How do car title loans work? Car title loans work differently in each state which means there is no simple answer to this question.

To help fully answer this complex question, instead of partially answer like most sources, we put together a comprehensive guide to aid in answering the various questions related to how different car title loan types work.

The short answer: Car title loans are a type of fast loan secured by your vehicle. They are a way to borrow money using the equity in your vehicle. You pledge your vehicle as collateral in exchange for quick cash. The lender holds your title until the loan is repaid.

Car Title Loans work Differently in Each State

The fact that car title loans work differently in each state means that repayment terms and interest rates can and do vary widely from state to state and even lender to lender within states.

Each state treats car title loans differently and each lender has different rates and fees.

To better explain how car title loans work in each state, we can break states up into four high level categories. Each state can fit into one of these categories:

- Very few or no regulations – this provides lenders a lot of flexibility to operate using business practices that are not always consumer friendly.

- Some restrictions – some regulations on the maximum interest rate, requirements for returning surplus from the sale of a vehicle, and other consumer protections.

- Heavy restrictions – some states have restricted car title loans to the point that no lenders operate. This means that technically they are permitted, however the restrictions are so sever that lenders chose not to do business in these states.

- Not permitted – some states do not allow them at all.

The fact that car title loans work differently in each state can make explaining how they work a bit complicated. This list shows the states that allow title loans; we’ll cover some specifics later.

For example, title loans in Florida are 30 day single payment loans. This means the entire loan amount, plus interest and fees, is due in one single payment. This is true for all single payment title loans and title pawns.

Additionally, car title loans online are becoming more widely available. This gives consumers greater access to car title loans with more competitive interest rates (assuming they choose their lender wisely); even when they don’t have a title loan place near their location.

The addition of both more lenders and more online title loan companies to the market can make it difficult to find the best title loan. A key to making sure you get a good deal on a car title loan is understanding how they work.

This guide covers how car title loans work. We start with preparing for a title loan, shopping for a title loan, and how both single payment and monthly term title loans work. We cover everything you need to know about car title loans.

Learning How Car Title Loans Work

We highly recommend to anyone considering a title loan spend some time learning about how they work. This includes how to prepare, apply, get approved, make payments, and get your title back.

We strongly recommend doing this before signing the loan agreement. Preparation is also an important part of getting a title loan; one that is often overlooked.

When preparation is overlooked, borrowers can end up with a title loan with unfavorable terms and conditions.

Why Title Loan Preparation is Important

The consequences of defaulting on a title loan range from late fees and interest charges to vehicle repossession. Before entering into a loan agreement make sure you understand all related elements of how title loans work.

Some lenders are more likely to repossess the vehicle than others; one of the many reasons choosing your lender is very important. We go over the other reasons a bit later.

Additionally, some title loans have very high rates making repayment extremely difficult. It is worth a few minutes of your time to learn exactly how title loans work, as well as how to get the best deal on a title loan.

Interest accrues daily, so understanding how title loan interest works will make it easier to decide whether or not a title loan is worth it. These reasons make it very important to learn everything you can prior to getting a title loan.

