Considering the fact that interest rates for every type of loan have risen this year, we though updating this post was necessary. The Federal Reserve has raised the target for the effective federal funds rate (EFFR) to 3.75 – 4.00%.

This is a significant change from the near zero interest rate environment of the past decade. This has an effect on all loans, not just car title loans. In short, it will cost more to borrow money. We’ll get into the specifics as this relates to title loans.

What are Car Title Loans?

Car title loans are a way to borrow money using your vehicle’s equity as collateral for the loan. These are also known as Title Pawns, Auto Equity Loans, Online Title Loans, and Installment Loans.

Title loans are frequently used for emergency or time sensitive financial needs; making instant online title loans something borrowers are interested in because of their ability to provide funds quickly.

The fact is there is a trade-off with being able to borrow money, fast, without the need for good credit. This trade-off is often the total cost of the loan.

Car Title Loan Cost Factors

There are two key factors that effect the cost of a car title loan – fees and interest rates. Fees should be fairly straight forward depending on the state. If you live in a state that permits high fees, make sure to look at the total moan cost, not just interest costs.

We suggest finding a lender that does not charge many fees, and does not charge unreasonable fees. This leaves the interest rate as the main factor we’ll look into in this post.

In addition to the cost of the loan it is also important to determine how much you can borrow with a title loan.

Interest Rates

We have written quite a bit about title loan interest rates and fees, so for the purpose of this post we’ll focus on a few rates and take a look at how the different rates effect the total loan cost. With rising borrowing costs for everyone, including lenders, title loan costs are likely to increase as well. This makes it more important than ever to understand how interest works.

So what is a typical title loan interest rate? The answer is, unfortunately, it depends. In certain states, the rate can be as low as 30% APR. On the other end of the spectrum in some states the rate can be as high as 300% APR.

This is a huge range and can have massive implications on repayment costs. This is especially true for loans with monthly installments. Before we get into more details it is important to note that there are two type of title loan repayment terms: Single payment and monthly installment.

Single Payment Loans

A single payment title loan has one payment that is due in full at the end of the loan term. These are usually 30 day loans and are often for smaller dollar amounts.

A typically example is a $1000 loan for 30 days. These loans usually have a higher interest rate than monthly installment loans.

The following table shows the total loan cost for a $1,000 single payment 30 day title loan with an interest rate of 80% APR, 160% APR, and 250% APR.

| APR | Interest Charge | Total Loan Payment |

|---|---|---|

| 80% | $80.00 | $1,080.00 |

| 160% | $160.00 | $1,160.00 |

| 250% | $250.00 | $1,250.00 |

Single payment loans are fairly straightforward and very short term. They only get complicated and long if you end up rolling them over. Always make sure you can repay the loan in full by the deadline to avoid having to roll over the loan.

We cover rollovers in another post; in short in many cases the principal remains the same while you continue to pay high interest charges each month.

Monthly Installment Loans

Monthly installment title loans have a payment of the same amount due each month for the loan term. These can be anywhere from a few months to a few years. These loans are amortized over the loan period, and a portion of every payment is applied to the principal value of the loan.

In some ways this makes it easier to repay the loan, assuming the interest rate is reasonable and the term isn’t too long. The two things you need to be aware of with a monthly installment loan are:

- The higher the rate, the higher the loan costs

- The longer the term, the higher the total loan costs

- Increasing both the rate and term results in a significant increase in total loan cost

This means you should keep the loan term as short as possible to save on interest. This is especially true if the interest rate is high.

Monthly Payment versus Loan Term

The main reason to increase the loan term, from say 6 months to 12 months is to lower the monthly payment. Given the fact that title loans are secured loans it is essential that the borrower be able to comfortably afford the payment.

One way to reduce the monthly payment is to extend the loan. With high interest loans, this only makes sense to a certain point. As you extend the loan, the interest charges get to a point where extending the loan can significantly increase the total loan cost while only decrease the monthly payment minimally.

Finding that balance is important to ensuring your title loan is both affordable and reasonable. This means comparing different loan terms and monthly payments, while keeping an eye on the total loan cost, to find the term that works for you.

