Car title loans are a fast and easy way to borrow money using the equity in your vehicle. Essentially you use the equity in your vehicle as collateral for the loan to get cash fast for any urgent expense.

We have written about why title loans can be confusing. In addition, both finding and understanding title loan interest rates can also be a challenge. The reality is most car title loan interest rates are fairly high and some can be very high.

The Monthly Interest Rate

Title loan interest rates are usually communicated as a monthly rate. This is instead of the more common Annual Percentage Rate (APR). This can make it confusing to find out what the title loan actually costs.

One way to make things easier is to convert the monthly rate to APR. Then you can compare loans to each other in the same terms. Converting the monthly rate to an APR estimate is easy, just multiply by 12.

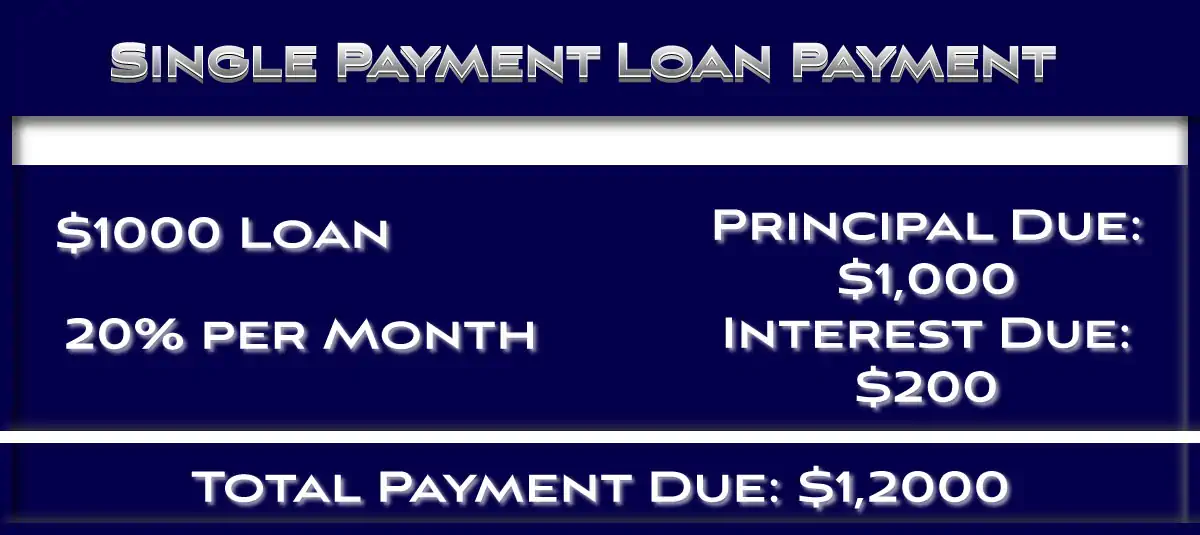

Figuring out or estimating the cost of a 30 day title loan is fairly easy. To get the total interest just multiple the amount borrowed by the monthly rate (an example is provided below).