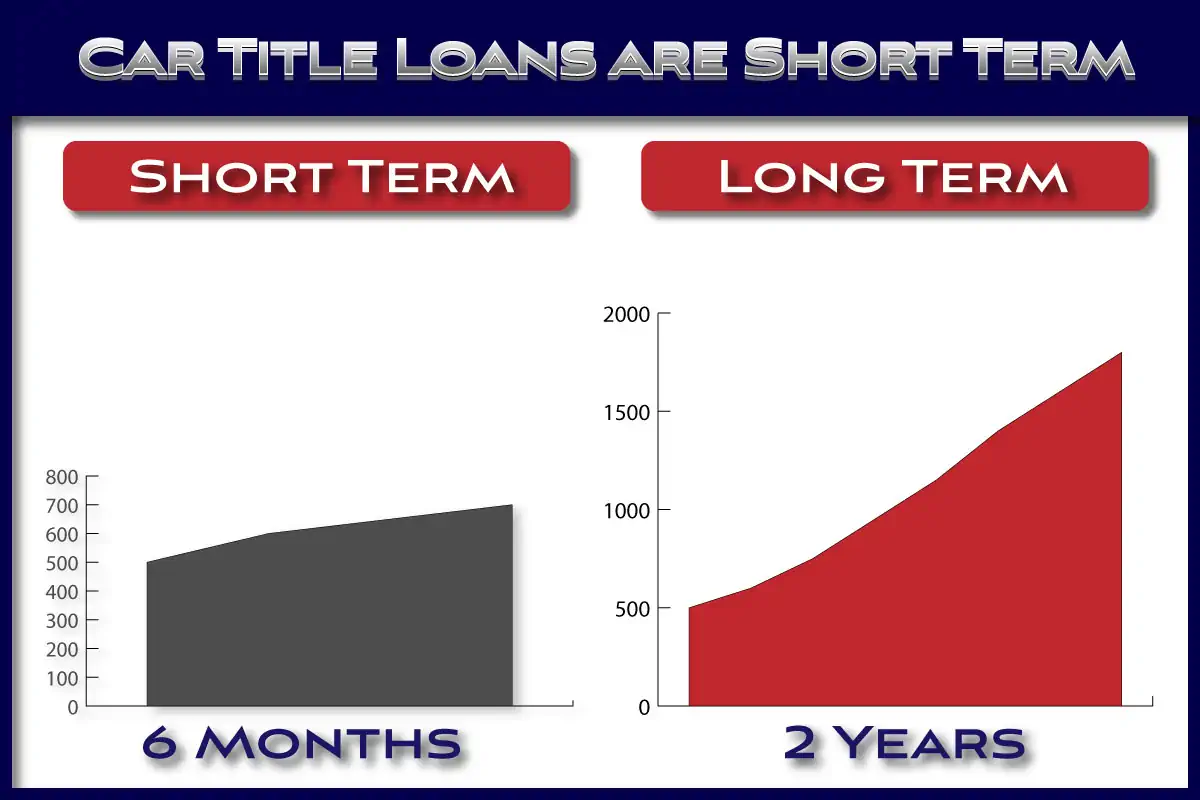

Car Title Loans are Short Term Solutions

Car title loans are meant to solve short term financial problems. Trying to make a car title loan long term leads to excessive costs. Do not make the mistake of trying to make one of these loans a long term solution.

Some lenders are offering longer term (2+ years). These can be very expensive.

In cases where title loans are amortized for two or three years, and even longer the total loan cost ends up being 3, 4, or more times the original loan amount. This is not a reasonable loan nor a solution to a financial problem.

We detailed this in a recent post on what car title loans really cost. It is worth a quick read and a look at the graphs if you are considering a title loan with a long term.

What is with Title Loan Names?

This wouldn’t be a complete guide to how title loans work unless we addressed title loan names. You may have noticed title loans are sometimes called different names in different states. This has to do with the laws in each state.

Some states do not allow title loans, so lenders use other names like “auto equity loans”, “cash advances”, “vehicle lines of credit”, and others.

They are also known as title pawns and pink slip loans. For the sake of simplicity, we’ll use the term “title loan” or “car title loan” throughout the rest of the article to refer to any loan where the vehicle is used as collateral.

Understanding Car Title Loans

To learn how car title loans work we first need to understand a car title loan. We will also briefly cover secured loans versus unsecured loans.

What is a Car Title Loan?

A car title loan is a way of borrowing money, quickly, using the equity in your vehicle as collateral. With a car title loan, you borrow money against the equity in your vehicle by pledging your vehicle as collateral for the loan.

This is important to remember – you are pledging your vehicle as collateral for the loan; not just the title. Should you fail to repay the loan you can lose your vehicle.

You do leave the title with the lender until the loan is repaid. In most states the lender records their lien on your title. The lien is released and your title returned to you when you make your final payment.

Why are Car Title Loans used?

Given the amount that vehicles have risen in price over the past decade there are more people with a significant amount of equity after their car loan is repaid.

Car title loans serve a purpose by providing access to that equity. You can use the funds for unplanned expenses, emergencies, medical bills, and any other need. They are typically used to cover short term financial shortfalls.

The fact that you can borrow against the equity in your vehicle, very fast, makes title loans widely used for emergency and urgent cash needs when other options are not available.

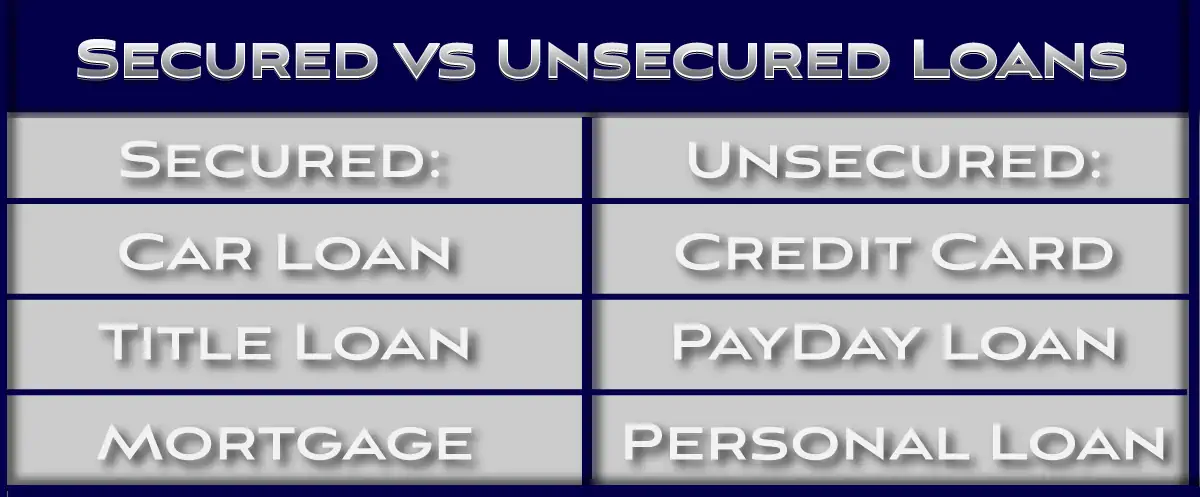

Car Title Loans are Secured Loans

You may have read that car title loans are secured loans. This is true. So, what is a secured loan and what is an unsecured loan?

Secured Loans versus Unsecured Loans

It is important to understand the difference between a secured loan and an unsecured loan. Secured loans have collateral associated with them, unsecured loans do not.

