How does vehicle history factor in to a title loan? Car title loans are secured by the vehicle used for the loan. This means the vehicle is a key part of the title loan transaction.

For online title loans, especially completely online title loans with no inspection, lenders do not get a chance to inspect or appraise the vehicle in person. The lender still needs to appraise the vehicle and assign a value.

For online title loans, the fact that the lender does not see the vehicle in person can make it more difficult to assign an accurate value to the vehicle.

To help with this process the lender uses both pictures and a vehicle history report. The lender combines these two items to perform a “virtual appraisal”.

Virtual Title Loan Appraisal

For completely online title loans many lenders perform what we call a virtual appraisal. During the virtual appraisal, the lender looks at vehicle pictures and examines a vehicle history report to assign a value to the vehicle.

It is obviously much more difficult to appraise a vehicle without seeing it in person. Flaws that are easily discovered with a quick in person inspection are now not nearly as easy to find. In many cases they may be completely hidden.

Vehicle Value Factors

We know title loans are based on vehicle value. So what makes up vehicle value? The main factors include:

- Year

- Make

- Model

- Mileage

- Condition

The one not listed is history, which absolutely has an affect on vehicle value. Generally, vehicle history will also affect condition.

During an in person appraisal it may be easier to determine condition. Some cars may photograph well, others may not.

Vehicle Value for Title Loans

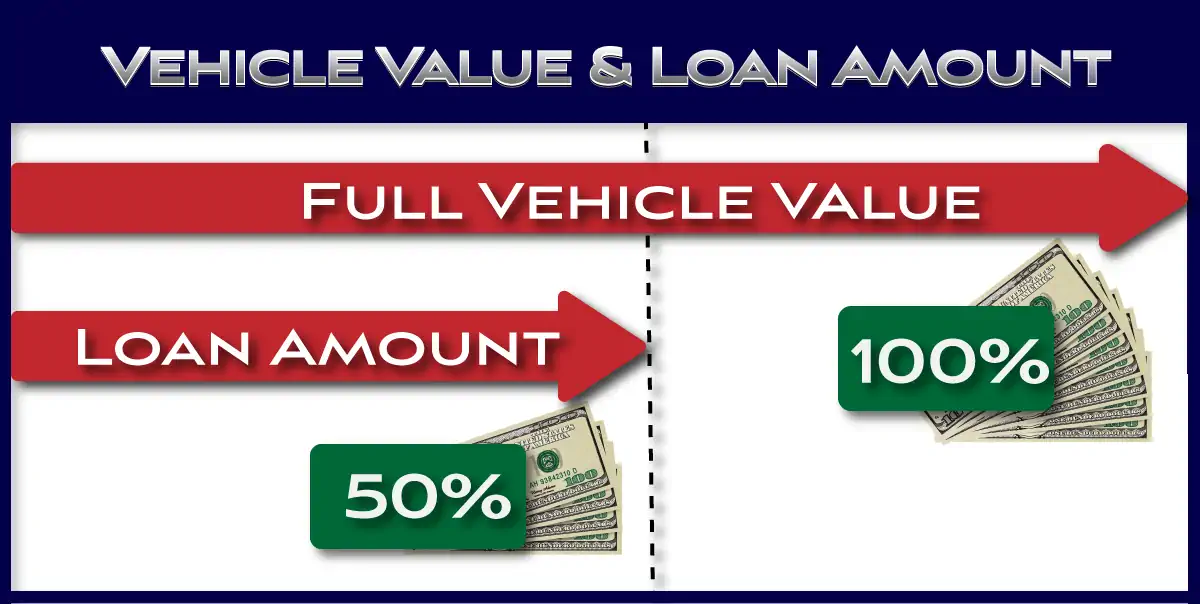

Once the vehicle value is determined by the lender, then a max loan value is assigned. This is usually 50% of the fair market value of the vehicle.

Some states may have slightly different max percentages, but in general using 50% is the standard.

Vehicle History Reports for Title Loans

Now that we know that vehicle history is a key element of an online title loan appraisal, what is the important information in a vehicle history report, and how can we find this information before applying for a title loan?

