you are about to visit. Make sure the read reviews from the Better Business Bureau and Ripoff Report, as these are reviews from borrowers after they have had the loan for some time.

Make a list of lenders you want to avoid. Then, do a search, and find lenders that you may want to work with.

FTL Tip: There is a tactic now where lenders ask customers to leave a review as soon as the loan is funded; these are not exactly accurate representations of their experience and most cannot be updated after the review is left.

Once you find a lender that you feel comfortable doing business with, Find out their rates, fees, and terms. Call them and ask them about their costs, ask for an estimate, and make sure it works with your budget.

Feel free to use our title loan calculator to calculate your costs. Once you’ve found a lender, move on to the next step, apply.

3. Apply for the Title Loan

The next step in the process is to apply for the title loan. Depending on the lender this can be as simple as filling out an online application.

For some lenders, you may need to complete the application in person. To make sure the process goes smooth, use the information and documents you gathered when preparing for the loan.

Have them ready and in one place when you apply. This will help ensure the application process is done right the first time with no delays. Some online lenders may ask for a significant amount of personal information including references.

FTL Tip: When asked to provide employer and other reference contact information, ask when and under what circumstance the lender would contact them. It is important to know beforehand if the lender is going to call your employer and for what reason.

4. Get Approved for your Title Loan

Approval is also easy since Title loans do not require a credit check, your vehicle is your credit. Another advantage of a no credit check loan is no hard inquiry on your credit report, so applying will not affect you credit score. Getting approved for your loan is simple after you apply.

The lender will let you know, usually quickly, whether or not your loan is approved. If the loan is not approved, you should be provided with a reason. Perhaps you did not meet a requirement, requested an amount not supported by the vehicle value, or do not have the income to support the payments.

It is possible the lender may adjust the approval amount based on the vehicle appraisal. In most states you can borrow up to 50% of the vehicle’s value. This doesn’t always mean you should, however.

Which brings us the the next step, determining how much you should borrow.

5. Determine how much to Borrow

This is another important step when learning how to get a title loan. It is also one that is often overlooked and skipped over by the lender. Some lenders will try to guide you toward borrowing the maximum allowable amount.

Avoid Borrowing the “Max”

All you have to do is visit lenders’ sites and you will find plenty of “How much cash can I get?” forms to submit, with no “How much will this Cost?” forms.

This is for a reason, many lenders want you to borrow the maximum without thinking about how much it will cost to repay. They are counting on you needing money quickly with few other options.

From the preparation, you should already have an amount that will meet your needs and result in a payment you can afford. Now that the lender has provided the maximum amount you can borrow, compare that with the amount you need to cover your expense. Adjust this as needed based on your lender’s costs.

FTL Tip: Don’t let the lender to persuade you to borrow the maximum loan amount just because you qualify. Learning how to get a title loan includes sticking to the amount that best meets your needs.

Borrow only what you Need

Make sure to borrow only what you need, and only what you can afford to repay. If you default on the loan, you may lose your vehicle.

You know how much you need for your immediate expense, and how much you can afford to repay each month. The only adjustment you should make is a small cushion for the unexpected.

As most lenders will not provide you with a detailed breakout of their costs, use our car title loan calculator. It will let you enter a loan amount and term in months, and calculate your monthly payments with both principal and interest. Adjust the numbers as many times as needed until you have a loan amount and payment that meets your needs.

6. Complete the Loan Agreement and Receive your Funds:

Now that you have met the requirements, found a reputable lender, applied and got approved, and determined your optimal loan amount, you are ready to complete the loan agreement and receive your funds. Success.

At this point, make sure to read the loan agreement in full and ask questions if you do not understand something. It is much better to clear up any misunderstanding before you sign the agreement.

Make sure to find out what happens if you make a late payment and who to contact if you have any questions or problems.

FTL Tip: Read the loan agreement in full before signing. Ask questions about anything you don’t understand. Make sure there are no extra fees or charges that you are not aware of.

7. Finally, Make your Title Loan Payments

After you complete the agreement and receive your funds the next step will be making your payments. Hopefully you found a lender that accepts multiple forms of payments, including debit cards online and over the phone.

This will make it easier to make your payments on time and allow you to make them from anywhere. Typical payment methods include cash, check, and debit card.

Some lenders also accept Western Union; although the fees for the borrower can be high. Try to pay with check or debit card to avoid unnecessary fees.

FTL Tip: Consider setting up an automatic Bill Pay payment each month through your checking account if this is an option. This way, you will not accidentally miss a payment.

8. Get your Title back

After your final payment, you get your title back. If you chose a decent lender this usually happens quickly. When you are completing your loan agreement ask the lender how long it takes to get your title back after the final payment.

Additionally, you will want to confirm that any lien recorded on the title has been released. Depending on the state, liens can be electronic. It is always a good idea to ask for a lien release letter with your final payment in case there is ever any question about whether you satisfied the lien.

How to get a Title Loan and Save Money

Once you get a Title Loan and start making payments; it is not too late to save money on your loan. A few ways to save include:

- Making early payments – payments credited to your account early will reduce the amount of interest you are charged.

- Make more than the minimum payment – every dollar over the minimum payment is applied to your outstanding principal balance. This will not only reduce the amount you owe, but also the interest that accrues.

- Add an extra payment between scheduled payments – adding a payment is an easy way to reduce the amount of interest you are charged and save on your title loan. The extra payment can be any amount. Every dollar applied to the principal will reduce your total interest charges.

How to get a Title Loan – Common Mistakes to Avoid:

Learning how to get a title loan includes learning the most common title loan mistakes to avoid. The single biggest mistake most borrowers make when figuring out how to get a title loan is rushing to the nearest lender assuming they are all the same. Then they sign the loan agreement without reading it in full.

Most people get car title loans as a last resort, and often for an emergency or urgent need. Needing to move quickly is understandable, but doesn’t mean you should rush.

Additionally, financial stress and other factors can contribute to not thinking clearly. The lenders that charge very high rates are counting on this. They prefer you don’t ask questions about the rate or fees.

Making this mistake can cost you a significant amount of money. Some $2,000.00 title loans can cost $6,000.00 to repay.

Do yourself a favor and avoid these mistakes. Do not enter into a title loan agreement until you know exactly what the costs are, and make sure they are reasonable. Our car title loans are much less than the competition.

Conclusion:

Figuring out how to get a title loan is not complicated once you understand how title loans work. First, make sure you make a good title loan candidate.

This includes making sure your vehicle supports the loan value and you have the ability to repay the loan. Then, find the best title loan company. Apply online and get the process started.

Remember to use our Title Loan Calculator to compare costs and make sure you are getting the best deal on a title loan.

One of the biggest mistakes people make when executing how to get a title loan is rushing through the process assuming all lenders are equal. This can lead to overpaying for the loan.

Finally, and very important, read the loan agreement in full. Once you’re done, read it again. Make sure you understand all terms and conditions and agree with everything prior to signing.