If you default on a secured loan, the lender can make a claim on the collateral.

For a car title loan this can mean repossession of the vehicle used to secure the loan. If you default on an unsecured loan, the lender has to try to collect the funds.

In many cases, they will pursue a court judgement. An easy example of an unsecured loan is a credit card.

This is a major difference and the primary reason many title loans do not require a credit check. You agree to pledge your vehicle as collateral for the loan and the lender holds your title while you make payments.

Once you make your final payment, the lender returns your title to you. Fail to make a payment, or violate the terms of the loan agreement, and the lender can repossess your vehicle.

This is one reason it is very important to choose your lender wisely, we’ll go over that later.

Now that we know what a title loan is, we can move on to answer the question “how do car title loans work?”.

How do Car Title Loans Work?

We’ve mentioned that car title loans use you vehicle as collateral to secure the loan. This is at the heart of how car title loans work for two reasons.

The first is related to loan approval. The value of your vehicle is used to determine the loan value, not you credit score. This is important for anyone looking for a no credit check title loan.

It is a good idea to figure out your vehicle’s value prior to applying for a title loan. This will give you an idea of how much you may be able to borrow.

This is one of the benefits of a title loan and is good news for those without perfect credit. In most cases, there is no hard inquiry on your credit report when getting a title loan.

Some title lenders do check your credit, so make sure to ask your lender if that is a concern.

Are Car Title Loans Bad?

Title loans, and more importantly, certain title lenders, often have a negative stigma attached to them. Generally, negative stigmas don’t come out of thin air.

Certain lenders have earned their reputation through the way they treat their customers. This reputation is often earned through charging very high rates.

Additionally, there are plenty of articles detailing why title loans are bad and why you should stay away from them at all costs.

It is worth noting that many of these are published by car title loan competitors (financial institutions and credit card company related).

In some cases, this may be true, and in others, false. It depends on your specific situation. If you are considering a car title loan make sure to perform a cost benefit analysis to determine if the title loan is worth it.

Not every situation can be improved with a title loan despite what some lenders may advertise.

We started Fast Title Lenders to provide an alternative to these lenders by offering online car title loans at lower rates. Our view is to provide customers with the information, including costs, to make a determination on whether or not a title loan is the right choice for them.

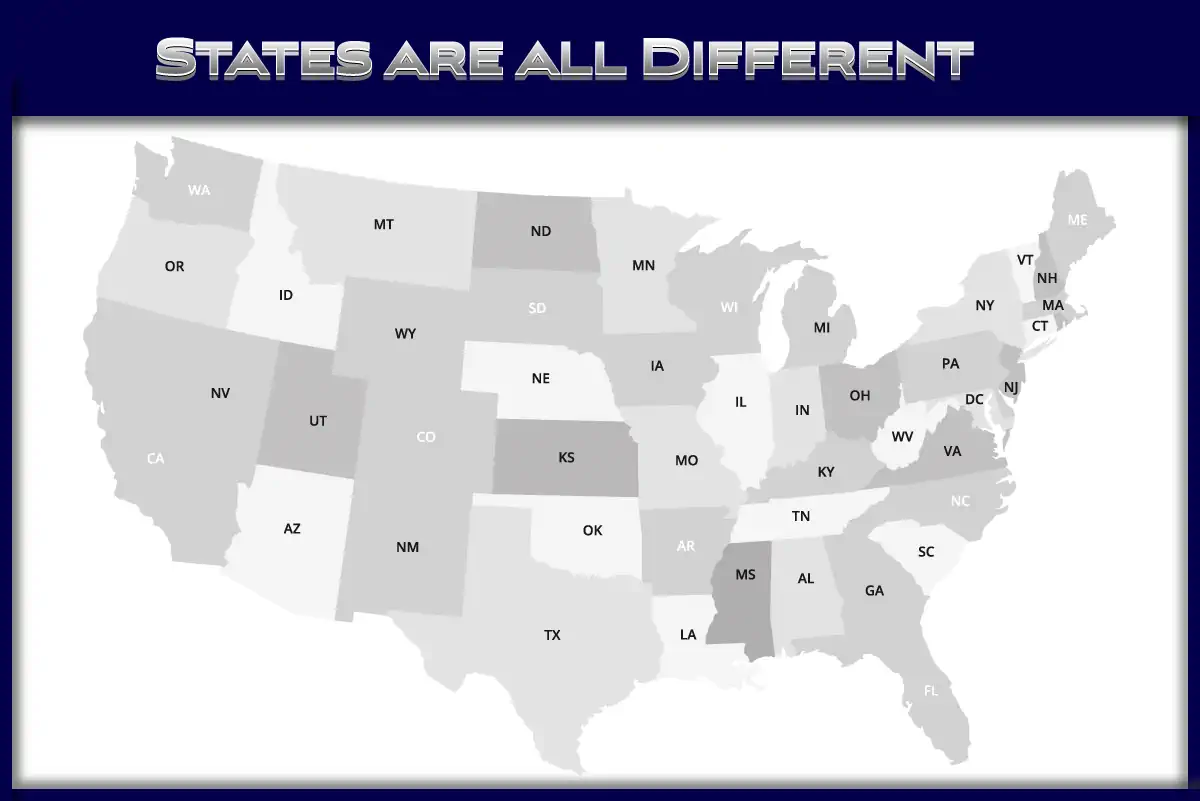

How Title Loans Work – Every State is Different

We mentioned that title loans work differently in every state. Not all states allow title loans and some states that do have few restrictions in place.