Getting a Vehicle History Report

You can get a vehicle history report from multiple sources including the two most used carfax and autocheck. Both of these sources will provide a detailed history report for any vehicle. The downside is that both of these have a cost associated with that history report.

Depending on what you expect to find, and how much detail you need, you may want to opt for a free vehicle history report.

How to get a Free Vehicle History Report

While not as detailed as a paid report from Carfax or Autocheck, there are some options for getting a free vehicle history report.

These free reports can tell you if there is anything major in your vehicle’s history that you need to be concerned about prior to applying for an online title loan.

One strategy is to pull a free report, check for any major issues, and pull a paid report if you find something that requires more information.

Vehicle History – Important Factors

As we’ve mentioned aside from mileage and condition, vehicle history is a major contributor to vehicle value. There re a few items in a vehicle’s history that will reduce the value, sometimes substantially.

These include both major and minor factors. For purpose of explaining thoroughly, we’ll list each one separately.

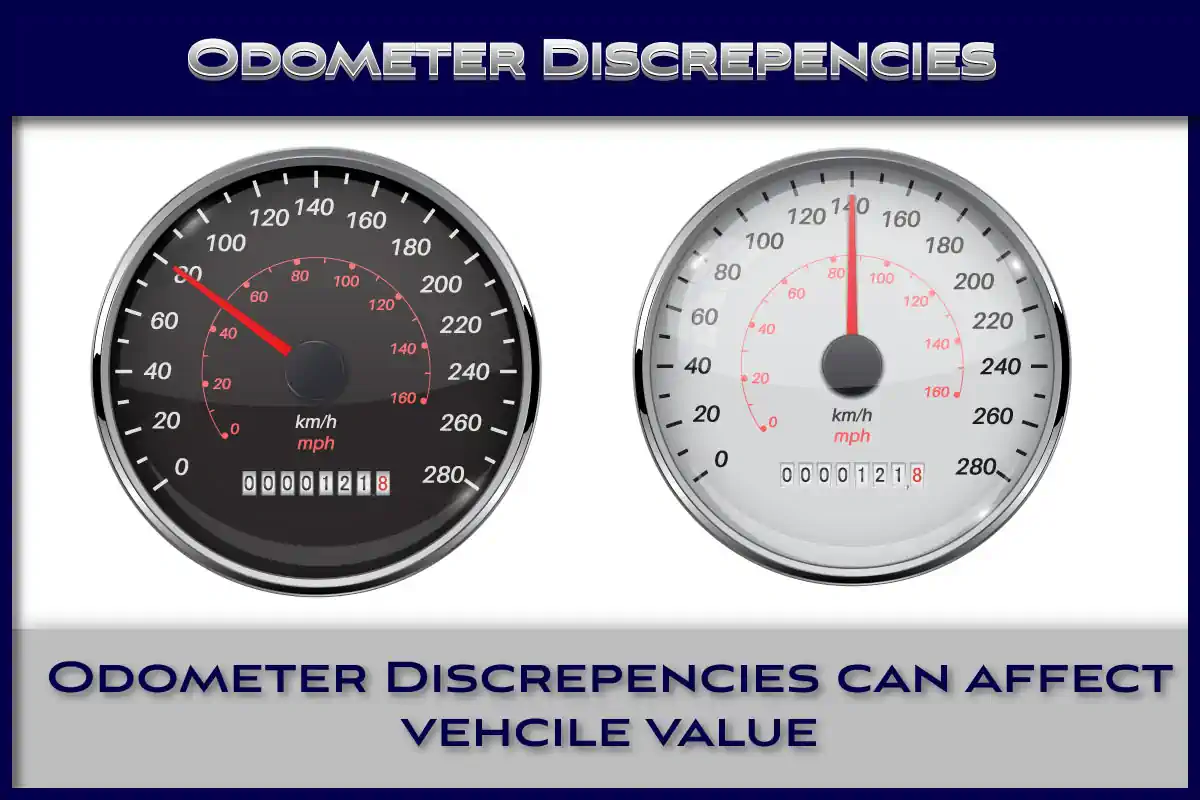

Odometer Discrepancy

Perhaps on of the most important history factors is an odometer discrepancy. These are more prevalent in older vehicles, where tampering with the odometer was more common.

