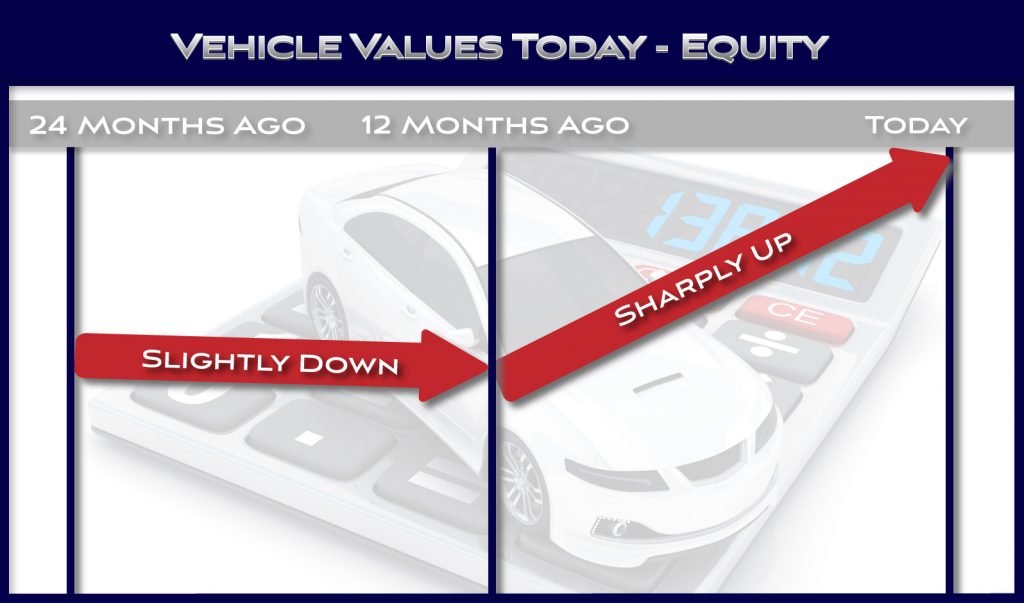

Used car valuations have increased quite a bit over that past year. A vehicle that was worth $5,000 12 months ago can be worth $7,000 or more today. This has both positive and negative implications for vehicle owners.

One positive impact is that any vehicle owner that may have owed more on a loan than their vehicle was worth, known as being ‘upside down’, may now have equity in their vehicle, even if only a little bit.

One negative is vehicle owners that live in states where personal property is taxed will likely be stuck with a higher tax bill this year. If you plan on selling or trading in the vehicle this tax increase may be worth it.

Recent Used Car Valuation Trends

For the majority of makes and models the trend in used car valuations has been a move up, in many cases a significant move up. According to Edmunds the average used car price increased by 27% during the past year. This is compared to the typical increase of around 1%.

This is caused by the shortage of new cars, leading many buyers to look for used cars. In other words a simple case of supply and demand. Right now, the demand for used cars is higher than the supply so basic free market laws lead to an increase in price of used cars.

Car Title Loan Relationship

So what does this have to do with car title loans? There are two key aspects of the current used car market that have a direct effect on title loans:

- Equity in vehicles can lead to higher max loan amounts

- Refinancing a title loan may result in a better valuation

Car Title Loans versus Selling and Buying a Car

Considering the fact that valuations have invreased significantly, it may be tempting to sell your current vehicle; I know I have considered it. My vehicle value has increased from $7,000 to approximately $10,000.

My first thought was to sell it for top dollar and buy something else. Then when I looked into it, the problem was buying something else resulted in paying top dollar for it. So the net result was not much different than a year ago.

The other option vehicle owners have is getting a title loan using the equity in their vehicle. With valuations increasing, so will the equity.

If considering a title loan you will need to decide whether you prefer an in-person or online loan. There are multiple types of online versions, including completely online title loans with no inspection.