Others have adopted rules that limit the amount of interest a lender can charge. This means how car title loans work is dependent on the state you reside in.

Where you live will determine how your car title loan works. Some states have 30 day loans, others monthly installment loans. Additionally, not all states allow title loans, so for some they may not be an option.

Check the title loan laws in your state, the link opens a map that shows the states that allow title loans with a summary of restrictions in each state. Once you find out whether or not car title loans are available in your state you can figure out if one is right for you.

This only adds to confusion if you are shopping for a title loan and are reading loan terms from another state. Car title loans are officially regulated in some states, and offered in other states under different names as previously mentioned.

For simplicity, we are going to explain how the two main types of car title loans work: Monthly installment loans and Single payment loans.

How do Different Types of Title Loans work?

As previously noted Car Title Loans are regulated at the state level and are not available in every state. We can break down title loans into two general types of title loans; single payment loans and monthly installment loans.

These loans are structured very differently and it is important to understand the differences between these two types of loans. The state you live in will dictate the type of car title loan available to you.

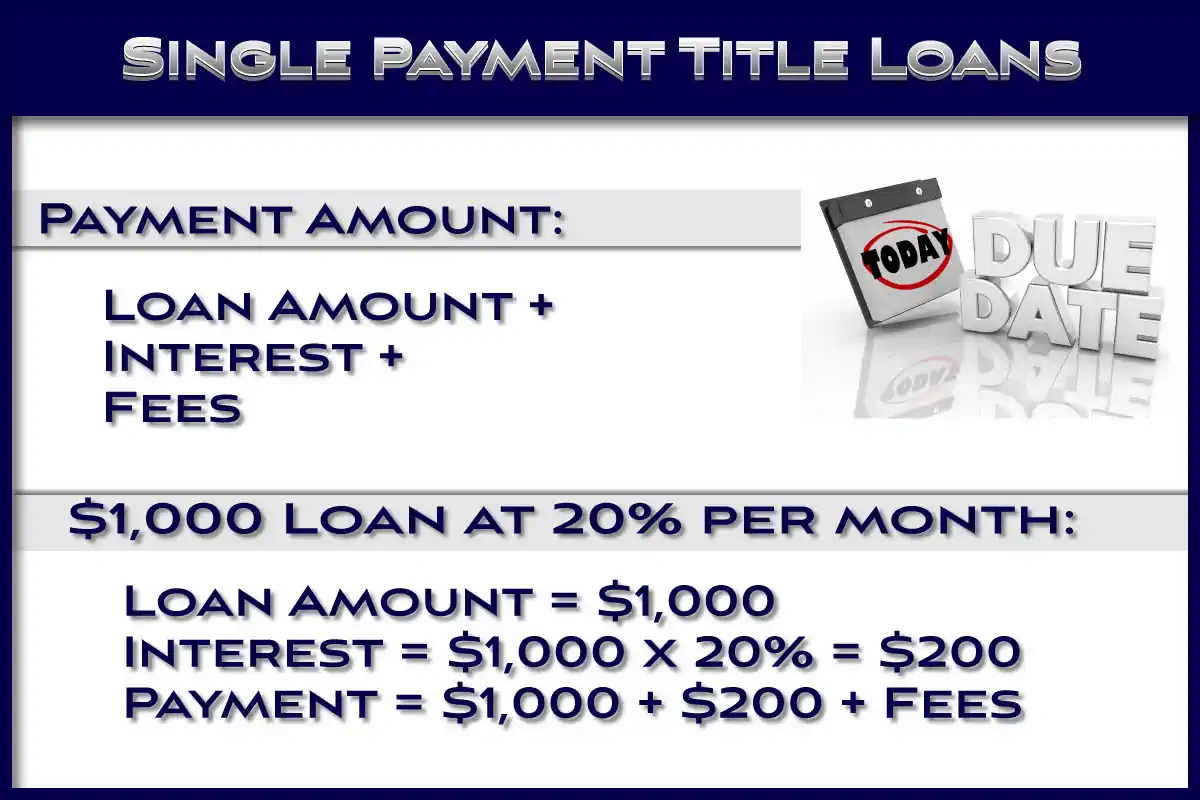

Single Payment Car Title Loans:

Some states have single payment car title loans. These car title loans work similar to payday loans in that you borrow a fixed amount and repay the entire loan plus a fee at the end of the loan period.

They are for a very short period of time, generally 30 days.

You must repay the entire loan in one lump sum plus any fees. These types of loans are available in Alabama, Florida, Georgia, Idaho, Missouri, Nevada, New Hampshire, and New Mexico.

Single payment loans are generally more difficult to repay and can have very high interest rates. In some states, interest is capped but fees are permitted.

This can make the actual costs difficult to figure out in addition to difficult to repay. There are also some additional challenges related to these types of loans.

Single Payment Loan Challenges

The reason they are difficult to repay is because you only have a very short period of time to repay the entire loan plus the interest and fees.

As an example, if you borrow $1000, you may need to repay $1200 after interest and fees in just 30 days. If you needed to borrow $1,000 this assumes you had no savings at the time.

