Fast Title Lenders spends quite a bit of time writing about online title loans. This is to try to inform potential title loan customers about how they work, what they cost, and how to prepare for one. We do this as much as possible with facts and not opinions.

The fact is there are a lot of companies writing and publishing content about online title loans. Unfortunately much of this information is out of date, incomplete, or just misleading (either purposely or inadvertently).

In this post we’ll concentrate on a few key points that will hopefully help potential borrowers make sense of an ever cluttered landscape of advertisers and competitors.

Key Online Title Loan Facts

First, let’s cover some key online title loan facts. These are simply facts, not opinions of any one person or company.

Online Title Loans Can Have High Interest Rates

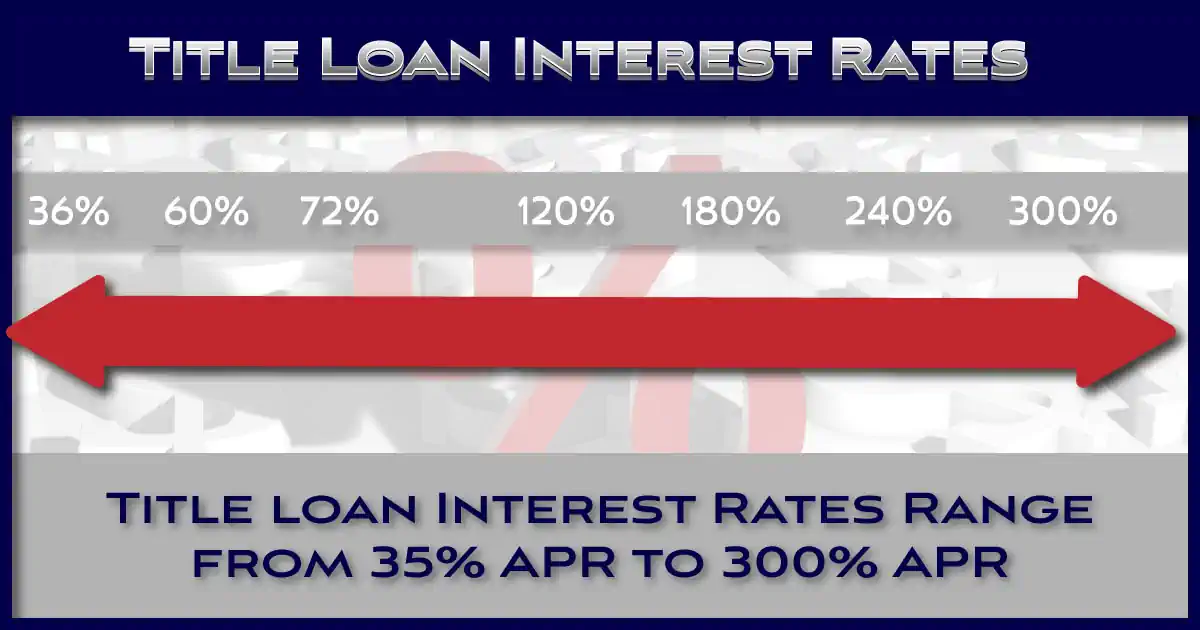

The first fact is that online title loans can have high interest rates. This is especially true when compared to other loan types. The part that is often miscommunicated, either on purpose or inadvertently, is just how high these rates are.

The truth is it depends on the state you live in and the lender you go to. Rates can vary from less than 36% in some states to as high as 25% per month, or 300% APR, in others. The typical title loan is somewhere in between, not on the high end as portrayed in many opinion articles.

Seemingly reputable publishers have articles stating that title loans online have an interest rate of 300% APR. This is a very high rate, a loan with this rate would generally not be a good idea for anyone.

The problem with stating this as a fact is it is simply not true for many online title loans. In fact, as stated some states limit lenders from charging more than 36% APR, far lower than the stated 300%. Other states limit rates to lower than 300%, much lower in many cases.

To find out how much different title loans with different rates actually cost you can use our title loan calculator. It will display the actual loan cost for any amount with various rates. Just remember to distinguish between the monthly rate and the APR.

These are Secured Loans

Online title loans are also secured loans. This means the vehicle used to get the loan is used as collateral for the loan. Should the borrower default, the lender has a claim to the vehicle.

A Lien is often Placed on the Vehicle

To secure the loan and make sure the paperwork is correct, the lender usually puts a lien on the vehicle. A lien is the formal way of securing the loan with the collateral. Should the borrower default, the lien provides the lender with what they need to recover their costs.

This is the reason why a lien free title is often at the top of the list of online title loan requirements. It is possible to get a title loan without a lien free title, assuming you are close to paying off an existing loan or are looking for a title loan refinance.