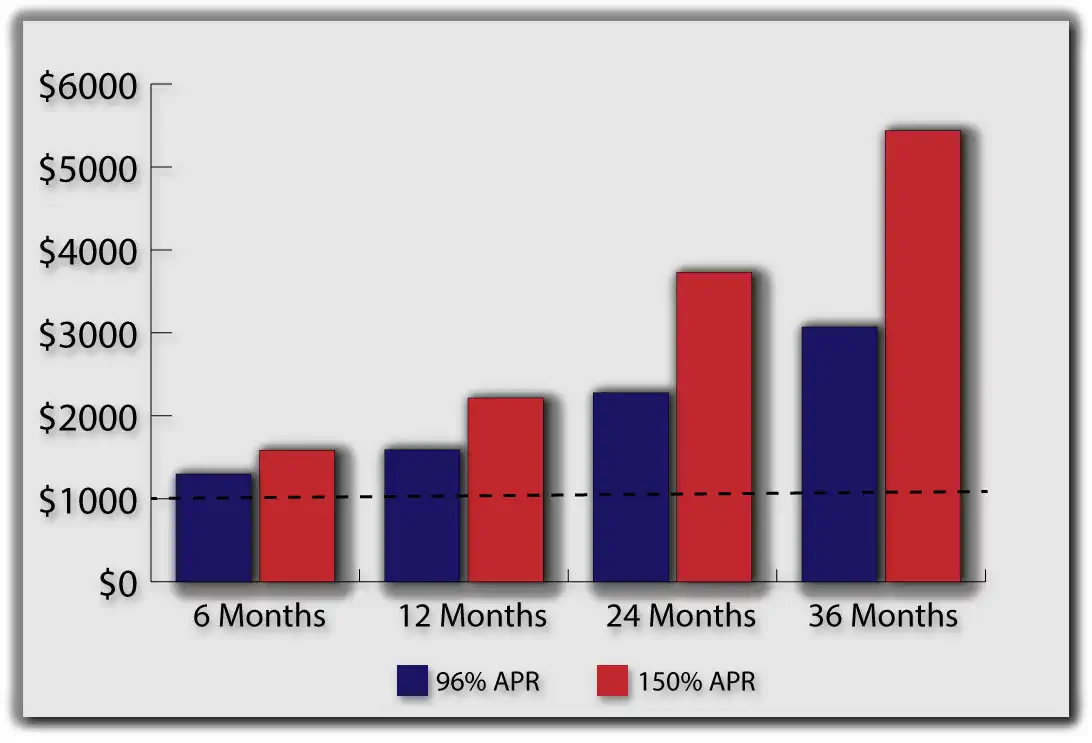

We’ll take a look at a $1,000 title loan with two different interest rates and four different terms. For purposes of this post we’ll use a 96% APR loan and a 150% APR loan. For comparing terms we’ll go with 6, 12, 24, and 36 months.

The two interest rates compared were 96% and 150%. As you can see from the graph, both increase as the loan term increases; but the 150% loan increases far more. In fact, the total loan cost for this rate for a 36 month term is over $5,000, or over five times the original principal.

Example of Actual Loan Costs

Actual title loan costs can be higher than those presented in this article. The following is a real example from a lender operating today:

| Loan Amount | APR | # of Months | Total Cost |

|---|---|---|---|

| $2,000 | 149.99% | 48 | $12,203 |

| $4,000 | 149.99% | 48 | $24,406 |

| $10,000 | 149.99% | 48 | $61,015 |

That is not a typo. It actually costs over $60,000 to borrow $10,000 for four years. This is with an APR of approximately 150%. Some title loans can have higher APRs making the total loan cost even higher. This just highlights the fact that title loans are not long term solutions.

Summary

Title loans are meant for short term problems for a reason, they are meant to be short term loans. Extending a loan for several years is not a good idea, even though many lenders are now offering these longer terms. Rising borrowing costs are likely to increase the cost of title loans.

When shopping for a title loan keep this in mind and remember to always consider the total loan cost in addition to the monthly payment. Nobody wants to end up repaying over 5 times or more than what they borrowed. If you happen to be stuck in an unfavorable loan, then it is worth considering a title loan refinance.