30 days may not be enough time to save up $1,200 to repay the loan in full.

An additional characteristic of single payment loans that can increase costs significantly is call a rollover.

How Title Loan Roll overs work

Many of the states with single payment title loans allow you roll over or extend the loan if you cannot repay it by the deadline. This can cause the fees to add up quickly.

If we use the $1,000 loan example and at the end of the first 30 days you cannot repay the full $1200, you will need to pay the $200 in interest and fees and “rollover” the loan for another month.

This means you will owe $1200 at the end of the second month, this is after paying $200 the first month. If you continue to “rollover” the loan you can see how the interest and fees quickly add up.

A $1,000 can end up costing two or three times that amount in interest and fees.

For single payment title loans make sure you can repay the full amount by the due date to avoid getting caught in a cycle of rolling over the loan without reducing the principal.

Monthly Installment Title Loans:

The other type of title loan is a monthly installment loan that is amortized over the loan period. Some states took notice of the difficulty single payment loans caused borrowers and took action to make the loans easier to repay.

Monthly term loans consist of equal monthly payments of principle and interest over a period of usually 4 – 12 months; and some even longer. This means a portion of every payment is applied to the principal of the loan.

These loans work the same way any other car loan works. You make a payment of the same amount each month, for the period of the loan, until the loan is paid off.

This is called loan amortization; learn more here: https://www.thebalance.com/how-amortization-works-315522.

Monthly Installment Title Loan Benefits

These loans tend to give the borrower more flexibility by providing more time to repay the full amount. They allow borrowers to make smaller monthly payments. This increases the probability of repaying the loan without defaulting.

Still, borrowers should make sure they can at least make the minimum payment each month to avoid the consequences of a missed payment.

While it is possible to get a title loan without income verification, it is recommended to always have the ability to repay the loan.

States that offer monthly term loans include Arizona, Illinois, Texas, Virginia, and Wisconsin.

Monthly Installment Title Loan Example:

As an example, a $1,000 12 month loan with a 96% APR costs less than $1,600 to repay over the full 12 months. The monthly payment is approximately $138.

With no prepayment penalty, you can pay the entire loan off in 30 days for a total cost of approximately $1080. This is significantly less than the single payment loan.

Want to calculate a different loan amount with a different loan length? Use our car title loan calculator to compute the monthly payment for any loan amount and term.

Not all monthly installment loans are as cheap as our online title loans. Some lenders that charge very high rates can have loan repayment amounts of two to three times the amount borrowed; similar to the single payment lenders.

Choosing your lender wisely, and negotiating a lower interest rate is important to getting the best deal on a title loan.

Title Loan Interest Rates:

What are title loan interest rates? There is no simple answer to this question as rates vary from state to state and lender to lender.

Some are as high as 300% APR; although rates this high are not as common today as they were in the past. Rates can be as low as 5% APR, like in Texas, but with a catch. Title loans in Texas have credit access fees which can be substantial.

Title loan interest is usually quoted as a Monthly Rate which is important to note. 20% per month sounds OK but it is actually 240% APR.

Some states noticed the difficulty consumers had repaying a 30 day, single payment title loan. They took action and required monthly payments of both principal and interest. These monthly installment loans are more common, especially for online car title loans.

Interest rates for these monthly term loans can be much lower that 300% APR. In fact, rates for a fraction of this are available from multiple lenders.

Make sure to do a bit of research and shop around when looking for a title loan. Interest rates can vary widely from lender to lender and even vary within a lender depending on the size if your loan.

Take your time and find a lender with a reasonable rate and a payment plan you can afford.

An affordable title loan should be your goal. Find a reputable lender that charges rates that result in payments you can comfortably afford. If there is any doubt about repaying the loan, seek an alternative.

Title Loan Information Online

If you are trying to learn how title loans work your first source is likely an Internet search. Many seemingly reliable publishers have published a series of inaccurate articles relating to car title loans and how they work.

Unfortunately much of the information provided is either biased, outdated, and/or inaccurate. Many of these articles have advertiser disclaimers, which probably explains it. But it still does a disservice to their readers.

Who Qualifies for a Title Loan?

To qualify for a title loan you will need a vehicle, free and clear vehicle title, drivers license, and insurance. You will also need some way to repay the loan (income from work or other source).

What about credit? That is one of the benefits of a car title loan and one of the reasons they are so easy to qualify for, your vehicle is your credit. However, just because you qualify for a title loan does not mean it is the right choice.

What if I’m still making Car Payments?

As mentioned, a lien free title is a key requirement for a title loan. In some cases, you still may be able to qualify for a title loan if you are still making payments.

In these cases there needs to be a significant amount of equity in the vehicle and the loan is almost paid off. You may also be able to refinance your title loan if you are stuck in a loan with unfavorable terms.

What is needed for a Car Title Loan?

Car title loans have certain requirements just like any other loan. A common question when searching for one of the loans is ‘what is needed’? The short answer is shown in the figure below:

- Car Title

- Insurance Card

- Drivers license

The specific requirements will also vary from lender to lender but have some general requirements in common. To get a title loan you will need, at a minimum, a vehicle with some equity in it, a valid drivers license, and a lien free title. Depending on the lender there may be some additional requirements.

