A title loan may or may not affect your credit score – it all depends on the lender. There are usually two different scenarios:

- The lender does a hard credit check and reports payment information to the credit bureaus.

- The lender does a soft credit check, but does not report payment information.

For the first scenario, the title loan will definitely affect your credit. This can be positive or negative, depending on whether or not you make your payments on time.

For the second scenario, there will be no effect on your credit score. The loan will not show up on your credit report and a soft credit check will not affect your credit score.

This is not the case for all title loans. To understand how a title loan can affect your credit score, you need to understand the different factors that make up the score. Additionally, it is important to understand how a title loan can have an affect on each of those factors.

How Credit Score is Calculated

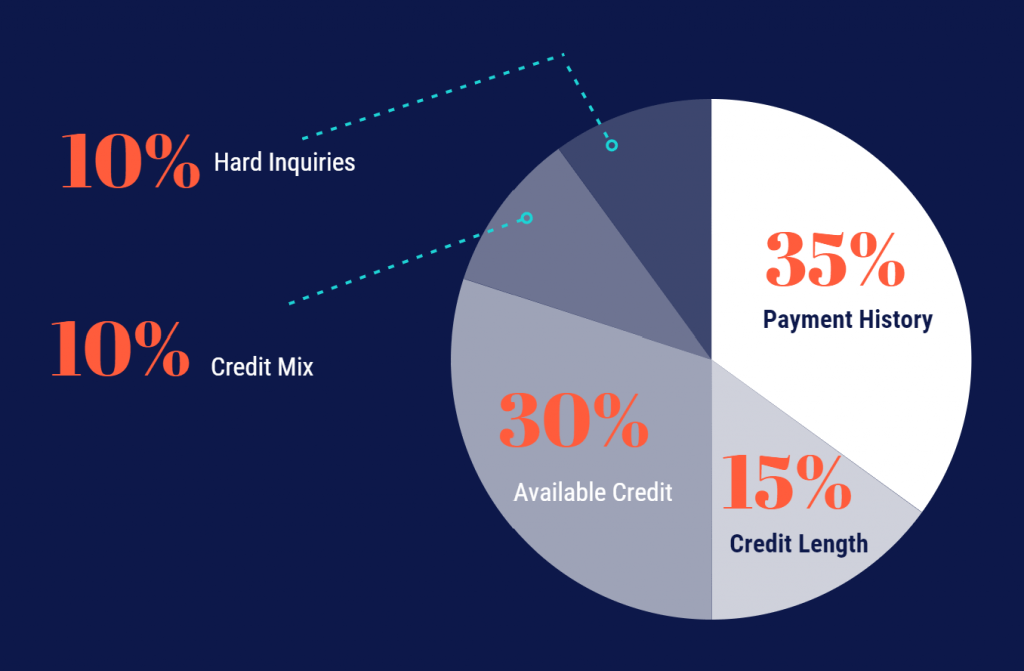

To understand how a title loan might affect your credit score, we need to look at how credit scores are calculated. Credit scores are calculated based on the following key factors:

- Hard Inquiries

- Credit Length

- Credit Use

- Payment History

- Mix of Credit

There are three primary credit bureaus, each has a slightly different way of calculating scores. The affect Title Loans have on your credit scores will be similar regardless of the minor differences in how scores are calculated.

Now, let’s take a look at how a title loan can affect each of these factors, positively or negatively. Once we know this, we can get a general idea of how a title loan will affect your credit, if at all.

Title Loan Affects on Credit Score Factors

1. Hard Inquiries

A hard inquiry occurs when you apply for credit and the lender pulls your credit report. Each hard inquiry slightly lowers your credit score. The more hard inquiries, the greater the negative affect.

Generally, one or two inquiries will not have a noticeable effect, but more than that may,. If the title lender does not check your credit, your credit score will not be affected. If they do check your credit then you will have a hard inquiry added to your credit report which will slightly lower you score.

2. Credit Length

The credit length factor is based on how long you have had credit and the average length of each account. Again, if the lender does not check credit or report to credit bureaus, your score will not be affected.

If the lender does check your credit, but does not report the loan to credit bureaus, then your score will not be affected. If the lender does report the loan, then it will affect your credit score.

The severity of the affect will depend on how many accounts you have on your report and the average age. If you have many accounts with a long history, adding a title loan will have little affect.

If you only have a few accounts that are fairly new, adding a title loan will lower your score in the short and medium term. If you repay the loan in full, your score will increase over the medium to long term.

3. Credit Use

One of the biggest factors that make up your score is credit use or outstanding debt. This is the total amount owed compared to the available credit. If the lender does not report the loan, your outstanding debt will not change and therefor your score will not be affected.

If the lender does report the loan, your outstanding debt will increase and your score may decrease as a result. We go over a creative way to use a title loan to increase your credit score, quickly, to facilitate getting a better interest rate on a large purchase.

4. Payment History

Another major factor in calculating your credit score is your payment history. This takes into account how many payments you have missed, and by how many days (30, 60, 90, etc). If the title loan is not reporting to agencies, missing a payment will not affect your credit score. Similarly, making all your title loan payments on time will not increase your credit score either.

If you are trying to rebuild your credit over the long term and are confident you will make all of your payments on time, you may consider finding a lender that reports the loan to credit bureaus.

Just keep in mind that in the short term your score will decrease as a result of the hard inquiry and increased outstanding debt. If you are looking for a fast way to increase your credit score using a title loan read our recent post on how to use a title loan to increase your credit score.

5. Mix of Credit

The mix of credit has an affect on your credit score. A mix of both secured and unsecured loans show an ability to manage different types of loans. Having a title loan on your credit report will help your mix of credit in the long run.

Similar to payment history, your short term score may be reduced slightly after you get the loan if it is reported to the credit bureaus. If you make all of your payments on time and repay the loan, your score should increase.

Can a Title Loan Hurt my Credit?

As discussed, a title loan will have a negative affect on your credit score if the lender pulls your credit report and reports the loan to the credit bureaus. If the lender does not run a credit check the title loan will not affect your credit score.

Can a Title Loan Increase my Credit Score?

There are two ways to use a title loan to increase your credit score. The first way, covered in detail in our post on how to use a title loan to increase your credit score, can be used to see the affects quickly.

This is typically used prior to making a large purchase like a home or piece of property. It can also be used prior to applying for a job where a credit check is required.

The second method takes a bit longer and may lower your score in the short/medium term but will help increase your score over the medium/long term assuming you make all of your payments on time. It involves finding a lender that does check your credit and does report to credit bureaus.

Because they check your credit, there will be a additional hard inquiry on your credit report. Your outstanding debt will also increase, which may lower your score. But, if you make all of your payments on time, your score should increase over the long term.

Can I get a Title Loan with No Credit Check?

Yes, there are online title loans with no credit check and no inspection. It all depends on whether or not the lender has a policy to check borrowers credit or not. Most online lenders will perform at least a soft credit inquiry to verify information.

Conclusion

Title loans, in most cases, do not affect your credit. There is, however, and innovative way to use a title loan to increase your credit score quickly. If you are interested in a title loan make sure to learn how a title loan works.

Additionally, if you are in the process of rebuilding your credit over a longer term, getting a title loan from a lender that reports the loan to credit bureaus may help with that. It will, however, lower the score in the short term.