The Vehicle Can Be Repossessed

Since the loan is secured by the vehicle, if the borrower does default and does not attempt to cure the default, the lender may repossess the vehicle to recover their costs. This is often the last resort for lenders as usually repossessions are not the best way to end a loan.

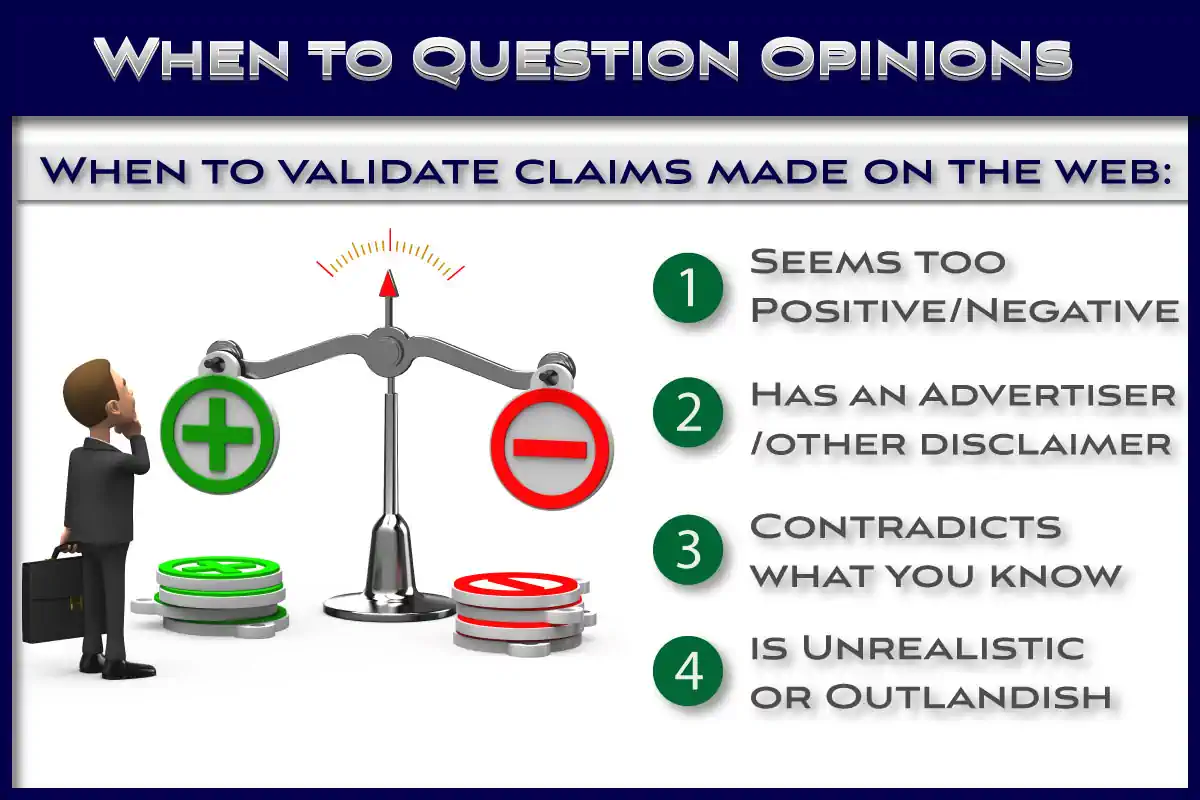

Online Title Loan Information to Question

In this day where everyone publishers information on the internet to generate clicks it is difficult to know what is accurate and what is not. One way to determine if an article you are reading has any sort of bias is to check to see if there is an advertiser disclosure.

There is an article right now, ranking very high on Google, about ‘How Online Title Loans Work’ that contains one of these advertiser disclosures.

The company that published this article makes money from their sponsors, credit card companies and banks. This article states all of the negative aspects of an online title loan, cites information collected almost a decade ago as fact, and provides the following three alternatives:

- Personal loan

- Credit Card Cash Advance

- Payday Alternative Loan from a Bank

It is easy to see that the goal of this article is to target potential title loan customers, provide them with outdated facts and negative information about title loans, and then steer them towards their advertisers.

Unfortunately this does not provide the reader with the full picture of how online title loans work and is obviously meant to discourage readers form seeking a title loan.

The article seems very legitimate because it is citing legitimate sources, but the problem with using a study published 7 years ago as a source is that there were not many online title loans 7 years ago. Most were in person, and laws in many states have changed since then.

Suggestions for Finding Facts Online

The best way to find out how online title loans really work, what they really cost, and other related information is to read from different and multiple sources. The fact is that every company is going to put their own spin on something to benefit them.

Properly prepare, take some time to do some research, and you will be glad you did. This way you can be armed with information prior to contacting a lender for a completely online title loan.