Many lenders require proof of insurance, proof of residence, and proof of income. Proof of the ability to repay the loan can often be substituted for proof of income. This means you can get a title loan with no income verification.

This is usually all you will need for a car title loan. Although some lenders may also require a spare key and some may require a GPS device be added to your vehicle.

Shopping for a Car Title Loan

Car title loans can be confusing and shopping for one can be an intimidating process. This is especially true if you are new to car title loans and don’t understand how they work.

Add to that the financial stress that comes with needing a title loan in the first place; and it is understandable to have hesitations and doubts about the process.

Further, the conflicting information on the Internet, some published by lenders, others published by competitors to lenders, certainly doesn’t make things any easier.

Additionally, like many other loans, some lenders tend to make them more complicated than they really are.

Now that we’ve pointed out the challenges, here are some solutions. Fast Title Lenders is a different kind of title loan company and we try to provide all readers with accurate information related to car title loans.

Our philosophy is to provide title loan customers with the facts; clear and complete information related to title loans. Not marketing nonsense that doesn’t help make an informed decisions.

Browse our site and you’ll find a wealth of information including articles pointing out the costs of title loans, tactics lenders use, and alternatives to title loans.

Online options are also available including loans without a vehicle inspection.

How do I get a Title Loan?

Assuming you meet the car title loan requirements, the first step is to prepare for the loan. As mentioned, this is a critical step when getting a title loan.

It can make a big difference in how much interest you pay as well as how well the title loan process goes. Title lenders charge different rates and fees and are not equal.

Many lenders, including many of the large lenders, charge very high rates and may not disclose actual costs until you are ready to sign the loan agreement. This is why it is critical to read the loan agreement in full before signing.

If you are shopping for a title loan, make sure to contact several lenders and ask how much they charge. Find one you are comfortable with that charges a reasonable rate with a payment you can afford.

We go over how to find the best title loan company in our Guide on How to Get a Title Loan.

Applying for a Title Loan

Once you find a lender apply for the loan and complete their process. Most lenders today allow you to apply and start the process online.

The online application process for a title loan is fairly simple and can usually be completed in a few minutes.

Once you complete the online application, the lender will let you know the next steps. For a traditional in-person title loan, this usually involves a short visit to the lender’s location to complete the paperwork.

For completely online title loans the process is a bit different and includes uploading pictures of your vehicle.

Some online title loans require you to visit a 3rd party for a vehicle inspection. Depending on the state, some lenders will come to you to complete the inspection for an online title loan if you can’t make it to their location.

Online title loans are fairly new, so the process will vary from lender to lender. The terms of the loan agreement will also vary, and interest rates will as well.

So it is important to read the loan agreement in full and make sure you understand every clause.

If you don’t understand something, ask the lender to explain it. If they can’t explain it, or you are still unclear, you may want to consider finding another lender.

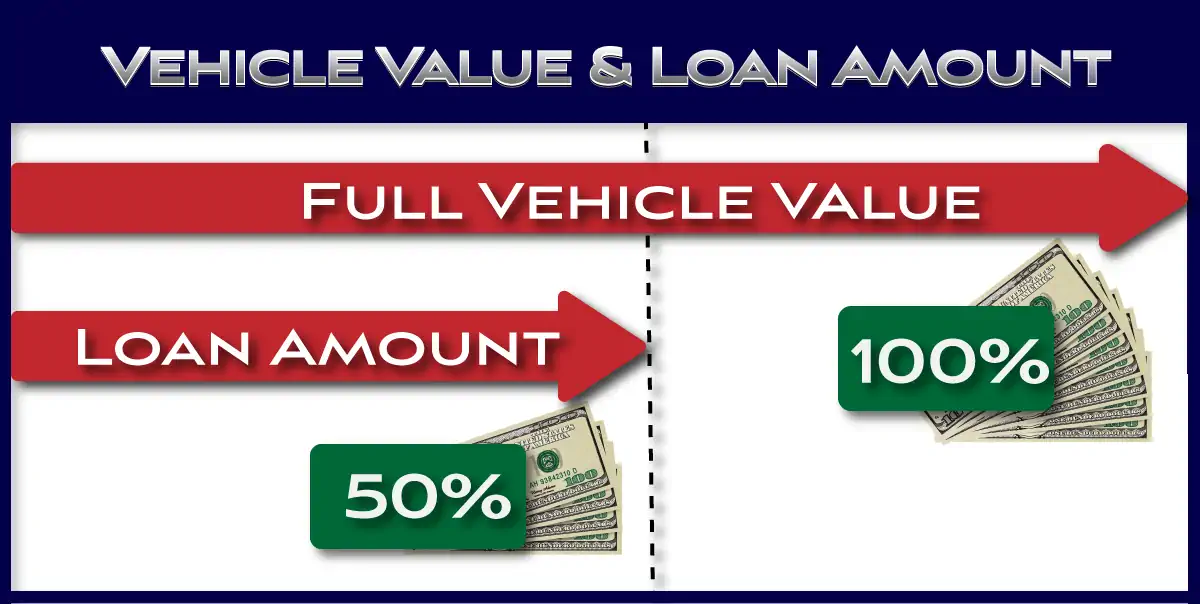

Title Loan Amount

When applying you may be asked how much you want to borrow. Remember, generally the loan is limited to 50% of the vehicle value. This assumes you can afford to make the payment(s).