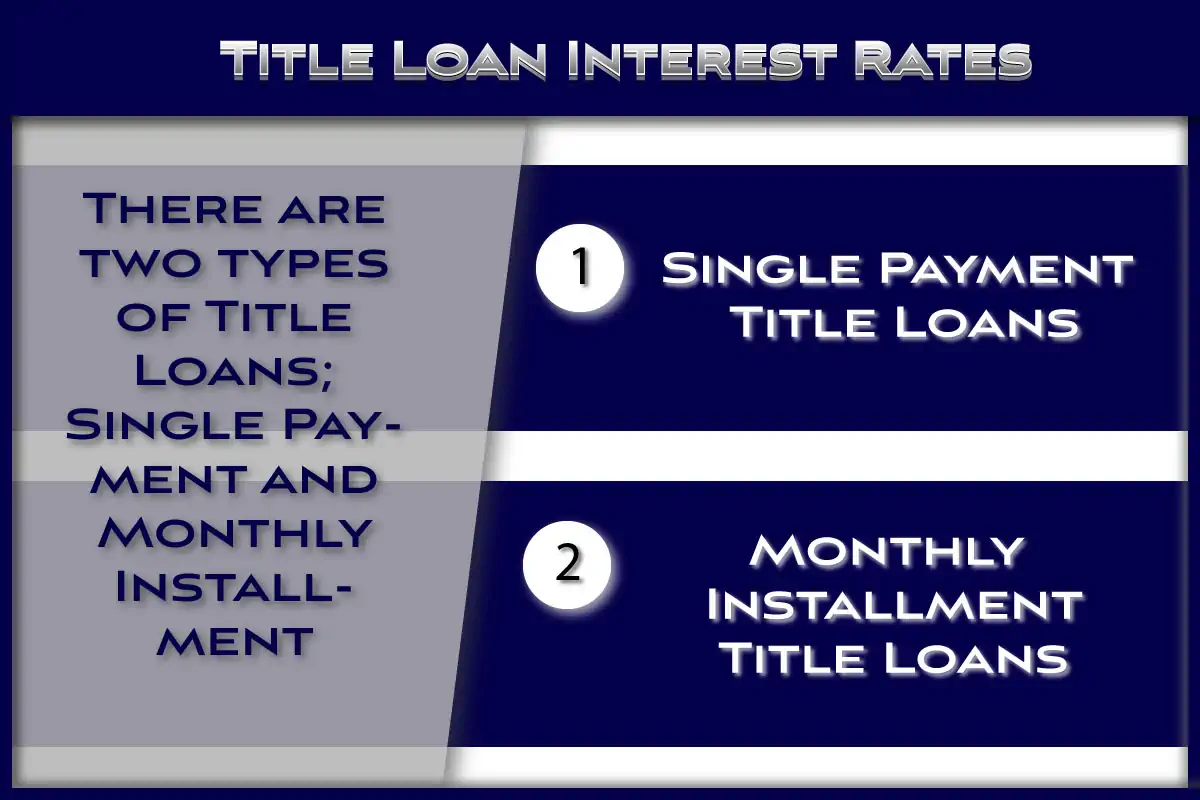

Two Main Title Loan Types

There are two main title loan types which can affect the interest rates for the loan. These include single payment title loans and monthly installment title loans.

Single Payment Title Loans

Single payment title loans are very short term loans with one payment due at the end of the loan term. These are sometimes called title pawns. The typical loan term for these types of loans is 30 days.

Interest Rates for Single Payment Title Loans

The reality is the interest rates for single payment title loans are generally high when expressed as APR. Most online title loan articles use these types of interest rates to categorize all title loans which is not always accurate.

The fact is interest rates for these loans can and do vary widely. They can range from under 36% APR to over 300% APR. In monthly terms this is 3% per month to 25% per month.

Single Payment Example

An example of a $1,000 title loan is shown below.

Monthly Installment Title Loan Interest Rates

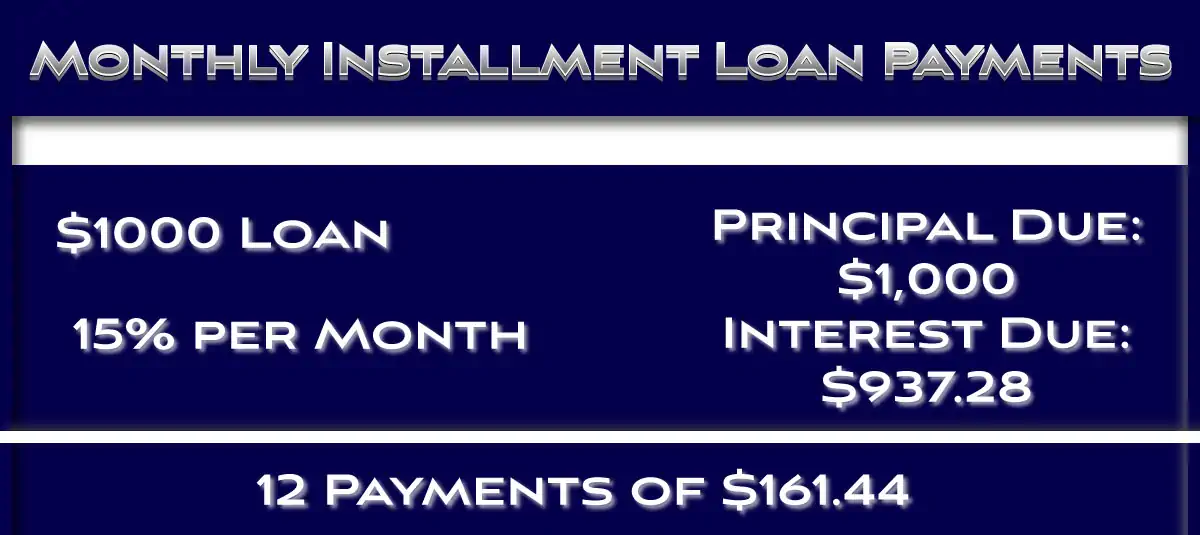

Monthly installment loans are usually amortized over the loan term. This means that you make equal payments each month until the loan is paid off. The lender applies a portion of the monthly payment to interest and the remainder to principal.