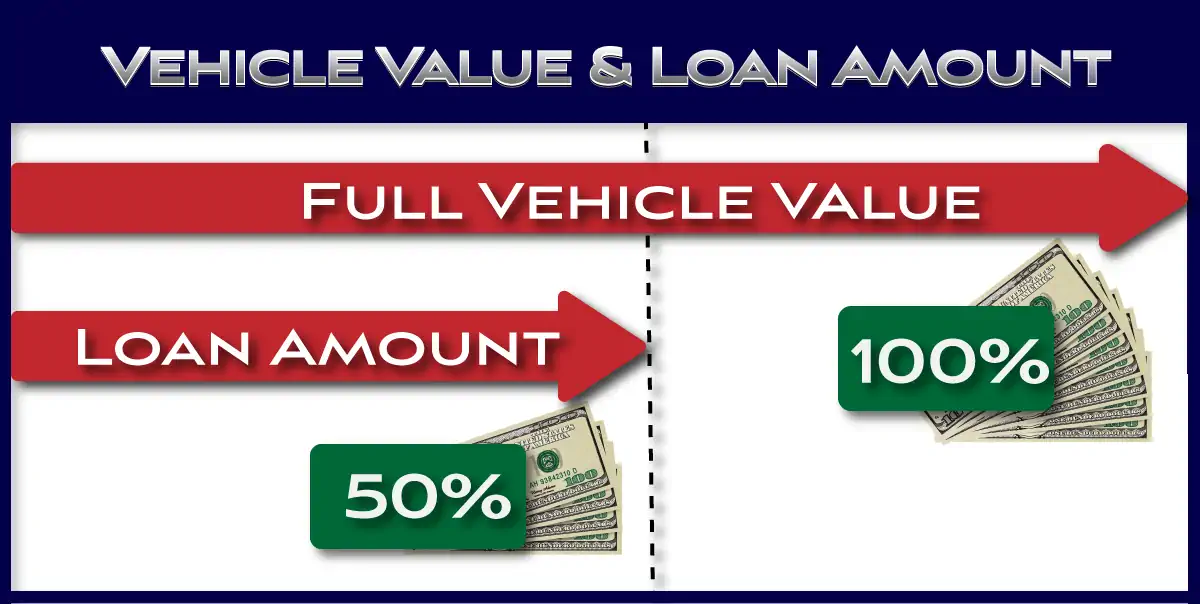

Vehicle Value and Title Loan Amount

The first is vehicle value. The max loan amount is directly related to vehicle value. Therefore, if the vehicle value increases by a certain amount, the max loan amount increases as well. This is not a dollar for dollar increase though.

The typical online title loan amount is capped at 50% of the vehicle’s fair market value. This means for every dollar the value increases, the max loan increases by $.50. So, if your vehicle is worth $2,000 more today then your max loan amount would likely be increased by $1,000.

Refinancing and Existing Title Loan

If you have an existing title loan, and needed more than you were able to borrow this could lead to a situation where the loan caused more problems if you were unable to solve the short term funding need.

With the increase in used car values it may be possible to get a title loan buyout that my be able to provide the funding needed to improve your situation. This should be looked at carefully and all options weighed.

Max Online Title Loan Amount

As we’ve stated several times always borrow only what you need to meet your requirement for short term funds. Don’t let a title loan company talk you into borrowing the max just because you qualify for it.

If you are unsure of your requirements we suggest you spend a little time properly preparing for the loan. Online title loans have additional requirements like vehicle pictures.

The fact is car title loans are expensive forms of credit. The more you borrow the more interest you will need to repay. Failure to repay the loan can result in repossession and loss of your vehicle. Make sure to understand how interest rates effect the cost of the loan.

Conclusion

Regardless of whether you plan on getting a title loan or not, understanding how much your car is worth is always a good idea. If you do plan on considering a title loan then understanding how much your car is worth is a must.

There are several companies that specialize in used car valuations. Use one of these to get your vehicle valuation, not a form on a title lender’s website. The companies that specialize in vehicle valuations use real world sales data and a significant amount of research.

You can visit Kelley Blue Book, Edmunds, NADA, and others to get your own vehicle valuation. We suggest you use one or more of these tools provided by these companies to get a good idea of what your vehicle is worth.

At that point if you are interested in a title loan make sure to prepare properly and choose the lender that offers the best deal for your specific situation.