Car title loans are designed to be short term solutions to meet your immediate financial needs.

Understanding the associated costs and risks, and especially how title loan interest works, will help you decide if one is right for you.

This will also help you prioritize payments to make sure you pay the least amount of interest possible.

How much will a Title Loan give you?

A title loan is unique in that the amount you can borrow is directly dependent on the vehicle, and more specifically, how much your vehicle is worth.

Vehicle values can vary quite a but depending on mileage, condition, and history. For example, a 2010 Mercedes ML550 with 60K miles in excellent condition can be worth almost twice as much as the same vehicle with 150K miles in fair condition.

The wide variation in vehicle values does affect the amount you can borrow from an online lender that offers no inspection title loans.

For good reason, without an inspection the lender takes on more risk (the vehicle may be worth less due to condition). Pictures only go so far when appraising a vehicle.

If you visit lender’s sites, you’ll often find encouragement to borrow the maximum amount you qualify for. In fact, you’ll find plenty of “how much cash can I get” forms promising to get you the most cash.

Just remember, the higher the loan, the more it will cost in interest to repay. Generally, it is a good idea to borrow only what you need to cover your urgent expense.

Vehicle Value

Title lenders generally use the Black Book value of your vehicle (sometimes Kelley Blue Book) to determine the value of your vehicle for the loan. They also perform a brief appraisal to confirm the condition.

For online title loans, you may be required to take the vehicle to have it inspected by a third party, make sure you check with your lender to find out if that is one of their requirements.

Vehicle History is Important

Vehicle history also plays a big role in your vehicle’s value. The number of owners, accidents, salvage history, rental use, and other information available in a vehicle history report will have an effect on your vehicle’s value.

This includes whether or not the vehicle has been in an accident, has a salvage history, or an odometer discrepancy. Use the information to adjust your vehicle value estimate as necessary.

This will give you an idea of how much you will be able to borrow. The maximum loan amount is directly related to the vehicle value. The value of the vehicle is a critical element of a title loan because the vehicle secures the loan.

How do Title Loans Work – Title Loan Collateral

When you get a car title loan you are pledging your vehicle as collateral for the loan (not just the vehicle title). You can continue to use and drive the vehicle, just as you would with any other car loan.

However, if you default on the loan, the lender may repossess your vehicle to recover their costs.

Depending on the state you live in they may also keep any proceeds from the sale of the vehicle. Some states require the lender to return excess proceeds from the sale of your vehicle, although some do not.

This can be a significant amount of money, make sure to find out your lender’s policy as it relates to this.

Nobody plans on having their car repossessed and sold, but losing any excess from the sale can make the situation even worse.

How do Title Loans Work – Process

Car title loans are one of the fastest and easiest ways to turn your car’s equity into cash. The title loan process is usually fairly straight forward. This does depend on the specific lender.

The process starts with a simple application. Most lenders allow you to fill out at least part of the application online.

Once completed, you’ll want to get your paperwork ready. We suggest putting everything in a single file or folder or file to make sure the process goes quickly.

Then, visit the lender, get your cash, and make your payments. It is usually that simple. Make sure to do your research first as lenders’ policies regarding fees, interest rates, and payment methods vary.

Online Title Loan Options

Online title loans are now available in many states. This includes online title loans that do not require a store visit or a physical vehicle inspection. In fact, it is possible to get a title loan that doesn’t require the car. This requires you to:

- Own the vehicle

- Have access to the vehicle

- Take vehicle pictures

- Meet the title loan requirements

The process for getting a completely online title loan is similar to an in-person loan, except every part of the process in done online. This include applying, getting approved, loan funding, and servicing. When the process is completed 100% over the web these are sometimes called an instant online title loan.

How do Bad Credit Title Loans work?

As mentioned, there is no credit check with most title loans. A bad credit title loan works the same way any other title loan works.

A bad credit title loan is simply a title loan with a lender that either does not check your credit or does not use the credit score as a factor for approving the loan.

In these cases your vehicle is your credit. This means you can get a title loan with:

- Bad Credit

- No Credit

- Any Credit

- Or Just Prefer Privacy

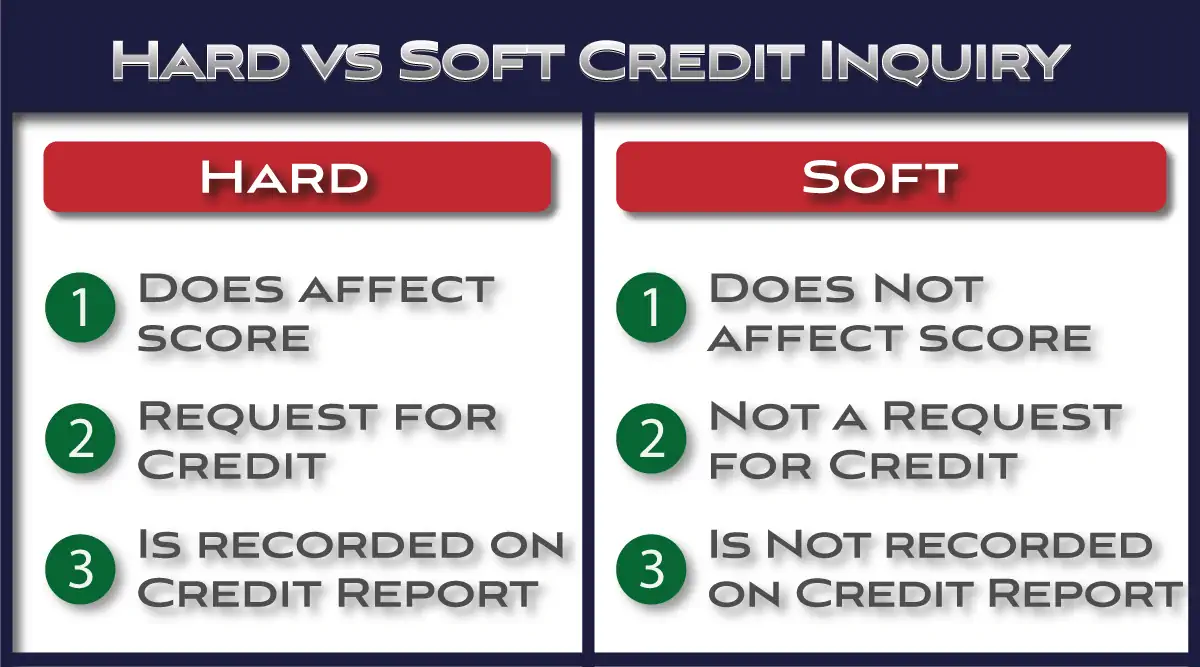

Itis important to understand the difference between a hard credit inquiry (credit check) and a soft credit inquiry. Some lenders will perform a soft credit inquiry to verify information. These do not affect your credit score.

How does a Default on a Title Loan work?

Generally, because the loan is secured by your vehicle, if you default the lender may repossesses your vehicle. We say may because not all lenders will jump at repossession.

For the best title loan companies, repossession is a last resort and is only done when there is no other option. This is typically after repeated attempts to contact the borrower fail.

This is no different than any other car loan. If you buy a new car, and stop making payments, the car will be repossessed. This is why it is important to communicate with your lender, and also choose your lender wisely.

Some lenders are known for repossessing vehicles after a single late payment. Others are more willing to work with borrowers.

Always make sure to read title loan agreement in full. The default procedures should be spelled out, along with how to cure the default should one happen.

What are the Benefits of a Title Loan?

Title loans have several benefits as well as pros and cons. One of the key benefits is the ability to get cash quickly with no credit check. This is very important for those without perfect credit and access to other funding.

In most cases the process takes about 30 minutes, making them one of the fastest and easiest loans to get. For those that need to complete the loan process online, instant online title loans can offer fast funding through direct deposit.

Additionally, because the vehicle is used to secure the loan, they are very easy to get approved for. Another key benefit of a title loan is the ability to keep driving your vehicle.

This allows you to get the funds you need quickly without an interruption in transportation that would result from selling or pawning your vehicle.

How to Save on a Title Loan

Even the best title loans can cost more than most other forms of credit. This makes ways to save when repaying them very important.

The easiest way to save a significant amount on a car title loan is to find a lender that charges a reasonable rate. The difference between lenders, and even within lenders, can be several hundred dollars per month which can equal thousands over the loan term.

Finding a title loan with a lower payment can save you a significant amount of interest on your next title loan. Additional ways to save include:

1. Negotiate your Title Loan

Many title loan customers do not realize they can negotiate the terms of their loan. There are plenty of title lenders, and lenders are in the business of making loans. Many lenders count on the fact that borrowers have an urgent need and are in a hurry to take care of their emergency expense.

This can lead to not fully reading the loan agreement and agreeing to terms they wouldn’t otherwise agree to. This includes very high interest rates.

When getting a title loan, don’t forget you are the customer. If the rate is too high, ask for a lower one. If it is still too high, find another lender. Make sure to understand all fees and payments associated with the loan.

It is not uncommon, especially for single payment loans, to have excessive fees due with the full loan payment. This can make repaying the loan very difficult and lead to the rollovers previously discussed. If the amount seems unreasonable, ask for a lower one.

2. Make Early and Extra Payments

What if you already have a loan with a very high interest lenders; how do you save on a title loan? Answering the question ‘how do car title loans work’ will provide you with a better understanding of title loans, which should help.

Now you know that making early payments, paying more than the minimum, and making additional payments will significantly reduce the amount of interest you are charged.

If you want to understand more about how interest is charged, we provide a detailed explanation of how title loan interest works with an amortization example.

3. Find the Right Lender

Find a lender that meets all of your needs and don’t be afraid to say no and walk away if the agreement is not something you can commit to.

Don’t get stuck in a very high interest loan that is difficult to repay. This will only cause more problems.

Also, prepare to negotiate. If you think the rate is too high, ask for a lower one. Remember, you are the customer, the lender needs you.

Conclusion:

How do car title loans work? As detailed in this article car title loans work differently depending on both the state and the lender. When used responsibly title loans can be a source of quick cash for emergencies to get you out of a jamb. While title loans work differently, all use your vehicle as collateral for the loan.

Likewise, it is important to do your research first and make sure you are dealing with a reputable title lender. New to title loans? We put together a guide detailing how to get a title loan to help.

Always remember when getting a title loan to find out your costs before signing the loan agreement. Make sure to only borrow what you can afford to repay and always read to loan agreement in full before signing.