Today this still exists where a vehicle owner may replace the odometer of the vehicle with one from a wrecked vehicle with lower mileage.

Given that mileage has a direct affect on value, an odometer discrepancy has the potential to significantly affect the value of the vehicle negatively.

The problem with an odometer discrepancy is there is no way to know for sure how many actual miles are on the vehicle. Given this, the lender has to assume the mileage is on the high end.

Fire or Flood Damage

Some vehicles that have either fire or water damage are sold at insurance auctions. These vehicles can be refurbished by car dealers and shops and then resold.

The problem with fire or flood damage is that there is no way to know how extensive the damage is. A car that has been fully submersed in water for a period of time is very difficult, if not impossible, to fully restore.

Therefore the value of any vehicles with fire or flood history will be reduced.

Salvage History

Similar to fire and flood, vehicles that have been totaled in a car accident are also sold at insurance auctions. Body shops purchase and repair these vehicles for resale.

Again, the problem with a totaled vehicle is that repairing it to pre accident condition is usually impossible. This lowers the value of the vehicle; in other words salvage history will effect the title loan.

Minor Vehicle History Factors

Some additional vehicle history factors are included in the report. These don’t have as much of an effect on value as those previously listed.

Number of Owners

This is a factor in assessing a vehicle’s value, but not a major one. A one owner vehicle will be worth more than a 2 or 3 owner vehicle. As mentioned this is not a major factor, unless the number of owners is very high.

For example, if a seven year old car has 12 owners, then this raises the question of why? Is there something inherently wrong with the vehicle that leads people to quickly trade it in?

Accidents

If the vehicle has been in an accident this will have a negative impact on the value. The severity of the affect depends on the severity of the accident. If it was a minor fender bender, then the affect will be minor.

On the other end of the spectrum if it was a major accident that required major repairs, this will have a large affect on the vehicle value.

Multiple Accidents

As expected, the more accidents the vehicle has been involved in, the greater the impact in the value. Two, three, four or more accidents will have a greater affect on vehicle value then a single minor accident.

This makes logical sense; consider you’re buying a car. What you you want to see in the vehicle history report?

Vehicle Use

The vehicle use will also affect vehicle value. This can have a minor impact, or a major impact depending on what the vehicle was use for and how long. Here are some examples:

Rental Vehicle Use

Vehicles with a rental history generally don’t have a major impact on vehicle value. On the positive side, rental companies usually maintain their vehicles well.

Rental vehicles are regularly inspected and usually maintained per the manufacturers recommendations. This includes oil changes and a variety of other maintenance procedures.

On the negative side, rental cars can have the tendency to be abused by some renters. This is not always the case. The fact that rental vehicles are regularly cleaned and maintained usually makes up for this.

Taxi Use

A vehicle with taxi history will likely be valued a bit lower. These vehicles usually have high miles, so the mileage has a major affect on the value.

Other Considerations

Some other considerations that may have an affect on vehicle value include how many recalls, and, more importantly, whether or not those recalls have been addressed.

Generally if a vehicle is recalled for a certain reason the manufacturer will address them at no cost. Multiple unaddressed recalls may have a negative affect on vehicle value.

Conclusion

Given the fact that title loans are secured by the vehicle it should be no surprise that vehicle value is used to determine the loan amount.

Additionally, given the number of online title loans today, the fact that you can get a title loan without the vehicle present, it should be no surprise that vehicle history factors in to the vehicle value.

Considering the fact that the lender has to appraise the vehicle without seeing the car in person it makes sense that they would use the vehicle history as a factor in completing the appraisal virtually.

Knowing this, borrowers considering completely online title loans are advised to be aware of their vehicle’s history (if they aren’t already). Now may be a good time to check your vehicle’s history if you have never done so.