This means that the principal balance decreases each month. It also means that the longer the loan term the greater the total interest charges for the loan. This increases as the interest rates increases.

This can have a significant effect on a loan that is amortized for more than 12-24 months. The costs can get quite excessive. This is why title loans are short term solutions.

Monthly Installment Loan Example

Below is an example of a monthly installment loan. Some states have loans with monthly installments that can range anywhere from a couple of months to more than a year. Rapid online title loans often have monthly installments.

Title Loan Refinance

If you end up in a very high interest monthly installment title loan it is worth considering a title loan refinance. While refinancing title loans is not permitted in every state, if it is in your location you could save a significant amount of money by reducing the interest rate.

How to Find Title Loan Interest Rates

Given the wide variation in potential online title loan interest rates it is imperative to find out what the interest rate is before applying with a certain lender. This can be easier said than done.

Not all lender publish their rates and those that do often have multiple rates (or a range). Finding out what the loan will actually costs can sometimes requires getting to the full loan agreement.

This doesn’t mean you can’t ask for a title loan quote. We recommend doing just that when we talk about preparing for an online title loan. Use the title loan calculator to optimize your loan term.

Getting the best title loan often requires several quotes from different lenders. This is especially true if you don’t have a title loan company near you.

Locating Accurate Information

Adding to the challenge of finding an accurate title loan quote and interest rate from online title loan companies is the litany of related information published on a regular basis.

Often this includes conflicting information published by title loan competitors. These include many credit card related companies like credit karma that publish numerous articles about title loans.

Additional companies, many related to promoting credit cards, also publish title loan articles.

The challenge in finding accurate title loan interest rate information is real and understandable. Most of these competitors state that title loan interest rates are 300+% APR.

While there are some title loan companies that charge very high rates, not all or even the majority do.

When you factor in the limits that many states impose on title lenders, that number becomes even smaller.

So, where do you look to get accurate title loan information? Credit karma is well known so shouldn’t they fact check their articles?

One would think so, but they are also funded by credit card companies so it is in their best interest to dissuade consumers from getting a title loan.

Add to that the fact that just about every “title loan alternative” list includes a credit card cash advance and it begins to make more sense.

Then, read the advertiser disclosure and it starts to make even more sense why companies would do everything they can to drive consumers away from title loans.

The reality is it is up to everyone to explore options they have. If a title loan solves a short term financial problem, and no lower cost alternative exists, then it is up to the consumer to make that determination. Title loans do have some advantages.

Unfortunately, to make that determination they need an accurate interest rate. This cannot be acquired from a competitor’s article, which is essentially an advertisement with an agenda.

Where to get Accurate Title Loan Information

To get accurate title loan information, including interest rates, do not go by something a credit card company publishes. Just about all of these articles state title loans are for 30 days with a 300+% APR. This is simply not accurate. Many states limit the maximum interest rate to far lower than this.

The only place to get accurate interest rate and related information is directly from the lender. When preparing for a title loan we recommend contacting several lenders to get quotes before deciding which one to go with.

Depending on what state you live in, and which lender you choose, you can end up with an interest rate that is a fraction of the 300% that most competitors write about. This is not always the case, but will be in many states and with many lenders.

Why Information from Competitors may be Incomplete

There is a reason you don’t get facts on a product or service from competitors. They want your business, and will provide partial truths and other incomplete and inaccurate statements to help benefit them.

This is not new, and the title loan industry has a reputation for not being forthcoming about costs, which certainly doesn’t help the situation. Go straight to the source for a real title loan quote. Then, make sure to read the loan agreement in full before signing.

Summary

Car title loan interest rates can be confusing but are essential to understand. When preparing for a title loan go straight to the source for information.

Relying on credit card funded companies for title loan information is not the most efficient or effective way to gather facts. And always read any loan agreement in full before signing.